In her first economic policy speech as the 2024 Democratic presidential nominee, Kamala Harris rightly criticized Donald Trump for favoring steep tariffs, saying her Republican opponent "wants to impose what is, in effect, a national sales tax on everyday products and basic necessities that we import from other countries." But in the same speech, Harris pitched a half-baked idea that is just as economically dubious, promising to crack down on "pr

In her first economic policy speech as the 2024 Democratic presidential nominee, Kamala Harris rightly criticized Donald Trump for favoring steep tariffs, saying her Republican opponent "wants to impose what is, in effect, a national sales tax on everyday products and basic necessities that we import from other countries." But in the same speech, Harris pitched a half-baked idea that is just as economically dubious, promising to crack down on "price gouging" by the grocery industry.

That proposal is so misguided that it provoked undisguised skepticism from mainstream news outlets such as CNN, the Associated Press, The New York Times, and The Washington Post, along with criticism by Democratic economists. It showed that Harris joins Trump in pushing populist prescriptions that would hurt consumers in the name of sticking it to supposed economic villains.

"If your opponent claims you're a 'communist,'" Post columnist Catherine Rampell suggested, "maybe don't start with an economic agenda that can (accurately) be labeled as federal price controls." Harvard economist Jason Furman, who chaired President Barack Obama's Council of Economic Advisers, was equally scathing.

"This is not sensible policy, and I think the biggest hope is that it ends up being a lot of rhetoric and no reality," Furman told the Times. "There's no upside here, and there is some downside."

That downside stems from any attempt to override market signals by dictating prices. High prices allocate goods to consumers who derive the greatest value from them, encourage producers to expand supply, and spur competition that helps bring prices down.

Without those signals, you get hoarding and shortages. This is not some airy-fairy theory; it reflects bitter experience since ancient times with interventions like the one Harris proposes.

Consider what happened when President Richard Nixon imposed wage and price controls in the 1970s. "Ranchers stopped shipping their cattle to the market, farmers drowned their chickens, and consumers emptied the shelves of supermarkets," Daniel Yergin and Joseph Stanislaw note in their 1998 book on the rise of free markets.

Or consider what happened more recently with eggs. Thanks to avian flu, Furman noted, "egg prices went up last year" because "there weren't as many eggs," but the high prices encouraged "more egg production." If federal regulators had tried to suppress egg prices, they would have short-circuited that market response.

Harris, of course, says she would target only unjustified price increases, the kind that amount to "illegal price gouging" by "opportunistic companies." But as she emphasizes, there currently is no such thing under federal law, and any attempt to define it would be plagued by subjectivity and a lack of relevant knowledge.

The fact that Harris pins the sharp grocery price inflation of recent years on corporate greed suggests that her judgment about such matters cannot be trusted. Economists generally rate other factors—including the war in Ukraine as well as pandemic-related supply disruptions, shifts in consumer demand, and stimulus spending—as much more important.

High profits, in any event, are another important signal that encourages investment and competition. By forbidding "excessive profits," Harris' proposed price policing would undermine the motivation they provide.

According to the most recent numbers, the annual inflation rate dropped below 3 percent as of July. With inflation cooling, this might seem like a strange time for Harris to resuscitate an idea that was already proving disastrous thousands of years ago. But as the Timesnotes, her message "polls well with swing voters."

The broad tariffs that Trump favors, which Harris condemns as "a national sales tax" that would "devastate Americans," also poll well in the abstract. But they are popular only until voters consider the consequences.

In a recent Cato Institute survey, for example, 62 percent of respondents favored a tariff on "imported blue jeans," but that number plummeted when they were asked to imagine the resulting price increases. Harris likewise is counting on voters who like what she says but do not contemplate what it would mean in practice.

Unsurprisingly, as the reigning World Cup champions, soccer is deeply embedded in Argentina's national identity. Players on the national team are praised as heroes by everyone, from die-hard fans to casual observers. Their trophies bring joy and a sense of triumph to a country that has seen much division and gloom in recent decades. Sadly, recent victories could be the last blaze of a dying fire. Soccer (or as we call it, fútbol) in Argentina is

Unsurprisingly, as the reigning World Cup champions, soccer is deeply embedded in Argentina's national identity. Players on the national team are praised as heroes by everyone, from die-hard fans to casual observers. Their trophies bring joy and a sense of triumph to a country that has seen much division and gloom in recent decades.

Sadly, recent victories could be the last blaze of a dying fire. Soccer (or as we call it, fútbol) in Argentina is in decline, exploited by nefarious interests—but President Javier Milei has a plan.

Until recently, domestic soccer clubs in Argentina had to be operated as nonprofits. An executive branch decree changed that, allowing clubs to become publicly traded companies. The change may spur lifesaving investment into Argentine soccer.

For fans of Argentina's national team and domestic league, this is good news.

Consider how many players are leaving Argentina to play elsewhere. In 2022, 5,000 Argentines were playing abroad, most of whom were promising players under the age of 20. Even among the 26 players on the World Cup-winning roster, only one came from a club in the Argentine league. The Argentine Football Association (AFA) is worried that players who start their careers overseas will choose not to represent their national team in international competitions. Even Lionel Messi, a dual national, was tempted to play for the Spanish national team before choosing to play for Argentina. AFA lives in constant fear of having a future world champion slip through their fingers.

What's causing this exodus of talent? While part of it is Argentina's general economic malaise, some, including Spanish La Liga President Javier Tebas, point a finger at AFA's narrow-minded refusal to allow private investment in the national soccer market. Tebas has said the Argentine team won the 2022 World Cup "despite AFA" because their players "were forged in European clubs."

Milei's reforms mean international companies could buy and sell teams, or invest in Argentina's striving clubs. An injection of foreign capital would be a boon not just to the clubs who'd be able to improve their capabilities and keep talented players at home, but also to the Argentine economy overall, as clubs expand and create more jobs with their newfound capital.

AFA leaders and some major teams denounced the reforms as a "privatization of football"—and if you know how the clubs currently work, it's easy to understand their resistance.

In Argentina, soccer clubs are more than just sports teams. A club is like a church, a provider of all manner of cultural and educational services, a place for communities to share, for families to enroll their children and invest in their future—every young player's dream is to go pro and pay back his parents' sacrifice. While the clubs are already private nonprofits—an organizational model they're very defensive about—in reality, they are run by politicians, celebrities, and businessmen who use them to promote their public image. They keep governance opaque, convoluted, and unaccountable, cementing their power by making deals with barra bravas, powerful hooligan organizations that handle their illegal activities and intimidate opponents into silence—both within the clubs and in electoral politics.

