What do the National Rifle Association (NRA), the American Civil Liberties Union (ACLU), and nine U.S. Supreme Court justices from five presidential administrations all have in common? That list is likely relatively small. But at least one area of overlap was made evident Thursday when the Court published a unanimous ruling that a New York government official allegedly violated the First Amendment by pressuring insurers and banks to sever busines

What do the National Rifle Association (NRA), the American Civil Liberties Union (ACLU), and nine U.S. Supreme Court justices from five presidential administrations all have in common? That list is likely relatively small. But at least one area of overlap was made evident Thursday when the Court published a unanimous ruling that a New York government official allegedly violated the First Amendment by pressuring insurers and banks to sever business ties with the NRA, which the ACLU is representing.

The decision resuscitates the gun advocacy group's lawsuit against Maria Vullo, the former head of New York's Department of Financial Services (DFS). The U.S. Court of Appeals for the 2nd Circuit had previously ruled in her favor.

At the core of the case is Vullo's advocacy following the 2018 shooting at Marjory Stoneman Douglas High School in Parkland, Florida. After that tragedy, in private meetings with insurance companies, Vullo allegedly expressed she would selectively apply enforcement action to groups that insisted on serving the NRA.

She didn't stop there. She also sent letters titled "Guidance on Risk Management Relating to the NRA and Similar Gun Promotion Organizations" to insurers and banks, in which she encouraged them to "continue evaluating and managing their risks, including reputational risks, that may arise from their dealings with the NRA or similar gun promotion organizations"; to "review any relationships they have with the NRA or similar gun promotion organizations"; and to "take prompt actions to manag[e] these risks and promote public health and safety." And in a press release with then-Gov. Andrew Cuomo, the two officials urged such companies to terminate their relationships with the gun advocacy group. Some took them up on the suggestion.

The constitutional issue at stake here is similar to the one the Court explored in Murthy v. Missouri, the case that asks if President Joe Biden's administration violated the First Amendment when it sought to convince social media companies to remove content it disliked. During those oral arguments in March, many justices appeared sympathetic to the view that government officials had not overstepped the bounds of their authority and had merely exercised their own free speech rights to persuade those companies to adopt their views, not unlike a White House press secretary promoting an ideological slant to the media.

But in NRA v. Vullo, the Court ruled unanimously that Vullo's actions as alleged by the NRA had crossed the line from persuasion into coercion. "Government officials cannot attempt to coerce private parties in order to punish or suppress views that the government disfavors," wrote Justice Sonia Sotomayor. The NRA, she said, "plausibly alleges that respondent Maria Vullo did just that."

The decision sends the case back to the 2nd Circuit, which could still give Vullo qualified immunity, the legal doctrine that shields government officials from suits like the NRA's if the misconduct alleged has not been "clearly established" in prior case law. That outcome is certainly probable, as the 2nd Circuit's original decision not only ruled that Vullo had not violated the Constitution—which the Supreme Court rejected today—but that even if she had, qualified immunity would insulate her from the NRA's claim.

It is difficult to imagine, however, a more obvious violation of the Constitution than the weaponization of government power to cripple advocacy disfavored by the state. The supposed reason for qualified immunity is that taxpayer-funded civil servants deserve fair notice that conduct is unlawful before a victim can seek recourse for those misdeeds. To argue that a government agent could not be expected to understand the contours of the First Amendment here is rather dire.

Many people may struggle to separate the constitutional question from the ideological backdrop. The NRA, after all, is one of the more polarizing lobbying organizations in the country, not least of which because its founding issue—gun rights—is not exactly a topic that elicits cool-headed responses. It has also become an advocacy group not just for firearms but for the Republican Party more broadly and the identity politics associated with it, alienating large swaths of people, to put it mildly.

There is another major group in the country that has followed a similar story arc, just on the other side of the political spectrum: the ACLU. Once a stalwart free speech group—so principled it defended the First Amendment rights of Nazis—it has, in modern times, sometimes actively advocated against civil liberties when those principles transgress progressive politics, an awkward move when considering the group's name. But no matter how much you dislike one or both of them, the NRA and the ACLU coming together here is all the more reflective of the fact that some things, like the First Amendment, really aren't partisan.

