In her first economic policy speech as the 2024 Democratic presidential nominee, Kamala Harris rightly criticized Donald Trump for favoring steep tariffs, saying her Republican opponent "wants to impose what is, in effect, a national sales tax on everyday products and basic necessities that we import from other countries." But in the same speech, Harris pitched a half-baked idea that is just as economically dubious, promising to crack down on "pr

In her first economic policy speech as the 2024 Democratic presidential nominee, Kamala Harris rightly criticized Donald Trump for favoring steep tariffs, saying her Republican opponent "wants to impose what is, in effect, a national sales tax on everyday products and basic necessities that we import from other countries." But in the same speech, Harris pitched a half-baked idea that is just as economically dubious, promising to crack down on "price gouging" by the grocery industry.

That proposal is so misguided that it provoked undisguised skepticism from mainstream news outlets such as CNN, the Associated Press, The New York Times, and The Washington Post, along with criticism by Democratic economists. It showed that Harris joins Trump in pushing populist prescriptions that would hurt consumers in the name of sticking it to supposed economic villains.

"If your opponent claims you're a 'communist,'" Post columnist Catherine Rampell suggested, "maybe don't start with an economic agenda that can (accurately) be labeled as federal price controls." Harvard economist Jason Furman, who chaired President Barack Obama's Council of Economic Advisers, was equally scathing.

"This is not sensible policy, and I think the biggest hope is that it ends up being a lot of rhetoric and no reality," Furman told the Times. "There's no upside here, and there is some downside."

That downside stems from any attempt to override market signals by dictating prices. High prices allocate goods to consumers who derive the greatest value from them, encourage producers to expand supply, and spur competition that helps bring prices down.

Without those signals, you get hoarding and shortages. This is not some airy-fairy theory; it reflects bitter experience since ancient times with interventions like the one Harris proposes.

Consider what happened when President Richard Nixon imposed wage and price controls in the 1970s. "Ranchers stopped shipping their cattle to the market, farmers drowned their chickens, and consumers emptied the shelves of supermarkets," Daniel Yergin and Joseph Stanislaw note in their 1998 book on the rise of free markets.

Or consider what happened more recently with eggs. Thanks to avian flu, Furman noted, "egg prices went up last year" because "there weren't as many eggs," but the high prices encouraged "more egg production." If federal regulators had tried to suppress egg prices, they would have short-circuited that market response.

Harris, of course, says she would target only unjustified price increases, the kind that amount to "illegal price gouging" by "opportunistic companies." But as she emphasizes, there currently is no such thing under federal law, and any attempt to define it would be plagued by subjectivity and a lack of relevant knowledge.

The fact that Harris pins the sharp grocery price inflation of recent years on corporate greed suggests that her judgment about such matters cannot be trusted. Economists generally rate other factors—including the war in Ukraine as well as pandemic-related supply disruptions, shifts in consumer demand, and stimulus spending—as much more important.

High profits, in any event, are another important signal that encourages investment and competition. By forbidding "excessive profits," Harris' proposed price policing would undermine the motivation they provide.

According to the most recent numbers, the annual inflation rate dropped below 3 percent as of July. With inflation cooling, this might seem like a strange time for Harris to resuscitate an idea that was already proving disastrous thousands of years ago. But as the Timesnotes, her message "polls well with swing voters."

The broad tariffs that Trump favors, which Harris condemns as "a national sales tax" that would "devastate Americans," also poll well in the abstract. But they are popular only until voters consider the consequences.

In a recent Cato Institute survey, for example, 62 percent of respondents favored a tariff on "imported blue jeans," but that number plummeted when they were asked to imagine the resulting price increases. Harris likewise is counting on voters who like what she says but do not contemplate what it would mean in practice.

It's OK to calm down about the economy. Yes, Friday's unemployment news was bad. Yes, the NASDAQ and Dow Jones neared correction territory on Friday morning. And yes, the Sahm Rule Recession Indicator has now been triggered. Odds are, though, a recession is not imminent. Here are three reasons why, in descending order of optimism. One, recent growth has been strong. Two, the economy has been near full employment for a while, and some kind of job

Here are three reasons why, in descending order of optimism. One, recent growth has been strong. Two, the economy has been near full employment for a while, and some kind of job growth slowdown is almost inevitable. Three, we're past the window where Federal Reserve actions can influence the election, though its recent behavior is still worrying.

Last week, the media's manic mood swing was on the exuberant side from news of a strong 2.8 percent gross domestic product (GDP) growth in the second quarter of 2024, which ended on June 30. This was a surprise improvement on the previous quarter's 1.4 percent growth. A normal reading is around 2 percent. Better, most of that growth was in the private sector, especially in consumer spending and inventory investment.

The current quarter's GDP growth estimate will come out on October 30. It would take a drastic swing to move from 2.8 percent to negative in just one quarter, though it has happened before. It typically takes two consecutive quarters of negative growth for the National Bureau of Economic Research to declare a recession, though its official standard is to call it as they see it.