Revenue from the domestic soccer league, such as TV rights money, is dispensed in a pyramid scheme with AFA President Claudio Tapia at the top, doling out favors to keep the clubs economically dependent. About 97 percent of clubs have, at some point, been on the brink of bankruptcy. This causes a vicious cycle: Teams in the league can't afford to keep promising players, who leave for foreign teams with deeper pockets, so the teams perform worse and earn less revenue.

In the late 1990s, Racing Club, one of the historic "Big Five" clubs, went bankrupt and was nearly liquidated. AFA authorized a special rescue plan that allowed insolvent clubs to contract private firms as management in exchange for financial salvage, copying previous experiences of successful entrepreneurial partnerships. Despite the plan's limited scope and the familiar cry of "veiled privatization," it performed so well that several clubs started contracting out their assets and are now faring consistently better than the rest. Meanwhile, fans remain involved by exercising oversight over contractors.

In a microcosm of national politics, mafiosos and oligarchs use populist rhetoric to entrench themselves in power, and then call the private sector to bail them out when reality catches up. In soccer, it's catching up again. Investment is still limited, the player pool is shrinking, clubs are chronically indebted and their services are becoming impoverished and exclusionary. Meanwhile, they're still run by a powerful few but lack transparency or efficiency. A country that's practically synonymous with fútbol should be attracting money and talent from all over the world, not scaring it away. A few conglomerates have expressed interest in Milei's reform, but he'll have to get past attempts at judicial obstruction and silencing of internal dissent by the AFA establishment.

Argentina is the birthplace of many stars in soccer history, but its clubs are suffering from economic stagnation. The private sector can help Argentines reclaim their clubs as social spaces and as points of national pride. Milei's reforms are an opportunity for soccer to become part of the nation's economic recovery. The profit motive, social ethics, and political will of those who love the sport can lead to even more glory.

After all the talk of abortion rights, protecting democracy, and how "fun" Vice President Kamala Harris apparently is, the first night of the Democratic National Convention culminated with a celebration of President Joe Biden's four years in office. Biden "recovered all those millions of jobs that [Donald] Trump watched slip away," Sen. Dick Durbin (D–Ill.) declared. Biden "rebuilt the economy" after the pandemic put it "flat on its back," intone

After all the talk of abortion rights, protecting democracy, and how "fun" Vice President Kamala Harris apparently is, the first night of the Democratic National Convention culminated with a celebration of President Joe Biden's four years in office.

Biden "recoveredallthosemillionsofjobsthat [Donald] Trumpwatchedslipaway," Sen. Dick Durbin (D–Ill.) declared. Biden "rebuilt the economy" after the pandemic put it "flat on its back," intoned Sen. Chris Coons (D–Conn.), a longtime Biden stan.

Biden himself put the cherry on top. "We'vehadone of the mostextraordinaryfouryearsofprogressever," the president said. "We gone from economic crisis to the strongest economy in the entire world," he claimed, pointing to job creation figures, economic growth, higher wages, and "inflation down, way down, and continuing to go down."

If so, someone should probably tell Vice President Kamala Harris about all that.

Just four days ago, Harris outlined plans for gigantic government interventions in the economy, including price controls. In what was billed as the first major policy speech of her hastily assembled campaign, Harris promised to implement the "first-ever federal ban on price gouging on food and groceries" and to take other actions to empower the federal government to "bring down costs." (There's been some debate in the days since her speech about whether it is fair to say Harris has called for price controls, but economist Brian Albretch has laid out clearly why she in fact did, writing that "any policy that gives the government the power to decide what price increases are 'fair' or 'unfair' is effectively a price control system. It doesn't matter if you call it 'anti-gouging,' 'fair pricing,' or 'consumer protection'—the effect is the same. When bureaucrats, not markets, determine acceptable prices, we're dealing with price controls.")

There has been a lot written already about why price controls are a terrible idea, and more will be written in the days ahead. For now, let's take a moment to appreciate the head-spinning logic that Biden and Harris are asking voters to accept: that America's economy is stronger than ever—but is also in need of radical government action to substitute the wisdom of bureaucrats for the market's power to determine prices.

Price controls are not a policy people reach for when things are going great. Governors don't go around threatening businesses with prosecution for price gouging when there's not a hurricane or other natural disaster happening. The Soviet Union didn't implement price controls because everyone was wealthy and well-fed. Neither did Venezuela.

But that's what Harris doing. On Friday, she promised "harsh penalties" on businesses that engage in whatever she (or her administration) determines to be "price gouging" or the collection of "excessive" profits—even though her campaign has yet to explain how she would determine those things.

Harris' promise to combat high grocery prices was made just hours after the White House Chief Economic Advisor Jared Bernstein was standing in front of reporters and touting how low grocery price inflation has been: "This morning, it was about 1 percent year over year," he said at a press briefing on Wednesday. "And there are a number of items within there where we actually have deflation, falling prices of some groceries."

Did someone tell Harris?

In part, this confusion probably stems from the unusual situation that Harris' campaign finds itself. She is, for all intents and purposes, the incumbent candidate in the race, despite not being the sitting president. And she's running against another quasi-incumbent in former President Donald Trump. Typically, incumbents try to push the message that everything is going well, or at least getting better, while challengers say everything sucks and promise to make it better.

With voters discontented with the state of the economy, both Trump and Harris are trying to distance themselves from the mess they each had a hand in creating. But Democrats can't go all-in on "everything sucks" for the obvious reason that Biden, the actual incumbent, is a Democrat.

The actual economic signals are a mixed bag right now. Unemployment has ticked up, raising fears of a possible recession on the horizon. High interest rates have replaced high inflation, which means many Americans are still feeling a squeeze on their personal finances. Biden doesn't deserve the applause he's getting, but there's also not a crisis that would demand the sort of radical actions Harris is proposing, even if the actions she's proposing really worked.

And of course, those high prices are largely the fault of government overspending (backed by heavy borrowing) during and after the pandemic. If Harris wants to put controls on something that would actually provide relief to Americans, she should aim to restrict government borrowing rather than grocery store prices.

Instead, it looks like Democrats have settled on the idea that Biden saved the economy and now Harris is here to clean up the mess—and they're just hoping no one thinks too hard about it.

By the way, you don't have to break your brain trying to make sense of this. It's far easier simply to remember that presidents don't run the economy and shouldn't get credit and/or blame for every single economic indicator. (Though they can certainly influence events, as we'll see if Harris gets her way and implements some form of federal price controls.)

But if nothing else, this Democratic cognitive dissonance creates a fun game for the next three nights of the convention: Will the speakers keep telling us that America's economy is stronger than ever, or that the country is in a crisis and Harris needs to be our price-setter-in-chief?