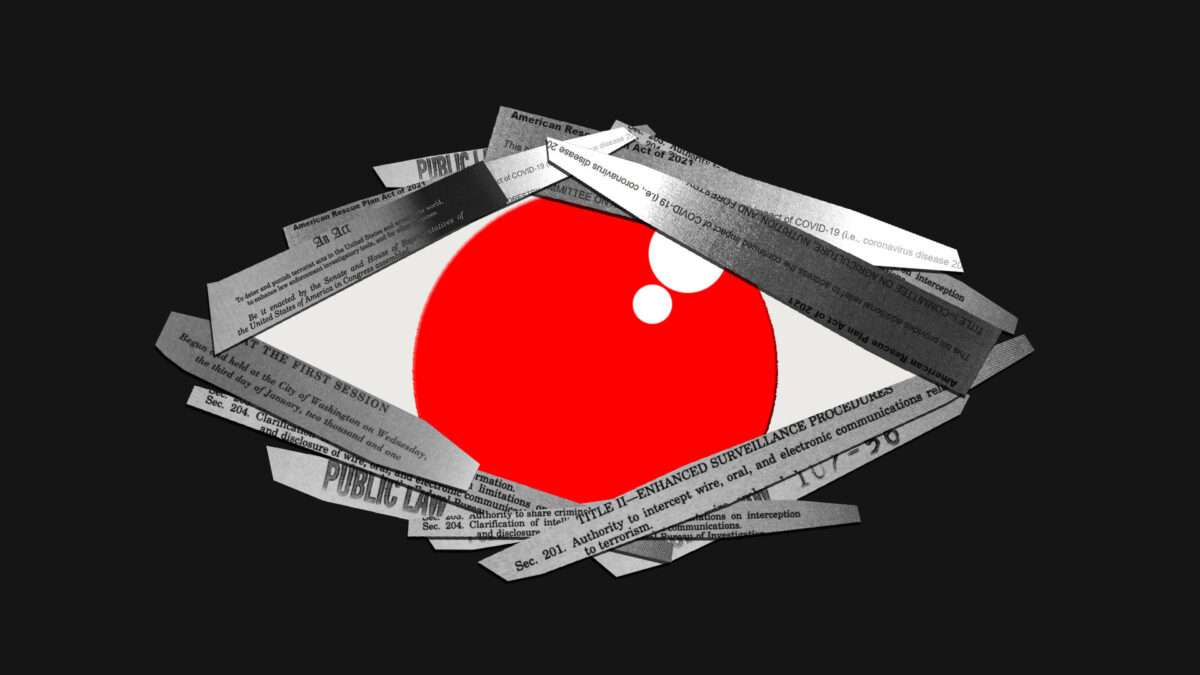

You have a 15-character password, shield the ATM as you enter your PIN, close the door when you meet with your banker, and shred your financial statements. But do you truly have financial privacy? Or has someone else been sitting silently in the room with you this whole time? While you might feel you have secured your financial information, the government has very much wedged its way into the room. Financial privacy has practically vanished over

You have a 15-character password, shield the ATM as you enter your PIN, close the door when you meet with your banker, and shred your financial statements. But do you truly have financial privacy? Or has someone else been sitting silently in the room with you this whole time?

While you might feel you have secured your financial information, the government has very much wedged its way into the room. Financial privacy has practically vanished over the last 50 years.

It's strange how quickly we have accepted the current state of financial surveillance as the norm. Just a few decades ago, withdrawing money didn't involve 20 questions about what we plan to use the money for, what we do for a living, and where we are from. Our daily transactions weren't handed over in bulk to countless third parties.

Yet, what is even stranger is that most people continue to believe in a version of financial privacy that no longer exists. They believe financial records continue to be private and the government needs a warrant to go after them. This belief couldn't be further from reality. Americans do not have financial privacy. Rather, we have the illusion of financial privacy.

Why is this? Put simply, financial surveillance has been kept hidden in three major ways: Encroachments into privacy have evolved gradually through obscure legislation, the scope of surveillance has constantly expanded through inflation, and much of the process is kept intentionally confidential.

Years of Obscure Legislative Changes

Compared to today, customers in the 1970s had far more freedom in opening accounts and interacting with their own money. Back then, the decision to transact with a bank could be based on the cash in one's pocket. Transactions were not scrutinized for threats of terrorism or drug trafficking. Customers were not legally required to supply a photo ID to set up an account. Banks decided for themselves what information they needed to set up an account, and this information remained effectively confidential between the customer and the bank.