The unemployment rate went up from 4.1 percent in June to 4.3 percent in July. June's reading snapped a 30-month streak of unemployment at or under 4 percent. This was the longest such streak since the 1960s.

For context, anything under 5 percent is considered pretty good. The eurozone's unemployment rate is currently 6 percent and often tops 10 percent, even in good times.

When an economy is essentially at full employment, a slowdown in job growth isn't necessarily cause for worry. The economy still has 8 million job openings, and the labor force still grew by 114,000 jobs. That annualizes to more than a million more jobs per year.

That is slower than population growth, which isn't ideal. The labor force participation rate is also still below prepandemic levels. But a sane immigration policy combined with labor reforms like loosening occupational licensing requirements would fill more of those job openings while creating more opportunities for workers who are still outside the labor force.

The Federal Reserve's recent actions spark some worry. The Fed has spent the last two-and-a-half years walking back its panicked overreaction to COVID-19, which caused high inflation in the first place, along with a bipartisan deficit spending explosion. Inflation is finally slowing and getting back close to its 2 percent target, down from its 9.2 percent peak.

The trouble is that Fed Chairman Jerome Powell indicated that the Fed will stop focusing solely on inflation and will now pay attention to the labor market as well. The Fed has a dual mandate that tasks it with both keeping inflation low and keeping employment high. These can contradict each other, as Powell might soon find out.

If unemployment continues to worsen, look for the Fed to counteract that with stimulus in the form of interest rate cuts and monetary expansion. The tradeoff to this stimulus is higher inflation—exactly what the Fed has been fighting.

While an expected interest rate cut in September isn't a big deal by itself, if it's the start of a larger stimulus campaign, any short-term economic boost will come at the cost of a slowdown later.

The Fed's actions have lag times ranging from about six months to 18 months, so anything it does now will not impact the election. This is good news for the Fed's independence, but it does not inspire faith in Powell's commitment to fighting inflation. It would be better for the Fed to stay focused on inflation. Monetary policy is a poor tool for job creation. Entrepreneurs have a much better track record.

As usual, the big picture is a mix of short-term pessimism and long-term optimism. Whether or not the current recession doommongering comes true, the long-term trend of increasing superabundance will hold. That's as good a reason for calm as any.

You can add the Internal Revenue Service to the ranks of federal agencies conceding that raining taxpayer money on all and sundry to offset the negative effects of pandemic-era closures didn't go as well as intended. Not only was a program meant to offset the cost of paying workers during lockdowns and voluntary social-distancing prone to being gamed, but the "vast majority" of claims submitted to the program show evidence of being fraudulent. T

You can add the Internal Revenue Service to the ranks of federal agencies conceding that raining taxpayer money on all and sundry to offset the negative effects of pandemic-era closures didn't go as well as intended. Not only was a program meant to offset the cost of paying workers during lockdowns and voluntary social-distancing prone to being gamed, but the "vast majority" of claims submitted to the program show evidence of being fraudulent.

The Tax Man Is Shocked To Discover Fraudsters

In the course of a detailed review of the Employee Retention Credit, "the IRS identified between 10% and 20% of claims fall into what the agency has determined to be the highest-risk group, which show clear signs of being erroneous claims for the pandemic-era credit," the IRS announced June 20. "In addition to this highest risk group, the IRS analysis also estimates between 60% and 70% of the claims show an unacceptable level of risk."

The Employee Retention Credit was offered to businesses that were shut down by government COVID-19 orders in 2020 or the first three quarters of 2021, experienced a required decline in gross receipts during that period, or qualified as a recovery startup business at the end of 2021. But it was clear early on that scammers were taking advantage of giveaways of taxpayer money, either to claim it for themselves or to pose as middlemen helping unwitting business owners file claims.

In March of 2023, the tax agency warned of "blatant attempts by promoters to con ineligible people to claim the credit." In September of that year, it stopped processing claims amidst growing evidence that vast numbers of applications were "improper," as the IRS delicately puts it. In March 2024, the agency announced that its Voluntary Disclosure Program had recovered $1 billion (since raised to over $2 billion) in improper payouts from participants who got to keep 20 percent of the take.

Ultimately, only "between 10% and 20% of the ERC claims show a low risk" for fraud, even by generous federal standards for throwing other people's money at problems largely of government creation.

"We will now use this information to deny billions of dollars in clearly improper claims and begin additional work to issue payments to help taxpayers without any red flags on their claims," commented IRS Commissioner Danny Werfel.

As of the end of May, the IRS "has initiated 450 criminal cases, with potentially fraudulent claims worth nearly $7 billion."

There's More Fraud Where That Came From

Of course, this is only the tip of the iceberg when it comes to pandemic stimulus fraud.

In April, Attorney General Merrick Garland boasted that the COVID-19 Fraud Enforcement Task Force (yes, it's widespread enough to rate its own task force) had "charged more than 3,500 defendants, seized or forfeited over $1.4 billion in stolen COVID-19 relief funds, and filed more than 400 civil lawsuits resulting in court judgements and settlements."