In this week's The Reason Roundtable, editors Peter Suderman, Katherine Mangu-Ward, and Nick Gillespie welcome special guest Ben Dreyfuss onto the pod ahead of this week's Democratic National Convention in Chicago to talk about Kamala Harris' truly terrible economic policy proposals. 02:48—Dreyfuss' YIMBY conversion thanks to Reason 13:20—Harris drops some lousy economic policy ideas. 32:37—The DNC begins. 44:25—Weekly Listener Question 53:33—Tar

In this week's TheReason Roundtable, editors Peter Suderman,Katherine Mangu-Ward, and Nick Gillespie welcome special guest Ben Dreyfuss onto the pod ahead of this week's Democratic National Convention in Chicago to talk about Kamala Harris' truly terrible economic policy proposals.

02:48—Dreyfuss' YIMBY conversion thanks to Reason

13:20—Harris drops some lousy economic policy ideas.

Send your questions to [email protected]. Be sure to include your social media handle and the correct pronunciation of your name.

Today's sponsors:

Lumen is the world's first handheld metabolic coach. It's a device that measures your metabolism through your breath. On the app, it lets you know if you're burning fat or carbs, and it gives you tailored guidance to improve your nutrition, workouts, sleep, and even stress management. All you have to do is breathe into your Lumen first thing in the morning, and you'll know what's going on with your metabolism, whether you're burning mostly fats or carbs. Then, Lumen gives you a personalized nutrition plan for that day based on your measurements. You can also breathe into it before and after workouts and meals, so you know exactly what's going on in your body in real time, and Lumen will give you tips to keep you on top of your health game. Your metabolism is your body's engine—it's how your body turns the food you eat into fuel that keeps you going. Because your metabolism is at the center of everything your body does, optimal metabolic health translates to a bunch of benefits, including easier weight management, improved energy levels, better fitness results, better sleep, etc. Lumen gives you recommendations to improve your metabolic health. It can also track your cycle as well as the onset of menopause, and adjust your recommendations to keep your metabolism healthy through hormonal shifts, so you can keep up your energy and stave off cravings. So, if you want to take the next step in improving your health, go to lumen.me/ROUNDTABLE to get 15 percent off your Lumen.

Qualia Senolytic: Have you heard about senolytics yet? It's a class of ingredients discovered less than 10 years ago, and it's being called the biggest discovery of our time for promoting healthy aging and enhancing your physical prime. Your goals in your career and beyond require productivity. But let's be honest: The aging process is not our friend when it comes to endless energy and productivity. As we age, everyone accumulates "senescent" cells in their body. Senescent cells cause symptoms of aging, such as aches and discomfort, slow workout recoveries, and sluggish mental and physical energy associated with that "middle age" feeling. Also known as "Zombie Cells," they are old and worn out and not serving a useful function for our health anymore, but they are taking up space and nutrients from our healthy cells. Much like pruning the yellowing and dead leaves off a plant, Qualia Senolytic removes those worn-out senescent cells to allow for the rest of your cells to thrive in the body. Take it just two days a month. The formula is non-GMO, vegan, and gluten-free, and the ingredients are meant to complement one another, factoring in the combined effect of all ingredients together. Resist aging at the cellular level and try Qualia Senolytic. Go to Qualialife.com/ROUNDTABLE for up to 50 percent off and use code ROUNDTABLE at checkout for an additional 15 percent off. For your convenience Qualia Senolytic is also available at select GNC locations near you.

It's OK to calm down about the economy. Yes, Friday's unemployment news was bad. Yes, the NASDAQ and Dow Jones neared correction territory on Friday morning. And yes, the Sahm Rule Recession Indicator has now been triggered. Odds are, though, a recession is not imminent. Here are three reasons why, in descending order of optimism. One, recent growth has been strong. Two, the economy has been near full employment for a while, and some kind of job

Here are three reasons why, in descending order of optimism. One, recent growth has been strong. Two, the economy has been near full employment for a while, and some kind of job growth slowdown is almost inevitable. Three, we're past the window where Federal Reserve actions can influence the election, though its recent behavior is still worrying.

Last week, the media's manic mood swing was on the exuberant side from news of a strong 2.8 percent gross domestic product (GDP) growth in the second quarter of 2024, which ended on June 30. This was a surprise improvement on the previous quarter's 1.4 percent growth. A normal reading is around 2 percent. Better, most of that growth was in the private sector, especially in consumer spending and inventory investment.

The current quarter's GDP growth estimate will come out on October 30. It would take a drastic swing to move from 2.8 percent to negative in just one quarter, though it has happened before. It typically takes two consecutive quarters of negative growth for the National Bureau of Economic Research to declare a recession, though its official standard is to call it as they see it.

The unemployment rate went up from 4.1 percent in June to 4.3 percent in July. June's reading snapped a 30-month streak of unemployment at or under 4 percent. This was the longest such streak since the 1960s.

For context, anything under 5 percent is considered pretty good. The eurozone's unemployment rate is currently 6 percent and often tops 10 percent, even in good times.

When an economy is essentially at full employment, a slowdown in job growth isn't necessarily cause for worry. The economy still has 8 million job openings, and the labor force still grew by 114,000 jobs. That annualizes to more than a million more jobs per year.

That is slower than population growth, which isn't ideal. The labor force participation rate is also still below prepandemic levels. But a sane immigration policy combined with labor reforms like loosening occupational licensing requirements would fill more of those job openings while creating more opportunities for workers who are still outside the labor force.

The Federal Reserve's recent actions spark some worry. The Fed has spent the last two-and-a-half years walking back its panicked overreaction to COVID-19, which caused high inflation in the first place, along with a bipartisan deficit spending explosion. Inflation is finally slowing and getting back close to its 2 percent target, down from its 9.2 percent peak.

The trouble is that Fed Chairman Jerome Powell indicated that the Fed will stop focusing solely on inflation and will now pay attention to the labor market as well. The Fed has a dual mandate that tasks it with both keeping inflation low and keeping employment high. These can contradict each other, as Powell might soon find out.

If unemployment continues to worsen, look for the Fed to counteract that with stimulus in the form of interest rate cuts and monetary expansion. The tradeoff to this stimulus is higher inflation—exactly what the Fed has been fighting.

While an expected interest rate cut in September isn't a big deal by itself, if it's the start of a larger stimulus campaign, any short-term economic boost will come at the cost of a slowdown later.

The Fed's actions have lag times ranging from about six months to 18 months, so anything it does now will not impact the election. This is good news for the Fed's independence, but it does not inspire faith in Powell's commitment to fighting inflation. It would be better for the Fed to stay focused on inflation. Monetary policy is a poor tool for job creation. Entrepreneurs have a much better track record.

As usual, the big picture is a mix of short-term pessimism and long-term optimism. Whether or not the current recession doommongering comes true, the long-term trend of increasing superabundance will hold. That's as good a reason for calm as any.