This changed in the 1970s when a pivotal piece of legislation was passed: the Bank Secrecy Act. Stemming from concerns in Congress regarding Americans concealing their wealth in offshore accounts, the legislation aimed to gather financial information to detect such activities. For example, financial institutions were required to monitor and report transactions over $10,000 to the government.

It didn't stop there. Over the years, Congress came up with more ways to expand financial surveillance in what is now best referred to as the "Bank Secrecy Act regime."

In 1992, the Annunzio-Wylie Anti–Money Laundering Act led to the introduction of suspicious activity reports (SARs), where, instead of just reporting anything over $10,000, financial institutions had to report "any suspicious transaction relevant to a possible violation of law or regulation." Two years later, the Money Laundering Suppression Act authorized the secretary of the treasury to designate the Financial Crimes Enforcement Network (FinCEN) as the agency to oversee these reports.

Following the September 11 attacks, the USA PATRIOT Act significantly expanded surveillance powers, granting the government easier access to communication records. Hidden among the pages of this sprawling omnibus bill was a set of "know your customer" requirements that forced banks not only to investigate who you are but also to verify that information on behalf of the government.

Again, Congress didn't stop there.

Another extensive omnibus bill, the American Rescue Plan Act of 2021, quietly introduced a rule intended to surveil all bank accounts with at least $600 of activity. Luckily, the controversial measure was noticed and met with immediate pushback. The Treasury Department responded by informing people that the government already has access to much of everyone's financial information.

While the proposal was retracted, the initiative was only shut down partially. Instead of affecting all bank accounts, the law narrowed its scope to require reporting for transactions over $600 made through a payment transmitter such as PayPal, Venmo, or Cash App.

Then the 2022 Special Measures To Fight Modern Threats Act aimed to eliminate some of the checks and balances placed on the Treasury, granting it the authority to use "special measures" to sanction international transactions.

While the Special Measures To Fight Modern Threats Act hasn't been passed, it remains a persistent presence in legislative proposals. It has been introduced in various forms, including as an amendment to the National Defense Authorization Act and as an amendment to the America COMPETES Act of 2022 (both of which failed), as well as a standalone bill.

Similar challenges exist in other bills that try to expand financial surveillance such as the Infrastructure Investment and Jobs Act, Transparency and Accountability in Service Providers Act, Crypto-Asset National Security Enhancement and Enforcement Act, and Digital Asset Anti-Money Laundering Act. Each new bill that passes could further chip away at our financial privacy.

Considering these laws and proposals are buried within thousands of pages of legislation, it's no wonder the public doesn't know what's going on.

A Constant Expansion Through Inflation

Even if every member of the public could read every bill front to back, there are still other ways that the Bank Secrecy Act regime has been able to expand silently each year. Surprisingly, inflation has also contributed to the erosion of our financial privacy.

Following the Bank Secrecy Act's requirement that financial institutions report transactions over $10,000, concerns were raised in court. A coalition including the American Civil Liberties Union, California Bankers Association, and Security National Bank argued that the Bank Secrecy Act violated constitutional protections, including the Fourth Amendment's protection against unreasonable search and seizure, as well as the First Amendment and Fifth Amendment. They successfully obtained a temporary restraining order against the act.

Unfortunately, the Supreme Court later held that the Bank Secrecy Act did not create an undue burden considering it applied to "abnormally large transactions" of $10,000 or more.

Let's put this number into context: In the 1970s, $10,000 was enough to buy two brand-new Corvettes and still have enough money left to cover taxes and upgrades. So perhaps the court's description of these transactions as "abnormally large" was fair at the time.

The problem is that this reporting threshold has never been adjusted for inflation. For over 50 years, it has stayed at $10,000. If the threshold had been adjusted this whole time, it would currently be around $75,000—not $10,000. Not adjusting for inflation would be like not receiving a cost-of-living adjustment for your income; it means losing money each year.

Each year with inflation is another year that the government is granted further access to people's financial activity. In 2022 alone, the U.S. financial services industry filed around 26 million reports under the Bank Secrecy Act. Of those, 20.6 million were on transactions of $10,000 or more, with around 4.3 million filed for suspicious activity. However, the second-most-common reason for filing a SAR was for transactions close to the $10,000 threshold. It almost makes one wonder why Congress bothered with a threshold at all if you can be reported for crossing it and also reported for not crossing it.

While the public has been focusing on the prices of groceries and gasoline when it comes to inflation, the impact of inflation on expanding financial surveillance has largely gone unnoticed.