Strong work. But the various pandemic stimulus bills tallied up to trillions of dollars. And a lot more than a few billion ended up in the hands of grifters.

"The total amount of fraud across all UI [unemployment insurance] programs (including the new emergency programs) during the COVID-19 pandemic was likely between $100 billion and $135 billion—or 11% to 15% of the total UI benefits paid out during the pandemic," the Government Accountability Office warned last September.

Earlier, the Small Business Administration's Inspector General found more than $200 billion stolen from the Economic Injury Disaster Loan (EIDL) program and Paycheck Protection Program (PPP). "This means at least 17 percent of all COVID-19 EIDL and PPP funds were disbursed to potentially fraudulent actors," noted the report.

With between 70 percent and 90 percent of claims for the Employee Retention Credit identified as likely scams, either the IRS is a stand-out magnet for grifters or other agencies need to return to their own investigations with a somewhat more skeptical eye.

Stimulus Fueled Inflation as Well as Fraud

It's maddening enough that the federal government is handing out vast sums of money to con artists. But Americans are contending with a 2024 economy in which the U.S. Bureau of Labor Statistics' own inflation calculator finds that it takes $124.77 to purchase what $100 bought in 2019, before anybody heard of COVID-19. Federal stimulus programs are directly to blame for much of that inflationary slippage in the dollar's buying power.

"U.S. fiscal stimulus during the pandemic contributed to an increase in inflation of about 2.6 percentage points in the U.S.," three economists with the Federal Reserve Bank of St. Louis estimated last year. The reason, they said, was that governments "injected large amounts of money into the economy"—money created from thin air to artificially pump up the economy.

"Inflation comes when aggregate demand exceeds aggregate supply," agreed economist John Cochrane of the Hoover Institution and the Cato Institute in a March piece for the International Monetary Fund. "The source of demand is not hard to find: in response to the pandemic's dislocations, the US government sent about $5 trillion in checks to people and businesses, $3 trillion of it newly printed money, with no plans for repayment."

Officials justified the stimulus as a necessary evil to offset economic collapse from often-mandatory pandemic closures by keeping demand flowing with government checks. After conceding that stimulus fueled inflation, the St. Louis Federal Reserve economists argued that massive spending likely prevented "worse outcomes despite the price pressures that may have resulted from the spending."

But officials could have refrained from issuing closure orders so the economy could function without mandated disruptions. That would have made the creation of trillions of dollars from thin air and its distribution around the country entirely beside the point. Then, grifters wouldn't have opportunity to scam hundreds of billions of dollars out of federal agencies, including the IRS.

It's nice that the IRS, like other federal agencies, is catching up with the vast fraud it enabled. But it would be better if government officials weren't constantly addressing problems they created.

Congressional Budget Office (CBO) projections provide valuable insights into how a big chunk of your income is being spent and reveal the long-term consequences of our government's current fiscal policies—you may endure them, and your children most certainly will. Yet, like most other projections looking into our future, these numbers should be taken with a grain of salt. So should claims that CBO projections validate anyone's fiscal track record

Congressional Budget Office (CBO) projections provide valuable insights into how a big chunk of your income is being spent and reveal the long-term consequences of our government's current fiscal policies—you may endure them, and your children most certainly will. Yet, like most other projections looking into our future, these numbers should be taken with a grain of salt. So should claims that CBO projections validate anyone's fiscal track record.

So much can and likely will happen to make projections moot and our fiscal outlook much grimmer. Unforeseen events, economic changes, and policy decisions render them less accurate over time. The CBO knows this and recently released alternative scenarios based on different sets of assumptions, and it doesn't look good. It remains a wonder that more politicians, now given a more realistic range of possibilities, aren't behaving like it.

First, let's recap what the situation looks like under the usual rosy growth, inflation, and interest rate assumptions. Due to continued overspending, this year's deficit will be at least $1.6 trillion, rising to $2.6 trillion by 2034. Debt held by the public equals roughly 99 percent of our economy—measured by gross domestic product (GDP)—annually, heading to 116 percent in 2034.

The only reason these numbers won't be as high as projected last year is that a few House Republicans fought hard to impose some spending caps during the debt ceiling debate. The long-term outlook is even scarier, with public debt reaching 166 percent of GDP in 30 years and all federal debt reaching 180 percent.

No one should be surprised. To be sure, the COVID-19 pandemic and the Great Recession made things worse, but we've been on this path for decades.

Unfortunately, if any of the assumptions underlying these projections change again, things will get a lot worse. That's where the CBO's alternative paths help. Policymakers and the public can better see the potential risks and opportunities associated with various fiscal policy choices, enabling them to make more informed decisions.

For instance, the CBO highlights that if the labor force grows annually by just 0.1 fewer percentage points than originally projected—even if the unemployment rate stays the same—slower economic growth will lead to a deficit $142 billion larger than baseline projections between 2025 and 2034. A similarly small slowdown in the productivity rate would lead to an added deficit of $304 billion over that period.