The first domino: A bad U.S. economic outlook, reflected in Friday's jobs report, helped prompt major stock sell-offs globally over the weekend. "Japanese stocks collapsed on Monday in their biggest single day rout since the 1987 Black Monday sell-offs," reports Reuters, with the Nikkei 225 index falling 12.4 percent and the Topix index falling 12.2 percent. The Kospi index in South Korea fell more than 10 percent. Equity markets felt the pain in

The first domino: A bad U.S. economic outlook, reflected in Friday's jobs report, helped prompt major stock sell-offs globally over the weekend.

"Japanese stocks collapsed on Monday in their biggest single day rout since the 1987 Black Monday sell-offs," reports Reuters, with the Nikkei 225 index falling 12.4 percent and the Topix index falling 12.2 percent. The Kospi index in South Korea fell more than 10 percent. Equity markets felt the pain in Taiwan, Australia, Singapore, Hong Kong, and China, though to a lesser degree. "At one point, the plunge in Japanese and Korean stocks tripped a 'circuit breaker' mechanism that halts trading to allow markets to digest large fluctuations," reportsThe New York Times. "But even after those mandatory breathers, the sell-off in stocks seemed to accelerate. Jitters spread to the debt market, prompting a halt in trading in Japanese government bonds as well."

Wall Street's "fear gauge"—the VIX—jumped to its highest level since 2020, when the pandemic prompted a wild market fluctuation. "The market response is a reflection of the deteriorating U.S. economic outlook," Jesper Koll, a director at financial services firm Monex Group, told the Times. "It was a New York sneeze that forced Japanese pneumonia."

The U.S. jobs report, released Friday, found that hiring slowed significantly in July. Unemployment continued its slow creep upward—4.3 percent, the highest since October 2021—and wage growth eased a bit. The jobs report also revised the May and June numbers downward, by a combined 29,000 jobs, indicating that the July downshift did not come out of nowhere. It also "stoked fear of a coming recession" due to something known as the "Sahm Rule," named for economic Claudia Sahm, who identified in 2019 a useful recession indicator that our July jobs report has unfortunately met (more on that from Reason's Eric Boehm).

Inflation has showed plenty of signs of cooling a bit, responding to Federal Reserve rate hikes, but the jobs report means a rate cut "could be on the table" as soon as September, according to Fed Chair Jerome Powell.

In other words, the aspirational "soft landing"—a cooling down of inflation without triggering a recession—may not in fact be materializing. And these American warning signs are leading to global ripple effects.

Bloomberg's Joe Weisenthal has, I think, the smartest and most concise take on what's going on, for those who indulge:

10 THOUGHTS ON TODAY'S BIG MARKET SELOFF

In today's 5 Things newsletter, I jotted down a bunch of random stuff about this moment in stocks, crypto, FX, and macro.

Here they are

1) It was clear instantly on Wednesday that Powell was going to be offsides this market: pic.twitter.com/iJ6ipo7Grc

Scenes from New York: Will Rudy Giuliani's real estate save him?

QUICK HITS

The U.S. government believes Iran and Hezbollah will retaliate against Israel for the recent assassinations of Hamas leader Ismail Haniyeh in Tehran and Hezbollah leader Fuad Shukr in Beirut.

Per tabloid reporting, which was partially confirmed by the campaign, Kamala Harris' husband, Doug Emhoff, had an affair during his first marriage (not to Harris). The woman he had an affair with allegedly became pregnant and did not keep the baby, though the campaign has not acknowledged or confirmed that part.

"Belgium's Olympic committee announced Sunday that it would withdraw its team from the mixed relay triathlon at the Paris Olympics after one of its competitors who swam in the Seine River fell ill," reports the Associated Press. "After a spring with an abnormal amount of rainfall, tests of the river's water found that the levels of E. coli bacteria were more than 20 times higher than what World Triathlon considers acceptable," wroteReason's Natalie Dowzicky last week. "But the mayor of Paris, Anne Hidalgo, still jumped into the Seine earlier this month in an effort to instill confidence that the waterway was just fine. But a small dip is very different from submerging yourself for hours of racing."

This is the most French possible thing that could have happened when Paris hosted the Olympics:

Running with a really stupid idea because it sounds cool, then somehow ending up fucking over the Belgians. https://t.co/K6Id4CUVV5

https://dts.podtrac.com/redirect.mp3/chrt.fm/track/35917C/d2h6a3ly6ooodw.cloudfront.net/reasontv_audio_8281110.mp3 1x 1.1x 1.25x 1.5x 2x 3x :15 :15 Download Glenn Loury: Tales of Sex, Drugs, and Capitalism "All you need, besides the cocaine, is a lighter, water, baking soda, some Q-Tip

"All you need, besides the cocaine, is a lighter, water, baking soda, some Q-Tips, high-proof alcohol, a ceramic mug, and a piece of cheesecloth or an old T-shirt," writes Glenn Loury in his riveting Late Admissions: Confessions of a Black Conservative. The book is surely the only memoir by an Ivy League economist that includes a recipe for crack cocaine along with technical discussions of Karl Marx, Ludwig von Mises, Friedrich Hayek, and Albert O. Hirschman.

Born in 1948 and raised working class on Chicago's predominantly black South Side, Loury tells a story of self-invention, ambition, hard work, addiction, and redemption that channels Benjamin Franklin's Autobiography, Richard Wright's Native Son, Saul Bellow's The Adventures of Augie March, and Milton Friedman's Capitalism & Freedom. An alternative title might have been "Rise Above It!," the slogan of a pyramid-scheme cosmetics company on which he squandered his savings as a young man in Chicago.

Now a chaired professor at Brown University and the host of The Glenn Show, a wildly popular YouTube offering, Loury worked his way through community college, Northwestern, and a Massachusetts Institute of Technology Ph.D., became the first tenured black economist at Harvard, emerged as a ubiquitous commenter on race and class in the pages of The New Republic and The Atlantic, was offered a post in the Ronald Reagan administration, and was then publicly humiliated after affairs, arrests, and addiction all became public, threatening the end of his professional and personal life. With the support of his wife, Linda Datcher Loury (herself a highly regarded economist), Alcoholics Anonymous (A.A.), and colleagues, Loury managed to rise above it and not just rebuild his academic reputation and relationships with his children, but also gain a unique perspective on economics, individualism, and community.

Reason: When you say you are a black conservative, what does that mean?

Glenn Loury: Well, I think of a few things. One of them is thinking that markets get it right in terms of the resource allocation problem and that the planning instinct and centralized, politically controlled interference in theeconomy is suspect. Of course, there are exceptions. The general predisposition is that I like prices. I like laissez faire. AndI think the first and second fundamental theorems of welfare economics are true, that we get efficient resource allocation when we allow the interplay of self-interest. You know, classical liberal stuff.