Much of the Process Is Confidential

With millions of reports being filed each year as both Congress and inflation continue to expand the Bank Secrecy Act regime, shouldn't members of the public at least know if they were reported to the government? For a little while, Congress seemed to think the process should operate that way.

Realizing the need to establish boundaries after the Supreme Court gave the green light to deputizing financial institutions as law enforcement investigators, Congress enacted the Right to Financial Privacy Act of 1978. The legislation mandated that individuals should be told if the government is looking into their finances. Not only did the law establish a notification process, but it also allowed individuals to challenge these requests.

So why don't we see complaints of invasive financial surveillance on the news?

Put simply, the Right to Financial Privacy Act doesn't live up to its name. Although it should result in some protections, Congress included 20 exceptions that let the government get around them. For example, the fourth exception applies to disclosures pursuant to federal statutes, including the reports required under the Bank Secrecy Act.

Making matters worse, the Annunzio-Wylie Anti–Money Laundering Act made filing SARs a confidential process. Both financial institution employees and the government are prohibited from notifying customers if a transaction leads to a SAR.And it's not just the contents of the reports that are confidential: Banks cannot even reveal the existence of a SAR.

With these laws, banks went from protecting the privacy of their depositors to being forced to protect the secrecy of government surveillance programs. It's the epitome of "privacy for me, but not for thee."

The frustration and harm this process causes might not be so secret. There are numerous news stories about banks closing accounts without any explanation. While many have blamed the banks for giving customers the silent treatment, they may be legally prohibited from disclosing that a SAR led to the closure.

As one customer described it, "I feel that I was treated unjustly and at least I deserve to get an explanation. I had no overdrafts, always paid my credit cards on time and I consider myself to be an honest person, the way they closed my accounts made me feel like a criminal." Another customer said, "Any time I asked about why [my account was closed] they said they were not allowed to discuss the matter."

The government claims this process should be kept secret so that it doesn't tip off criminals. Yet SARs are not evidence of a crime by default.

The exact details of the reports are confidential but some aggregate statistics are available. These suggest that the top three reasons for a bank to file a SAR include (1) suspicions concerning the source of funds, (2) transactions below $10,000, and (3) transactions with no apparent economic purpose. These are not smoking guns.

There are many reasons why a bank might close an account, including inactivity, violations of terms and conditions, frequent overdrafts, and internal restructuring. But when banks refuse to explain closures, it might just be because they are prohibited from doing so, further keeping the public in the dark about financial surveillance activities.

A Balancing Act

Many might still ask, "If these reports catch a couple of bad guys, aren't they all worth it?" This raises a fundamental societal question: To what extent are we OK with pervasive surveillance if it stops bad people doing bad things?

To answer this question, we should first recognize that the optimal crime rate is not zero. While a world without crime might seem preferable, the costs of achieving that can be prohibitively high. We can't burn down the entire world just to stop somebody from stealing a pack of gum. There is a percentage of crime that is going to exist—it's not ideal, but it is optimal.

Similarly, the cost of pervasive surveillance is also too high. Maintaining a balance of power by protecting people's privacy is essential for a free society. Surveillance can restrict freedoms, such as the freedom to have certain religious beliefs, support certain causes, partake in dissent, and hold powerful people accountable. We need to have financial privacy. We have too many examples where surveillance has gone wrong and allowed these freedoms to be squashed. We have to be careful about creeping surveillance that tilts the balance of power too far away from the individual.

Removing this huge financial surveillance system doesn't mean ending the fight against terror or crime. It means making sure that Fourth Amendment protections are still present in the modern digital era. It's not supposed to be easy to get this magic permission slip that lets you into everyone's homes. The Constitution was put in place to prevent such abuses—to restrict the powers of government and protect the people.

Breaking the Illusion of Financial Privacy

Over the past 50 years, the U.S. government has slowly built a sprawling system of unchecked financial surveillance. It's time to question whether this is the world we want to live in. Instead of having a regime that generates 26 million reports on Americans at a cost of over $46 billion in a given year, we should have a system that respects individual rights and only goes after criminals.

Yet, government officials seem to have another vision in mind. Through obscure legislative changes, inflationary expansions, and a process of confidentiality, financial privacy has been continuously eroded over time.

Changing this reality is an uphill battle, but it's one that's worth fighting. The first step is raising awareness about how far financial surveillance norms have shifted in just a few decades.Changes won't happen until we dispel the illusion of financial privacy.