Back in 2020, the prevalent theory among those who claimed we shouldn't worry about debt was that interest rates were remarkably low and would stay low forever. As if. These guys have since learned what many of us have known for years: that interest rates can and will go up when the situation gets bad enough. So, what happens if rates continue to rise above and beyond those CBO used in its projections? Even a minuscule 0.1-point rise above the baseline would produce an additional $324 billion on the deficit over the 2025-2034 period.

The same is true with inflation, which, as every shopper can see, has yet to be defeated. If inflation, as I fear, doesn't go away as fast as predicted by CBO—largely because debt accumulation is continuing unabated—it will slow growth, increase interest rates, and massively expand the deficit. To be precise, an increase in overall prices of just 0.1 points over the CBO baseline would result in higher interest rates and a deficit of $263 billion more than projected.

Now, imagine all these variations from the current projections happening simultaneously. It's a real possibility. The deficit hike would be enormous, which could then trigger even more inflation and higher interest rates. The question that remains is: Why aren't politicians on both sides more worried than they seem to be?

What needs to happen before they finally decide to treat our fiscal situation as a real threat? President Joe Biden doesn't want to tackle the debt issue. In fact, he's actively adding to the debt with student loan forgiveness, subsidies to big businesses, and other nonsense. Meanwhile, some Republicans pay lip service to our financial crisis, but few are willing to tackle the real problem of entitlement spending.

The time for political posturing is over. The longer we wait to address these issues, the more severe the consequences will be for future generations. It's time for our leaders to prioritize the nation's long-term economic health over short-term political gains and take bold steps toward fiscal responsibility. Only then can we hope to secure a stable and prosperous future for all Americans.

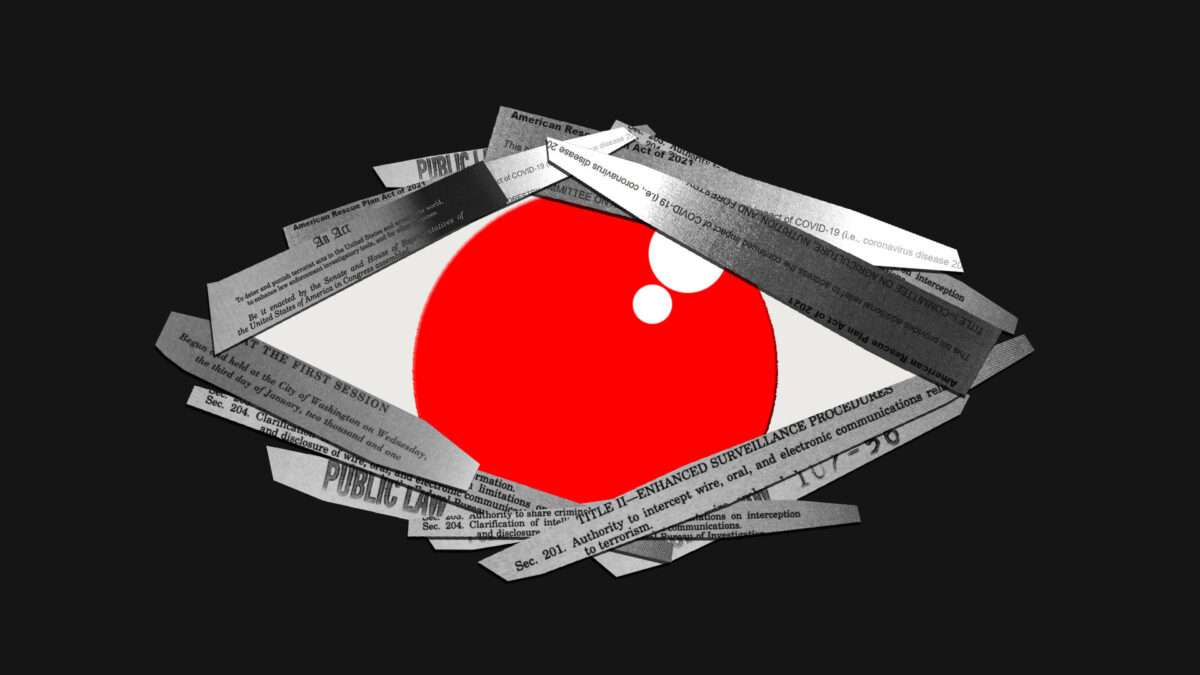

You have a 15-character password, shield the ATM as you enter your PIN, close the door when you meet with your banker, and shred your financial statements. But do you truly have financial privacy? Or has someone else been sitting silently in the room with you this whole time? While you might feel you have secured your financial information, the government has very much wedged its way into the room. Financial privacy has practically vanished over

You have a 15-character password, shield the ATM as you enter your PIN, close the door when you meet with your banker, and shred your financial statements. But do you truly have financial privacy? Or has someone else been sitting silently in the room with you this whole time?

While you might feel you have secured your financial information, the government has very much wedged its way into the room. Financial privacy has practically vanished over the last 50 years.