That makes you a libertarian, not a conservative.

Well, I was going to go the Edmund Burke route. I was going to say not discarding everything that's been handed to me from the past generations. Respect for tradition, reverence for some of these things that we've been handed down. So when people can't define who's a man and who's a woman, I hold my wallet. I'm a little bit skeptical about this nouveau thing.

But the "black conservative" comes out of I think a reflex or reaction to the dilemma that we African Americans face as the descendants of slaves, a marginal population disadvantaged in various ways and struggling for equality, dignity, inclusion, freedom.

I think there's a trap in that situation: the trap of falling into a status of victim and of looking to the other, the white man, the system to raise our children and deliver us from the challenge which everybody faces of living life in good faith, of, as Jordan Peterson puts it, standing up straight with your shoulders back. Of confronting the reality that there's some stuff that nobody can do for you. This posture of dependence, these arguments for reparations, this invocation of structural and systemic [racism], when the real questions are of responsibility and role.

In your book you cover your education in economics, but it's also a memoir that traffics a lot with addiction, both with drugs and sex. Can economics explain addictive behavior and self-destructive behavior?

Well, I think of the late Gary Becker. He has a paper on addiction. And I think of George Stigler and Becker's classic paper "De Gustibus Non Est Disputandum"—about taste there can be no dispute. They do it all in terms of intertemporal preferences, where you build up a taste for certain kinds of pleasures, and you invest in them.

Did they get it right?

No, I don't think they got it right. I thought it was reductive, closed off. [It's an] "everything's going to be optimization; we just have to find the right objective function" way of looking at the world. I much prefer [game theorist and Nobel laureate] Tom Schelling's engagement with the problems of self-command, as he called it, and addiction, which was understanding the conflict within the single individual who at one point in time would want not to smoke or to use cocaine, but at another point in time would find themselves, notwithstanding their understanding that this is not good for them, being compelled to do it nonetheless, and the strategic interaction between those two types within the same person.

Some critics of capitalism say that drug addiction is the apotheosis of capitalism, that it creates a bunch of things that enslave people. But your story, in one way, is about learning self-command and control over self-destructive behaviors. Is there a larger lesson from your struggles with addiction and your ultimate triumph over it?

Yeah, A.A. saved my life. That therapeutic community, that halfway house I lived in for five months in 1988: They saved my life. I went to meetings faithfully for years. And I abstained. I was clean and sober for five years. But I eventually drifted away from the A.A. abstinence philosophy.

I did have a period where I was very religious. I was born again. This initiated during the period when I was struggling to recover from drug addiction but persisted long after I was out of the woods. It changed my perspective. The hope, the whole experience of going through rehab and what they did, it quieted me down. I started reading the Bible even before I was professing genuine religious conviction. I started memorizing passages after I began to confess some belief, going to meetings, living within myself, a kind of humility. I'm not in control. Let go and let God.

What is the work that you're most proud of as an economist?

I think my best technical paper was published in Econometrica in 1981. It's called "Intergenerational Transfers and the Distribution of Earnings." It applied what at the time were state-of-the-art technical methods in dynamic optimization and the behavior of dynamic stochastic systems to the problem of inequality. It formalized the idea that young people depend on the resources available to their parents, in part, to realize their productive potential as workers and economic agents. Investments made early in life by parents in children affect the productivity of children later in life. That productivity is also dependent on other factors beyond parental control that are random, but it depends on the resources that are available. There cannot be perfect markets to allow for borrowing forward against future earnings potential, so as to realize the investment possibilities. If a parent doesn't have the resources to fund the investment themselves, there's no place to go to borrow to get piano lessons for a kid who might develop into a virtuoso pianist.

As a consequence, inequality has resource allocation consequences. Some parents have a lot of resources; others have very little. But the kids all have comparable potential, and there's diminishing returns to investing in kids. The net result is that if you could move money from rich parents to poor parents and indirectly move investment in kids from rich families to poor families, the loss in the former would outweigh the gain in the latter.

Is that a rebuttal to the idea that you can rise above it on your own? Throughout your work you make a case that if we want a more equitable society, we have to do something to help kids whose parents don't have any resources.

I see them as two different realms of argument about human experience. On the one hand, I'm talking about how there can be market failures and incompleteness and informational impact. Illness and externalities and property rights are unclear, and things like that. And you can make arguments about a minimal role for government intervention to deal with public goods problems and environmental externality problems and perhaps market failures.

On the other hand, if I'm talking to an individual about how to live their life, about whether or not to delegate responsibility for their life to outside forces or to live in good faith, to take responsibility for what you do, that's existential, almost spiritual. It's how to be in the world as opposed to how the world works.

You're on college campuses now, and campuses are more fraught than they ever have been. Do you feel like that message has disappeared?

I think so, especially with the debate that's going on presently about the war in Gaza and the campus protests occupying spaces and setting up tents on the campus green and canceling graduations and seizing buildings and engaging in civil disobedience and whatnot.

But that all comes in the aftermath of the culture war that we've been fighting about critical race theory and diversity, equity, and inclusion. These arguments have been around for a while, and I've tended to be on the side of suspicion of the so-called progressive sentiment. There's too much focus on race and sex and sexuality as identities in the context of the university environment, where our main goal is to acquaint our students with the cultural inheritance of civilization. Their narrow focus on being this particular thing and chopping up the curriculum to make sure that it gets representative treatment feels stifling to me, especially if you let that spill over into what can be said.

The therapeutic sentiment. The kids have these sensibilities. We have to be mindful of them. We don't want to offend. We don't want anyone to be uncomfortable. No, the whole point is to make you uncomfortable. You came thinking something that was really a very superficial and undeveloped framework for thinking; I'm going to expose you to some ideas that run against that grain, and you're going to have to learn how to grapple with them. And in your maturity, you may well return to some of these, but you will do so with a much firmer sense of exactly what it is that you're affirming. I want to educate you. I don't want to placate you. I'm not here to make you feel better.

I do think there's too much reliance on system-based accounts and much less of an embrace of responsibilities that we as individuals have in our education, our politics, our social and economic lives.

What is the case against affirmative action?

The case against affirmative action: It's unfair to people who are disfavored. They didn't do anything to be in the group that you decided you wanted to put your thumb on the scale for. It has concerning incentive problems. If you belong to the favorite group, it's OK to have a B average and be in the 70th percentile of test takers. And you can get into UCLA or Stanford or Yale if you're black. But if you're white, you better have an A-minus average. And you'd better be at the 90th percentile of the test takers.