As Donald Trump tells it, all of the civil and criminal cases against him are part of a Democratic conspiracy to keep him from returning to the White House. Although some of the many charges against him involve credible allegations of serious crimes, they have been overshadowed recently by two New York cases that are much weaker. In 2016, Manhattan District Attorney Alvin Bragg says, Trump "corrupt[ed] a presidential election" by concealing embar

As Donald Trump tells it, all of the civil and criminal cases against him are part of a Democratic conspiracy to keep him from returning to the White House. Although some of the many charges against him involve credible allegations of serious crimes, they have been overshadowed recently by two New York cases that are much weaker.

In 2016, Manhattan District Attorney Alvin Bragg says, Trump "corrupt[ed] a presidential election" by concealing embarrassing information from voters. And according to New York Attorney General Letitia James, whose lawsuit resulted in a staggering "disgorgement" order against Trump last week, he defrauded lenders and insurers by habitually inflating the value of his assets.

Bragg and James, both Democrats, argue that Trump was dishonest, which will not come as news to anyone who has been paying attention to the persistent gap between reality and his public statements on matters large and small. But neither Bragg nor James has been able to explain exactly who was victimized by the misrepresentations they cite.

Bragg's criminal case, which is now scheduled for trial on March 25, charges Trump with 34 counts of falsifying business records. Each of those is based on an invoice, check, or ledger entry that allegedly was designed to disguise Trump's reimbursement of a $130,000 payment that Michael Cohen, his former lawyer, gave porn star Stormy Daniels shortly before the 2016 election to keep her from talking about her alleged affair with Trump.

Falsifying business records—in this case, mischaracterizing the payments to Cohen as compensation for legal services—is ordinarily a misdemeanor. But Bragg is charging Trump with 34 felonies, each punishable by up to four years in prison, because he allegedly was trying to cover up "another crime."

Bragg says the "criminal activity" that Trump sought to "conceal" included "attempts to violate state and federal election laws." That claim is based on legal interpretations so iffy that Bragg's predecessor, Cyrus R. Vance Jr., rejected them after lengthy consideration.

Explaining why he nevertheless is trying to convert one hush payment into 34 felonies, Bragg complains that Trump "hid damaging information from the voting public during the 2016 presidential election." Although Bragg says that offense is "the heart of the case," it is not a crime: If Daniels had simply agreed not to talk about the alleged affair after Trump asked her nicely, the result would have been the same.

James' case likewise lacks any measurable injury to a specific victim, which is not required by the New York law she used to sue Trump. Although she presented plenty of evidence that Trump overvalued his properties and exaggerated his wealth, she did not show that lenders or insurers suffered any losses as a result.

Most notoriously, Trump claimed his apartment in Manhattan's Trump Tower was 30,000 square feet, nearly three times its actual size. He valued Mar-a-Lago, his golf resort in Palm Beach, based on the assumption that it could be sold for residential purposes, which the deed precluded.

New York County Supreme Court Justice Arthur Engoron also found that the Trump Organization had treated rent-stabilized apartments as if they were not subject to that restriction, assumed regulatory permission for construction that had not in fact been approved, failed to discount expected streams of revenue, dramatically departed from estimates by professional appraisers, and counted Trump's limited partnership interest in a real estate company as cash even though he could not access the money without the company's consent. But the sum that Engoron ordered Trump to pay, which totals nearly half a billion dollars with interest, was styled as "disgorgement" of "ill-gotten gains," not as compensation for damages.

That's because James was not able to identify any damages to lenders or insurers, which she was not legally obliged to do. As in Bragg's case, the striking absence of any injury commensurate with the punishment lends credibility to Trump's reflexive complaint that he is the victim of a partisan vendetta.

In this week's The Reason Roundtable, Katherine Mangu-Ward is in the driver's seat, alongside Nick Gillespie and special guests Zach Weissmueller and Eric Boehm. The editors react to the latest plot twists in Donald Trump's various legal proceedings and the death of Russian opposition leader Alexei Navalny. 00:41—The trials of Donald Trump in Georgia and New York 25:04—Weekly Listener Question 33:23—Sora, a new AI video tool 43:55—The death of Al

In this week's TheReason Roundtable, Katherine Mangu-Ward is in the driver's seat, alongside Nick Gillespie and special guests Zach Weissmueller and Eric Boehm. The editors react to the latest plot twists in Donald Trump's various legal proceedings and the death of Russian opposition leader Alexei Navalny.