It's strange how quickly we have accepted the current state of financial surveillance as the norm. Just a few decades ago, withdrawing money didn't involve 20 questions about what we plan to use the money for, what we do for a living, and where we are from. Our daily transactions weren't handed over in bulk to countless third parties.

Yet, what is even stranger is that most people continue to believe in a version of financial privacy that no longer exists. They believe financial records continue to be private and the government needs a warrant to go after them. This belief couldn't be further from reality. Americans do not have financial privacy. Rather, we have the illusion of financial privacy.

Why is this? Put simply, financial surveillance has been kept hidden in three major ways: Encroachments into privacy have evolved gradually through obscure legislation, the scope of surveillance has constantly expanded through inflation, and much of the process is kept intentionally confidential.

Years of Obscure Legislative Changes

Compared to today, customers in the 1970s had far more freedom in opening accounts and interacting with their own money. Back then, the decision to transact with a bank could be based on the cash in one's pocket. Transactions were not scrutinized for threats of terrorism or drug trafficking. Customers were not legally required to supply a photo ID to set up an account. Banks decided for themselves what information they needed to set up an account, and this information remained effectively confidential between the customer and the bank.

This changed in the 1970s when a pivotal piece of legislation was passed: the Bank Secrecy Act. Stemming from concerns in Congress regarding Americans concealing their wealth in offshore accounts, the legislation aimed to gather financial information to detect such activities. For example, financial institutions were required to monitor and report transactions over $10,000 to the government.

It didn't stop there. Over the years, Congress came up with more ways to expand financial surveillance in what is now best referred to as the "Bank Secrecy Act regime."

In 1992, the Annunzio-Wylie Anti–Money Laundering Act led to the introduction of suspicious activity reports (SARs), where, instead of just reporting anything over $10,000, financial institutions had to report "any suspicious transaction relevant to a possible violation of law or regulation." Two years later, the Money Laundering Suppression Act authorized the secretary of the treasury to designate the Financial Crimes Enforcement Network (FinCEN) as the agency to oversee these reports.

Following the September 11 attacks, the USA PATRIOT Act significantly expanded surveillance powers, granting the government easier access to communication records. Hidden among the pages of this sprawling omnibus bill was a set of "know your customer" requirements that forced banks not only to investigate who you are but also to verify that information on behalf of the government.

Again, Congress didn't stop there.

Another extensive omnibus bill, the American Rescue Plan Act of 2021, quietly introduced a rule intended to surveil all bank accounts with at least $600 of activity. Luckily, the controversial measure was noticed and met with immediate pushback. The Treasury Department responded by informing people that the government already has access to much of everyone's financial information.

While the proposal was retracted, the initiative was only shut down partially. Instead of affecting all bank accounts, the law narrowed its scope to require reporting for transactions over $600 made through a payment transmitter such as PayPal, Venmo, or Cash App.

Then the 2022 Special Measures To Fight Modern Threats Act aimed to eliminate some of the checks and balances placed on the Treasury, granting it the authority to use "special measures" to sanction international transactions.

While the Special Measures To Fight Modern Threats Act hasn't been passed, it remains a persistent presence in legislative proposals. It has been introduced in various forms, including as an amendment to the National Defense Authorization Act and as an amendment to the America COMPETES Act of 2022 (both of which failed), as well as a standalone bill.

Similar challenges exist in other bills that try to expand financial surveillance such as the Infrastructure Investment and Jobs Act, Transparency and Accountability in Service Providers Act, Crypto-Asset National Security Enhancement and Enforcement Act, and Digital Asset Anti-Money Laundering Act. Each new bill that passes could further chip away at our financial privacy.

Considering these laws and proposals are buried within thousands of pages of legislation, it's no wonder the public doesn't know what's going on.

A Constant Expansion Through Inflation

Even if every member of the public could read every bill front to back, there are still other ways that the Bank Secrecy Act regime has been able to expand silently each year. Surprisingly, inflation has also contributed to the erosion of our financial privacy.

Following the Bank Secrecy Act's requirement that financial institutions report transactions over $10,000, concerns were raised in court. A coalition including the American Civil Liberties Union, California Bankers Association, and Security National Bank argued that the Bank Secrecy Act violated constitutional protections, including the Fourth Amendment's protection against unreasonable search and seizure, as well as the First Amendment and Fifth Amendment. They successfully obtained a temporary restraining order against the act.

Unfortunately, the Supreme Court later held that the Bank Secrecy Act did not create an undue burden considering it applied to "abnormally large transactions" of $10,000 or more.

Let's put this number into context: In the 1970s, $10,000 was enough to buy two brand-new Corvettes and still have enough money left to cover taxes and upgrades. So perhaps the court's description of these transactions as "abnormally large" was fair at the time.

The problem is that this reporting threshold has never been adjusted for inflation. For over 50 years, it has stayed at $10,000. If the threshold had been adjusted this whole time, it would currently be around $75,000—not $10,000. Not adjusting for inflation would be like not receiving a cost-of-living adjustment for your income; it means losing money each year.