The systematic implementation of affirmative action amplifies the concerns that one might have about stigmatizing African Americans who would be presumed to be beneficiaries. This is the classic complaint of [Supreme Court Justice] Clarence Thomas, that his Yale law degree isn't worth anything because it's got an asterisk on it because of affirmative action.

There's something undignified about not being held to the same standard as other people and everybody assuming that because of the sufferings of your ancestors you're somehow in need of a special dispensation.I don't regard that as equality. You're not standing on equal ground when you're dependent upon such a dispensation. In the case of affirmative action, it's a Band-Aid. You're treating a symptom and not the underlying cause. The underlying reality is there are population differences in the express[ed] productivity of the agents in question. The African Americans, on average, are producing fewer people in relative numbers who are exhibiting these kinds of skills that your instruments of assessment are intended to measure. And if you don't remedy that problem, you're never going to get truly to equality.

Where are these population differences coming from? Is it primarily an effect of cultural change? Is it inherited differences in economic status and opportunity? Is it genetic?

I don't think it's genetic, though I can't rule out that genetics could have an effect. I'm just not persuaded by the evidence of the early childhood developmental stuff. I don't underestimate the differences in the effectiveness of primary and secondary education. This is not just race. This is race and class and geography and whatnot. I think we'd do ourselves as a society a lot of good if we were to follow the sort of wholesale reform movement in K-12, including charter schools and more competition to the union-dominated public provision sector of that part of our social economy.

But culture is a tough one. I give a lot of evidence indirectly in my memoir about the effects of culture on life experience. The culture that nurtured me coming up in Chicago had its positives. It also had its norms, values, ideals, what a community affirms as being a life well lived, how people spend their time, about parenting, things of this kind.

I read this book by two Asian sociologists, Min Zhou and Jennifer Lee, called The Asian American Achievement Paradox, and it attempts to explain, based on interview data from a couple hundred families in Southern California, how it is that these Asian communities are able to send their youngsters to places like Harvard and Stanford in such large numbers. And it basically makes a cultural argument. One of the chapters is entitled "The Asian F." It turns out that the Asian F is an A-minus, according to some of their respondents. I don't think you can discount the importance of that kind of cultural reinforcement, because at the end of the day what matters is how people spend their time.

You're a critic of race-based policies, but you also get kind of pissed when people dismiss the black experience. You say being a black American is a part of your identity. Is there a way for us to bring our individual cultural and ethnic heritage to the conversation that doesn't divide us or put us in one group or another?

We all have a story. We all have a narrative and a cultural inheritance. And yet underneath we are kind of all the same. Our struggles are comprehensible to each other, and our triumphs and our failures are things that we can relate to as human beings. And that's how we should be relating to each other.

I'm in my 70s now, and I've just written a book about my life. So who am I? What does it amount to? I'm the kid that really did grow up immersed in an almost exclusively black community on the South Side of Chicago. The music that I listened to, the food that I ate, the stories that I was told and that I told to my own children in turn. These things are related to the history, the struggles and triumphs, the dreams and hopes of African-American people. That's a part of who I am. And it annoys me when people attempt to say "get over it" to me. They're not respecting me when they tell me that race is not a deep thing about people.

It's a superficial thing, I grant you that. I grant you the melanin in the skin, the genetic markers that are manifest in my physical presentation, don't add up to very much. But the dreams of my fathers and others, the lore, the narrative about who "we" are, that's not arbitrary and it's not trivial. And it seems to me sociologically naive in the extreme to just want to move past that. That's a part of who people actually are.

But I struggle with this, because I also want to tell my students not to wear that too heavily, not to let it blinker them and prevent them from being able to engage with, for example, the inheritance of European civilization in which we are embedded. That's also your inheritance. Tolstoy is mine. Einstein is mine. And yours. I want to say to youngsters of whatever persuasion: Don't be blinkered. Don't be so parochial that you miss out on the best of what's been written and thought and said in human culture.

(Photo: Ken Richardson)

This interview has been condensed and edited for style and clarity.

A bummer of a jobs report released Friday morning triggered a sharp drop in the stock market and stoked fear of a coming recession—thanks to something known as the "Sahm Rule." So what is that? It is named after economist Claudia Sahm, who served as a top economic advisor during the Obama administration and identified a historical indicator of coming recessions in 2019: every time since 1970 that the three-month moving average of the U.S. unemplo

A bummer of a jobs report released Friday morning triggered a sharp drop in the stock market and stoked fear of a coming recession—thanks to something known as the "Sahm Rule."

So what is that?

It is named after economist Claudia Sahm, who served as a top economic advisor during the Obama administration and identified a historical indicator of coming recessions in 2019: every time since 1970 that the three-month moving average of the U.S. unemployment rate is more than half a percentage point above the lowest three-month moving average from the previous year, a recession has soon followed.

That's a bit complicated, admittedly. If you want to know what it looks like in practice, check out today's jobs report. Unemployment in July ticked upwards to 4.3 percent. Over the past three months, the average unemployment rate has been 4.13 percent. That's quite a bit higher than the lowest three-month average from the past year—which was 3.63 percent, between June and August 2023.

But the "rule" is also a set of guidelines. In the 2019 paper where Sahm identified this historical early warning system for a coming recession, she called for governments to begin distributing stimulus payments as soon as this alert was triggered. Doing so, she argued, would allow for a speedier response to a recession by eliminating the lag that occurs while politicians and other observers debate whether a recession is coming and what to do about it. Essentially, it is meant to be a technocratic solution to a recurring problem.

The political system has not adopted that approach—and thank goodness, because the federal government is $35 trillion in debt and already on pace to run a $2 trillion deficit this year. There's literally no money for stimulus checks right now.

But there's one more complicating factor. Sahm herself says this might be a false alarm.

The Wall Street Journalreports that "Sahm doesn't think the economy is on the immediate cusp of a recession. She reckons that changes in the supply of labor since the pandemic, including the recent jump in immigration, have led the Sahm rule to overstate how weak the job market is."

"We are still in a good place, but until we see signs of stabilizing, of leveling out, I'm worried," Sahm, who also worked at the Federal Reserve and is now the chief economist at New Century Advisors, an investment firm, told the Journal.

It's good to be cautious about the predictive power of historical trends. Indeed, in that 2019 paper, Sahm warned that "the Sahm rule is an empirical regularity. It's not a proposition; it's not a law of nature."

Federal Reserve Chairman Jerome Powell echoed that sentiment this week. He called the Sahm Rule "a statistical regularity" on Wednesday, adding that "it's not like an economic rule, where it's telling you something must happen." At a meeting earlier this week, the Federal Reserve decided to hold interest rates steady, though it indicated that a rate cut could be coming in September.