00:41—The trials of Donald Trump in Georgia and New York

Send your questions to [email protected]. Be sure to include your social media handle and the correct pronunciation of your name.

Today's sponsor:

ZBiotics. Pre-Alcohol Probiotic Drink is the world's first genetically engineered probiotic. It was invented by Ph.D. scientists to tackle rough mornings after drinking. Here's how it works: When you drink, alcohol gets converted into a toxic byproduct in the gut. It's this byproduct, not dehydration, that's to blame for your rough next day. ZBiotics produces an enzyme to break this byproduct down. Just remember to make ZBiotics your first drink of the night and to drink responsibly, and you'll feel your best tomorrow. Go to zbiotics.com/roundtable to get 15 percent off your first order when you use code ROUNDTABLE at checkout. ZBiotics is backed with a 100 percent money-back guarantee, so if you're unsatisfied for any reason, they'll refund your money, no questions asked.

On Friday, New York County Supreme Court Justice Arthur Engoron ordered Donald Trump to pay a staggering $355 million for repeatedly inflating asset values in statements of financial condition submitted to lenders and insurers. When the interest that Engoron also approved is considered, the total penalty rises to $450 million. All told, Trump and his co-defendants, including three of his children and former Trump Organization CFO Allen Weisselber

On Friday, New York County Supreme Court Justice Arthur Engoron ordered Donald Trump to pay a staggering $355 million for repeatedly inflating asset values in statements of financial condition submitted to lenders and insurers. When the interest that Engoron also approved is considered, the total penalty rises to $450 million. All told, Trump and his co-defendants, including three of his children and former Trump Organization CFO Allen Weisselberg, are on the hook for $364 million, or about $464 million with interest.

On its face, a penalty of nearly half a billion dollars is hard to fathom given that no lender or insurer claimed it suffered a financial loss as a result of the transactions at the center of the case, which was brought by New York Attorney General Letitia James. But the law under which James sued Trump and his co-defendants does not require any such loss. The money demanded by Engoron's 92-page decision, which goes to the state rather than individual claimants, is styled not as damages but as "disgorgement" of "ill-gotten gains." It is aimed not at compensating people who were allegedly harmed by Trump's misrepresentations but at deterring dishonesty that threatens "the financial marketplace."

Proving "common law fraud," Engoron notes, requires establishing that the defendant made a "material" statement he knew to be false, that the plaintiff justifiably relied on that statement, and that he suffered damages as a result. Section 63(12) of New York's Executive Law, by contrast, authorizes the attorney general to sue "any person" who "engage[s] in repeated fraudulent or illegal acts or otherwise demonstrate persistent fraud or illegality in the carrying on, conducting or transaction of business." The attorney general can seek "an order enjoining the continuance of such business activity or of any fraudulent or illegal acts, directing restitution and damages and, in an appropriate case, cancelling" the defendant's business certificate.

"The statute casts a wide net," Engoron observes. It defines "fraud" to include "any device, scheme or artifice to defraud and any deception, misrepresentation, concealment, suppression, false pretense, false promise or unconscionable contractual provisions." Although Engoron found substantial evidence that lenders and insurers relied on the Trump Organization's misrepresentations, the state did not have to prove that they did or that they suffered damages as a result.

"Timely and total repayment of loans does not extinguish the harm that false statements inflict on the marketplace," Engoron writes. "Indeed, the common excuse that 'everybody does it' is all the more reason to strive for honesty and transparency and to be vigilant in enforcing the rules. Here, despite the false financial statements, it is undisputed that defendants have made all required payments on time; the next group of lenders to receive bogus statements might not be so lucky. New York means business in combating business fraud."

Engoron ruled that the appropriate standard of proof was a preponderance of the evidence, which typically applies in civil cases and requires showing that an allegation is more likely than not to be true. "Defendants have provided no legal authority for their contention that the higher 'clear and convincing' standard does, or should, apply," he writes. "A clear and convincing standard applies only when a case involves the denial of, addresses, or adjudicates fundamental 'personal or liberty rights' not at issue in this action."