Each year with inflation is another year that the government is granted further access to people's financial activity. In 2022 alone, the U.S. financial services industry filed around 26 million reports under the Bank Secrecy Act. Of those, 20.6 million were on transactions of $10,000 or more, with around 4.3 million filed for suspicious activity. However, the second-most-common reason for filing a SAR was for transactions close to the $10,000 threshold. It almost makes one wonder why Congress bothered with a threshold at all if you can be reported for crossing it and also reported for not crossing it.

While the public has been focusing on the prices of groceries and gasoline when it comes to inflation, the impact of inflation on expanding financial surveillance has largely gone unnoticed.

Much of the Process Is Confidential

With millions of reports being filed each year as both Congress and inflation continue to expand the Bank Secrecy Act regime, shouldn't members of the public at least know if they were reported to the government? For a little while, Congress seemed to think the process should operate that way.

Realizing the need to establish boundaries after the Supreme Court gave the green light to deputizing financial institutions as law enforcement investigators, Congress enacted the Right to Financial Privacy Act of 1978. The legislation mandated that individuals should be told if the government is looking into their finances. Not only did the law establish a notification process, but it also allowed individuals to challenge these requests.

So why don't we see complaints of invasive financial surveillance on the news?

Put simply, the Right to Financial Privacy Act doesn't live up to its name. Although it should result in some protections, Congress included 20 exceptions that let the government get around them. For example, the fourth exception applies to disclosures pursuant to federal statutes, including the reports required under the Bank Secrecy Act.

Making matters worse, the Annunzio-Wylie Anti–Money Laundering Act made filing SARs a confidential process. Both financial institution employees and the government are prohibited from notifying customers if a transaction leads to a SAR.And it's not just the contents of the reports that are confidential: Banks cannot even reveal the existence of a SAR.

With these laws, banks went from protecting the privacy of their depositors to being forced to protect the secrecy of government surveillance programs. It's the epitome of "privacy for me, but not for thee."

The frustration and harm this process causes might not be so secret. There are numerous news stories about banks closing accounts without any explanation. While many have blamed the banks for giving customers the silent treatment, they may be legally prohibited from disclosing that a SAR led to the closure.

As one customer described it, "I feel that I was treated unjustly and at least I deserve to get an explanation. I had no overdrafts, always paid my credit cards on time and I consider myself to be an honest person, the way they closed my accounts made me feel like a criminal." Another customer said, "Any time I asked about why [my account was closed] they said they were not allowed to discuss the matter."

The government claims this process should be kept secret so that it doesn't tip off criminals. Yet SARs are not evidence of a crime by default.

The exact details of the reports are confidential but some aggregate statistics are available. These suggest that the top three reasons for a bank to file a SAR include (1) suspicions concerning the source of funds, (2) transactions below $10,000, and (3) transactions with no apparent economic purpose. These are not smoking guns.

There are many reasons why a bank might close an account, including inactivity, violations of terms and conditions, frequent overdrafts, and internal restructuring. But when banks refuse to explain closures, it might just be because they are prohibited from doing so, further keeping the public in the dark about financial surveillance activities.

A Balancing Act

Many might still ask, "If these reports catch a couple of bad guys, aren't they all worth it?" This raises a fundamental societal question: To what extent are we OK with pervasive surveillance if it stops bad people doing bad things?

To answer this question, we should first recognize that the optimal crime rate is not zero. While a world without crime might seem preferable, the costs of achieving that can be prohibitively high. We can't burn down the entire world just to stop somebody from stealing a pack of gum. There is a percentage of crime that is going to exist—it's not ideal, but it is optimal.

Similarly, the cost of pervasive surveillance is also too high. Maintaining a balance of power by protecting people's privacy is essential for a free society. Surveillance can restrict freedoms, such as the freedom to have certain religious beliefs, support certain causes, partake in dissent, and hold powerful people accountable. We need to have financial privacy. We have too many examples where surveillance has gone wrong and allowed these freedoms to be squashed. We have to be careful about creeping surveillance that tilts the balance of power too far away from the individual.

Removing this huge financial surveillance system doesn't mean ending the fight against terror or crime. It means making sure that Fourth Amendment protections are still present in the modern digital era. It's not supposed to be easy to get this magic permission slip that lets you into everyone's homes. The Constitution was put in place to prevent such abuses—to restrict the powers of government and protect the people.

Breaking the Illusion of Financial Privacy

Over the past 50 years, the U.S. government has slowly built a sprawling system of unchecked financial surveillance. It's time to question whether this is the world we want to live in. Instead of having a regime that generates 26 million reports on Americans at a cost of over $46 billion in a given year, we should have a system that respects individual rights and only goes after criminals.

Yet, government officials seem to have another vision in mind. Through obscure legislative changes, inflationary expansions, and a process of confidentiality, financial privacy has been continuously eroded over time.

Changing this reality is an uphill battle, but it's one that's worth fighting. The first step is raising awareness about how far financial surveillance norms have shifted in just a few decades.Changes won't happen until we dispel the illusion of financial privacy.