The official arbiter of recessions is the National Bureau of Economic Research (NBER), a private entity whose definition of a recession takes into account monthly indicators like employment, personal income, and industrial production along with quarterly gross domestic product (GDP) growth (by their terms, two consecutive quarters of negative GDP growth often, but not always, correspond with an official recession).

Still, the outlook is certainly darker after Friday's jobs report. If a recession is coming, the federal government's and Federal Reserve's ability to respond will be severely limited by the poor fiscal and monetary decisions that have left the Treasury deeply in debt and the central bank's balance sheets overstretched.

The Sahm Rule has correctly predicted every recession in the past half-century. Let's hope it got this one wrong.

Is the future of the GOP more libertarian, nationalist, or, somehow, both? Joining us today is Vivek Ramaswamy, entrepreneur, author, and former presidential candidate. He's been making a hard pitch for what he's called a "libertarian-nationalist alliance" for the past several months. He was at the 2024 Libertarian National Convention where he tried to convince libertarians to vote Republican. Reason's Zach Weissmueller also saw Ramaswamy at the

Is the future of the GOP more libertarian, nationalist, or, somehow, both?

Joining us today is Vivek Ramaswamy, entrepreneur, author, and former presidential candidate. He's been making a hard pitch for what he's called a "libertarian-nationalist alliance" for the past several months. He was at the 2024 Libertarian National Convention where he tried to convince libertarians to vote Republican. Reason's Zach Weissmueller also saw Ramaswamy at the Republican National Convention, where he was trying to convince MAGA supporters to be more libertarian. Reason's Stephanie Slade saw him make his case for "national libertarianism" at the National Conservatism Conference. That event was also attended by vice presidential candidate J.D. Vance, who has a different vision for the conservative movement. Those dueling visions are the subject of today's episode.

Note:This episode is plagued by technical issues due to a software malfunction. With the exception of an approximately nine-minute section (which is marked in the episode), the full conversation is intact.

Watch the full conversation on Reason's YouTube channel or the Just Asking Questions podcast feed on Apple, Spotify, or your preferred podcatcher.

Pictures of Vivek Ramaswamy, Donald Trump, Liz Wolfe, and Zach Weissmueller with the Reason logo, the Just Asking Questions logo, and the words "Libertarian or nationalist?" all in white

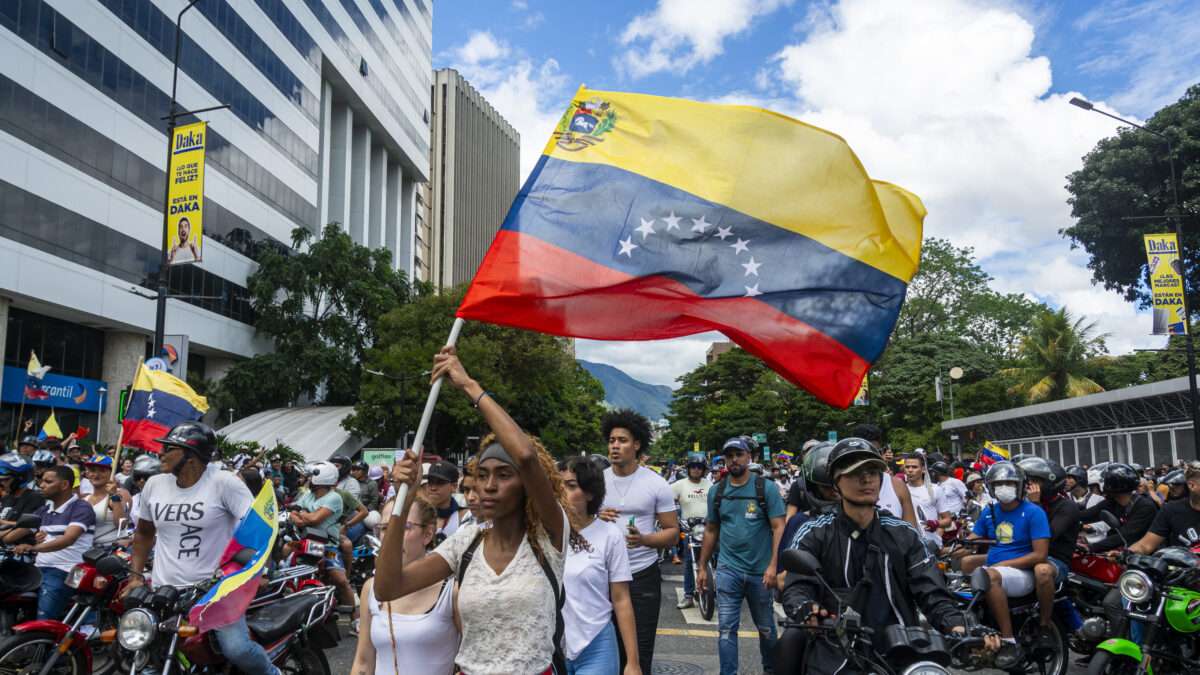

Nicolás Maduro is the authoritarian leader of Venezuela. Last weekend, he declared himself the winner of that country's presidential election—an outcome that is highly disputed; the Carter Center lambasted the Maduro regime's lack of transparency and said the process "cannot be considered democratic." Thousands of Venezuelans have taken to the streets in protest. In response, the government has implemented a crackdown, killing at least 16 people

Nicolás Maduro is the authoritarian leader of Venezuela. Last weekend, he declared himself the winner of that country's presidential election—an outcome that is highly disputed; the Carter Center lambasted the Maduro regime's lack of transparency and said the process "cannot be considered democratic."

Thousands of Venezuelans have taken to the streets in protest. In response, the government has implemented a crackdown, killing at least 16 people and detaining a thousand more. Such behavior is entirely characteristic of Maduro, an outlaw who has faced credible accusations of drug trafficking, public corruption, and crimes against humanity. His unscrupulous leadership has plunged the country into depression and poverty. As Reason's Katarina Hall wrote, "Almost 8 million Venezuelans have fled the country amid hyperinflation, shortages of essential goods, and rampant corruption. Many more have expressed their desire to leave if Maduro remains in power."

Maduro's governing ideology is not a secret: He is a socialist. He is the successor to the leftist tyrant Hugo Chávez. He heads Venezuela's ruling Socialist Party. His policy prescriptions are in line with socialism: His government has instituted price controls, seized assets from private companies, and contributed to the country's hyperinflation problem. If it walks like a duck, quacks like a duck, and wrecks the economy with a mixture of centralized planning, repression, and pure theft—well, it's a socialist duck.