Engoron had previously ruled that disgorgement of profits is one of the remedies allowed by Section 63(12) in this case. "In flagrant disregard of prior orders of this Court and the First Department [court of appeals], defendants repeat the untenable notion that 'disgorgement is unavailable as a matter of law' in Executive Law §63(12) actions," he wrote in that September 2023 decision, which held that Trump had committed fraud within the meaning of the statute. "This is patently false, as defendants are, or certainly should be, aware that the Appellate Division, First Department made it clear in this very case that '[w]e have already held that the failure to allege losses does not require dismissal of a claim for disgorgement under Executive Law § 63(12).'"

In Friday's decision, Engoron reviews the examples of fraud that he described in the earlier ruling. Most notoriously, they include the claim that Trump's triplex apartment in Manhattan's Trump Tower was 30,000 square feet, nearly three times its actual size. That misrepresentation was included in Trump's statements of financial condition (SFCs) from 2012 through 2016 and was not corrected until after Forbes made the glaring discrepancy public in 2017.

In 2012, former Trump International Realty employee Kevin Sneddon testified, Weisselberg asked him to assess the apartment's value. "In response to the request," Engoron writes, "Sneddon asked Weisselberg if he could see the Triplex, to which Weisselberg responded that that was 'not possible.' Sneddon then asked if Weisselberg could send him a floorplan or specs of the Triplex to evaluate, to which Weisselberg also said 'no.' Sneddon then asked Weisselberg what size the Triplex was, to which Weisselberg responded 'around 30,000 square feet.' Sneddon then used the 30,000 square foot number in ascertaining a value for the Triplex."

The value of Mar-a-Lago, Trump's golf resort in Palm Beach, also figured prominently in the case. The deed to Mar-a-Lago precluded it from ever being used as private residential property, a clause that made it eligible for a lower tax rate. Yet SFCs repeatedly valued Mar-a-Lago as if it could be sold for residential purposes. Engoron notes that Trump "insisted that he believed Mar-a-Lago is worth 'between a billion and a billion five' today, which would require not only valuing it as a private residence, which the deed prohibits, but as more than the most expensive private residence listed in the country by approximately 400%"

Other examples of misrepresentations included treating rent-stabilized apartments as if they were not subject to that restriction, assuming regulatory permission for construction that had not in fact been approved, failing to discount expected streams of revenue, dramatically departing from estimates by professional appraisers, and counting Trump's limited partnership interest in a real estate company as cash even though he could not access the money without the company's consent. More generally, expert testimony indicated, Trump tended to value properties based on rosy "as if" assumptions rather than the "as is" valuations preferred by lenders.

The defendants argued that the accountants charged with compiling the SFCs were responsibile for verifying their accuracy. But as Engoron notes, the accounting firms' role was limited to assembling information provided by the Trump Organization, which they assumed to be accurate. "There is overwhelming evidence from both interested and non-interested witnesses, corroborated by documentary evidence, that the buck for being truthful in the supporting data valuations stopped with the Trump Organization, not the accountants," he says. "Moreover, the Trump Organization intentionally engaged their accountants to perform compilations, as opposed to reviews or audits, which provided the lowest level of scrutiny and rely on the representations and information provided by the client; compilation engagements make clear that the accountants will not inquire, assess fraud risk, or test the accounting records."

Trump also argued that the SFCs were unimportant because lenders and insurers would perform their own due diligence. Engoron was unimpressed by that defense, especially with regard to the insurers. "Because the Trump Organization is a private company, not a publicly traded company," he says, "there is very little that underwriters can do to learn about the financial condition of the company other than to rely on the financial statements that the client provides to them."

Were the Trump Organizations overvaluations "material"? Engoron had already concluded that "the SFCs from 2014-2021 were false by material amounts as a matter of law." Under Section 63(12), he says, materiality "is judged not by reference to reliance by or materiality to a particular victim, but rather on whether the financial statement 'properly reflected the financial condition' of the person to which the statement pertains."

If fraud "is insignificant," Engorion concedes, "then, like most things in life, it just does not matter." But that "is not what we have here," he adds. "Whether viewed in relative (percentage) or absolute (numerical) terms, objectively (the governing standard) or subjectively (how the lenders viewed them), defendants' misstatements were material….The frauds found here leap off the page and shock the conscience."

While there is no precise numerical standard for materiality, Engoron says, "this Court confidently declares that any number that is at least 10% off could be deemed material, and any number that is at least 50% off would likely be deemed material. These numbers are probably conservative given that here, such deviations from truth represent hundreds of millions of dollars, and in the case of Mar-a-Lago, possibly a billion dollars or more."