Enlarge (credit: apomares | E+)

A jury has unanimously convicted Avi Eisenberg in the US Department of Justice's first case involving cryptocurrency open-market manipulation, the DOJ announced Thursday.

The jury found Eisenberg guilty of commodities fraud, commodities market manipulation, and wire fraud in connection with the manipulation on a decentralized cryptocurrency exchange called Mango Markets.

Eisenberg is scheduled to be sentenced on July 29 and is facing "a maximum

A jury has unanimously convicted Avi Eisenberg in the US Department of Justice's first case involving cryptocurrency open-market manipulation, the DOJ announced Thursday.

The jury found Eisenberg guilty of commodities fraud, commodities market manipulation, and wire fraud in connection with the manipulation on a decentralized cryptocurrency exchange called Mango Markets.

Eisenberg is scheduled to be sentenced on July 29 and is facing "a maximum penalty of 10 years in prison on the commodities fraud count and the commodities manipulation count, and a maximum penalty of 20 years in prison on the wire fraud count," the DOJ said.

President Joe Biden will reportedly use tonight's State of the Union address to once more rail against what the White House has taken to calling "shrinkflation"—the annoying corporate practice of shrinking the size of products rather than raising prices. Politico reported this week that "recent drafts of Biden's State of the Union address have included a reference to shrinkflation as part of a broader segment on administration efforts to pressure

President Joe Biden will reportedly use tonight's State of the Union address to once more rail against what the White House has taken to calling "shrinkflation"—the annoying corporate practice of shrinking the size of products rather than raising prices.

Politicoreported this week that "recent drafts of Biden's State of the Union address have included a reference to shrinkflation as part of a broader segment on administration efforts to pressure companies to lower costs across the board." A White House spokesperson told the outlet that Biden "will continue to call out rip-offs such as shrinkflation, greedflation, and price gouging."

You'll note that, up there in the first sentence, I acknowledged that shrinkflation is annoying. It is, and polls show that consumers are indeed put off by the practice. Even Cookie Monster is upset about it. There are reasons to believe this is, on some level, a politically savvy move by the White House that reflects whatever data it's gleaned from polling.

But Biden's economically illiterate attempts to pin shrinkflation on greedy corporations aren't telling even half of the story. Here are three things to keep in mind when Biden starts spouting off tonight.

First, shrinkflation is just inflation.

It's not a side effect of inflation or a consequence of inflation. It is inflation. So when Biden, or anyone else, is complaining about this, what they are really saying is, "Wow, it sure sucks that your money doesn't buy as much stuff as it used to." Maybe that can score Biden some points for looking like he shares the concerns of regular Americans—even though he hasn't had to worry about a household grocery budget in decades—but this is nothing more than an attempt at rhetorical misdirection.

Second, shrinkflation is not a new phenomenon (because it is no different from inflation, which has also been around for as long as people have been using money).

Corporations didn't suddenly get more greedy and they didn't discover the tradeoff between sizes and prices in the wake of surging inflation during 2022. In fact, shrinkflation has been around since before there were corporations.

"Whenever grain was in short supply in feudal Europe, bakers had two choices: They could either raise prices or sell smaller loaves. They chose the latter," wrote Keith Plocek in Slate in 2022. "To do otherwise would violate the widely-held principle of a "just price"—formulated by Thomas Aquinas in the 13th century—and invite a bread riot."

That famous business school story about American Airlines saving a ton of money by removing a single olive from the salads it served to passengers in the 1980s? That's shrinkflation! What about Chock full o'Nuts deciding to sell 13-ounce packages of coffee instead of one-pound containers, thus ushering in an industrywide change? Shrinkflation! This is neither a novel idea nor a particularly sinister one, and it is certainly not something that needs to be regulated by the federal government.

Finally, Biden's proposed solution to shrinkflation would automatically cause prices to rise.

We don't yet know exactly what Biden is going to suggest at tonight's speech, but it seems likely that he'll tout a new task force launched this week meant to combat "unfair and illegal" pricing. On Tuesday, Biden announced the joint project of the Federal Trade Commission and Department of Justice with the goal of "making sure corporations are held accountable when they try to rip off Americans."

It's worth asking: What would happen if this task force succeeds? Assume every company in America decides to immediately undo any reductions in the size or quantity of products. What would happen to prices?

"In an inflationary environment, firms must decide whether to raise their headline prices or trim product sizes," wrote Ryan Bourne, an economist at the libertarian Cato Institute. "Banning 'shrinkflation' is effectively a mandate to raise package prices, rather than pursuing a size‐price bundle that some (particularly low‐income) consumers might prefer."

To put it in terms even Cookie Monster might understand: If the cost of making a single cookie has increased—because the flour and sugar are more expensive, and the workers making the cookies are making higher wages—then the cost of a package of 20 cookies will increase accordingly. If you want to avoid raising prices, you might only sell 15 cookies per package.

But if the government mandates 20 cookies per package—such an incredibly silly thing to have the federal government regulate, it's worth noting—then the price of that bag of cookies is certainly going up. The inflation that's occurred over the past few years can't be wiped away with a White House edict or canceled by a new task force.

As Dean Baker, a senior economist at the progressive Center for Economic and Policy Research, toldPolitico this week: "Costs have gone up—wages are 20 percent higher than they were in 2019….We're not going to have a world where people get to keep their 20 percent pay increases and pay what they did four years ago for food."

Bizarrely, Biden's attempt to change the conversation away from inflation involves a set of policies that would make Americans even more aware of how inflation is affecting them. The White House should be careful what it wishes for.

America is celebrated for its economic dynamism and ample and generously paid employment opportunities. It's a nation that attracts immigrants from around the world. Yet Americans are bummed, and have been for a while. They believe that life was better 40 years ago. And maybe it was on some fronts, but not economically. Surveys repeatedly demonstrate that Americans view today's economy in a negative light. Seventy-six percent believe the country

America is celebrated for its economic dynamism and ample and generously paid employment opportunities. It's a nation that attracts immigrants from around the world. Yet Americans are bummed, and have been for a while. They believe that life was better 40 years ago. And maybe it was on some fronts, but not economically.

Surveys repeatedly demonstrate that Americans view today's economy in a negative light. Seventy-six percent believe the country is going in the wrong direction. Some polls even show that young people believe they'll be denied the American dream. Now, that might turn out to be true if Congress continues spending like drunken sailors. But it certainly isn't true based on a look back in time. By nearly all economic measures, we're doing much better today than we were in the 1970s and 1980s—a time most nostalgic people revere as a great era.

In a recent article, economist Jeremy Horpedahl looked at generational wealth (all assets minus all debt) and how today's young people are faring compared to previous generations. His findings are surprising. After all the talk about how Millennials are the poorest or unluckiest generation yet, Horpedahl's data show them with dramatically more wealth than Gen Xers had at the same age. And this wealth continues to grow.

What about income? A new paper by the American Enterprise Institute's Kevin Corinth and Federal Reserve Board's Jeff Larrimore looks at income levels by generation in a variety of ways. They find that each of the past four generations had higher inflation-adjusted incomes than did the previous generation. Further, they find that this trend doesn't seem to be driven by women entering the workforce.

That last part matters because if you listen to progressives and New Right conservatives, you might get a different story: that today's higher incomes are only due to the fact that both parents must now work in order for a family to afford a middle-class lifestyle. They claim that supporting a family of four on one income, like many people did back in the '70s and '80s, is now impossible. Believing this claim understandably bums people out.

But it's not true. One of its many problems, in addition to the data evidence provided by Corinth and Larrimore, is that it mistakenly implies that single-income households were the norm. In fact, as early as 1978, 50 percent of married couples were dual earners and just 25.6 percent relied only on a husband's income. I also assume that there are more dual-income earners now than there were in the '80s. While this may in fact be true for married couples (61 percent of married parents are now dual-earners), because marriage itself has declined, single-earner families have become relatively more common.

Maybe the overall morosity on the economy has to do with the perception that it's more expensive to raise a family these days than it used to be. Another report by Angela Rachidi looks at whether the decline in marriage, fertility, and the increase in out-of-wedlock childbirths are the result of economic hardship. She finds that contrary to the prevailing narrative, "household and family-level income show growth in recent decades after accounting for taxes and transfers." Not only that, but "the costs of raising a family—including housing, childcare, and higher education costs—have not grown so substantially over the past several decades that they indicate an affordability crisis."

So, what exactly is bumming people out? We may find an answer in the 1984 Ronald Reagan campaign ad commonly known as "Morning in America." It begins with serene images of an idyllic American landscape waking up to a new day. It features visuals of people going to work, flags waving in front of homes, and ordinary families in peaceful settings. The narrator speaks over these images, detailing improvements in the American condition over the past four years, including job creation, economic growth, and national pride.

I believe this feeling is what people are nostalgic about. It seems that they are nostalgic about a time when America was more united and it was clearer what being American meant. Never mind that this nostalgia is often based on an incomplete and idealized memory of an era that, like ours, was not perfect.

This is a serious challenge that we need to figure out how to address. One thing that won't help, though, is to erroneously claim that people were economically better off back then and call on government to fix an imaginary problem.

Inflation stressing you out? Making you wish you had just a touch of nicotine in your system? Unfortunately, that'll cost a lot. While prices economywide have risen 3.1 percent in the last year, cigarette prices have jumped 8 percent. On top of federal and state taxes that often make up half the price of a pack, tobacco companies tend to raise their prices faster than inflation to make up for declining sales volume. These and the rest of the numb

Inflation stressing you out? Making you wish you had just a touch of nicotine in your system? Unfortunately, that'll cost a lot. While prices economywide have risen 3.1 percent in the last year, cigarette prices have jumped 8 percent. On top of federal and state taxes that often make up half the price of a pack, tobacco companies tend to raise their prices faster than inflation to make up for declining sales volume. These and the rest of the numbers in the Reason Sindex use data from November 2023.

{kind=link}