Did those deviations ultimately matter in the decisions that lenders and insurers made? Engoron's summary provides reason to doubt that they did. Deutsche Bank, he notes, routinely "applied a 50% 'haircut' to the valuations presented by" clients, which a witness "affirmed was the standardized number for commercial real assets." A defense witness opined that lenders generally just want to see "the engagement of a warm body of a billionaire to stand behind the loan in his equity infusion and capital."

James nevertheless argued that Trump, by systematically exaggerating his wealth and the amount of cash he could access, misled lenders about what would happen in the event that the Trump Organization could not meet its obligations. And those misrepresentations, she said, allowed the business to borrow more money on terms more favorable than it otherwise could have obtained.

The difference between the interest rates that lenders charged based on Trump's personal financial guarantee and the rates they would have charged without it was crucial to Engoron's calculation of how much the defendants should disgorge. Over their vigorous objections, he accepted the numbers offered by a state witness, investment bank CEO Michiel McCarty, who compared the rate that Deutsche Bank charged the Trump Organization based on Trump's personal guarantee with the rate it proposed for a loan without that guarantee. By McCarty's calculation, the Trump Organization saved a total of about $168 million in interest on loans for four projects.

By itself, that estimate accounts for nearly half of the disgorgement that Engoron ordered. He also included nearly $127 million in "net profits" from the 2022 sale of the Old Post Office in Washington, D.C., which Trump had converted into a hotel. That deal, James argued, was facilitated "through the use of false SFCs," without which it would not have happened. She also argued that "without the ill-gotten savings on interest rates, defendants would not even have been able to invest in the Old Post Office and/or other projects."

Taking into account the partnership interest "fraudulently labeled as cash," James said, "Trump would have been in a negative cash situation" by 2017 but for the $74 million or so "saved through reduced interest payments." She noted that "the Old Post office loan itself was a construction loan, and its proceeds were necessary to the construction and renovation of the hotel, which enabled the 2022 sale and resulting profits."

Engoron found these arguments, especially the first, persuasive. The profits from the sale of the Old Post Office, he concludes, "were ill gotten gains, subject to disgorgement, which is meant to deny defendants 'the ability to profit from ill-gotten gain.'"

Engoron also counted $60 million in profits from the 2023 sale of a license to operate a golf course at Ferry Point Park in the Bronx, which Trump had obtained from the New York City Department of Parks & Recreation in 2012. "By maintaining the license agreement for Ferry Point, based on fraudulent financials," Engoron says, "Donald Trump was able to secure a windfall profit by selling the license to Bally's Corporation."

Although reliance is not required to prove fraud under Section 63(12), it does implicitly figure in these disgorgement calculations. But for the "fraudulent financials," Engoron assumes, Trump would have had to pay higher interest rates on the four loans, and neither the Ferry Point deal nor the Old Post Office renovation and sale would have happened. The defendants, of course, dispute those counterfactuals.

Explaining the need for continued independent supervision of the Trump Organization, Engoron emphasizes Trump et al.'s "refusal to admit error." After "some four years of investigation and litigation," he says, "the only error (inadvertent, of course) that they acknowledge is the tripling of the size of the Trump Tower Penthouse, which cannot be gainsaid. Their complete lack of contrition and remorse borders on pathological. They are accused only of inflating asset values to make more money. The documents prove this over and over again. This is a venial sin, not a mortal sin. Defendants did not commit murder or arson. They did not rob a bank at gunpoint. Donald Trump is not Bernard Madoff. Yet, defendants are incapable of admitting the error of their ways. Instead, they adopt a 'See no evil, hear no evil, speak no evil' posture that the evidence belies."

Engoron "intends to protect the integrity of the financial marketplace and, thus, the public as a whole," he writes. "Defendants' refusal to admit error—indeed, to continue it, according to the Independent Monitor—constrains this Court to conclude that they will engage in it going forward unless judicially restrained. Indeed, Donald Trump testified that, even today, he does not believe the Trump Organization needed to make any changes based on the facts that came out during this trial."

Although Engoron says his court "is not constituted to judge morality," his outrage at Trump's financial dishonesty is palpable. That dishonesty, which is consistent with the ego-boosting lies that Trump routinely tells about matters small (e.g., the size of the crowd at his inauguration) and large (e.g., a presidential election he still insists was "rigged" by systematic fraud), is indeed striking. In this case, however, it did not result in any injuries that Trump's lenders or insurers could identify. Under New York law, Engoron says, that does not matter. But maybe it should.