So it came as something of a shock when a recentNew York Times article that correctly described Venezuela's overall problems—and Maduro's perfidy in particular—nevertheless identified the government's economic policy as "brutal capitalism" rather than socialism. Here was The Times:

If the election decision holds and Mr. Maduro remains in power, he will carry Chavismo, the country's socialist-inspired movement, into its third decade in Venezuela. Founded by former President Hugo Chávez, Mr. Maduro's mentor, the movement initially promised to lift millions out of poverty.

For a time it did. But in recent years, the socialist model has given way to brutal capitalism, economists say, with a small state-connected minority controlling much of the nation's wealth.

Economists say what now? These economists are not identified by The Times; the given hyperlink redirects to a Times article about improvements in the Venezuelan economy. These improvements were due to the introduction of some market reforms, according to economists with actual names.

"Lifting some controls does not make Venezuela a capitalist country," writes George Mason University economist Tyler Cowen. "Moreover, the lifting of controls led to improvements."

When a small state-connected minority controls much of the nation's wealth—and maintains its grip on power by outlawing dissent and cheating in elections—then the ruling ideology is socialism, almost by definition. Maduro, it bears repeating, makes no secret of this: He is the leader of the United Socialist Party of Venezuela.

Socialists will complain, as they often do, that various socialist governments are not practicing actual socialism. Under their idealized system, socialists claim, the government's centralized redistribution of resources will be fair, equal, and democratic. Yet it certainly says something about such a system that it collapses into outright tyranny every time it is attempted. Socialist governance seems to require concentrating an extraordinary amount of power in elite government decision makers; this tends to produce a new ruling class, the widespread deprivation of political rights for everyone else, and crippling poverty.

Socialism is brutal, as the people of Venezuela know perfectly well. They understand that better than The New York Times.

This Week on Free Media

Amber Duke and I discuss MSNBC's confusion over what Sen. J.D. Vance (R–Ohio) really wants, President Joe Biden's plan to pack the Supreme Court, and weird affinity groups supporting Vice President Kamala Harris. (Apologies for my hoarse voice; I had too much fun at a Green Day/The Smashing Pumpkinsconcert the night before we filmed.)

Worth Watching

Like most fans of the Marvel Cinematic Universe (MCU), I am of the opinion that things have mostly gone awry since Avengers: Endgame concluded "The Infinity Saga." (Though I enjoyed several of the post-Endgame television shows on Disney+: WandaVision, Loki, Hawkeye, and What If…?) I was thus incredibly pleased to learn that the Russo brothers—who were responsible for many of the MCU's best films, including Endgame and Infinity War—are returning to rescue the franchise. Most notably, they have enlisted a familiar face: Robert Downey Jr., who famously portrayed Tony Stark/Iron Man, the original MCU superhero who gave his life to save the universe.

Downey Jr. will not be playing Stark again, thank goodness. While there are all sorts of ways to revive the character—alternate universes, time travel, etc.—doing so would cheapen his sacrifice at the conclusion of Endgame. Instead, Downey Jr. will play Victor von Doom, a beloved villain from the Marvel comics. It seems likely that this version of Doctor Doom will have some connection to Stark; as previously mentioned, the MCU has made use (some would say overuse) of alternate realities.

In any case, the recent reveal of Downey Jr. at Comic-Con in San Diego, California, was something to behold.

You can add the Internal Revenue Service to the ranks of federal agencies conceding that raining taxpayer money on all and sundry to offset the negative effects of pandemic-era closures didn't go as well as intended. Not only was a program meant to offset the cost of paying workers during lockdowns and voluntary social-distancing prone to being gamed, but the "vast majority" of claims submitted to the program show evidence of being fraudulent. T

You can add the Internal Revenue Service to the ranks of federal agencies conceding that raining taxpayer money on all and sundry to offset the negative effects of pandemic-era closures didn't go as well as intended. Not only was a program meant to offset the cost of paying workers during lockdowns and voluntary social-distancing prone to being gamed, but the "vast majority" of claims submitted to the program show evidence of being fraudulent.

The Tax Man Is Shocked To Discover Fraudsters

In the course of a detailed review of the Employee Retention Credit, "the IRS identified between 10% and 20% of claims fall into what the agency has determined to be the highest-risk group, which show clear signs of being erroneous claims for the pandemic-era credit," the IRS announced June 20. "In addition to this highest risk group, the IRS analysis also estimates between 60% and 70% of the claims show an unacceptable level of risk."

The Employee Retention Credit was offered to businesses that were shut down by government COVID-19 orders in 2020 or the first three quarters of 2021, experienced a required decline in gross receipts during that period, or qualified as a recovery startup business at the end of 2021. But it was clear early on that scammers were taking advantage of giveaways of taxpayer money, either to claim it for themselves or to pose as middlemen helping unwitting business owners file claims.

In March of 2023, the tax agency warned of "blatant attempts by promoters to con ineligible people to claim the credit." In September of that year, it stopped processing claims amidst growing evidence that vast numbers of applications were "improper," as the IRS delicately puts it. In March 2024, the agency announced that its Voluntary Disclosure Program had recovered $1 billion (since raised to over $2 billion) in improper payouts from participants who got to keep 20 percent of the take.

Ultimately, only "between 10% and 20% of the ERC claims show a low risk" for fraud, even by generous federal standards for throwing other people's money at problems largely of government creation.

"We will now use this information to deny billions of dollars in clearly improper claims and begin additional work to issue payments to help taxpayers without any red flags on their claims," commented IRS Commissioner Danny Werfel.

As of the end of May, the IRS "has initiated 450 criminal cases, with potentially fraudulent claims worth nearly $7 billion."

There's More Fraud Where That Came From

Of course, this is only the tip of the iceberg when it comes to pandemic stimulus fraud.

In April, Attorney General Merrick Garland boasted that the COVID-19 Fraud Enforcement Task Force (yes, it's widespread enough to rate its own task force) had "charged more than 3,500 defendants, seized or forfeited over $1.4 billion in stolen COVID-19 relief funds, and filed more than 400 civil lawsuits resulting in court judgements and settlements."

Strong work. But the various pandemic stimulus bills tallied up to trillions of dollars. And a lot more than a few billion ended up in the hands of grifters.

"The total amount of fraud across all UI [unemployment insurance] programs (including the new emergency programs) during the COVID-19 pandemic was likely between $100 billion and $135 billion—or 11% to 15% of the total UI benefits paid out during the pandemic," the Government Accountability Office warned last September.

Earlier, the Small Business Administration's Inspector General found more than $200 billion stolen from the Economic Injury Disaster Loan (EIDL) program and Paycheck Protection Program (PPP). "This means at least 17 percent of all COVID-19 EIDL and PPP funds were disbursed to potentially fraudulent actors," noted the report.

With between 70 percent and 90 percent of claims for the Employee Retention Credit identified as likely scams, either the IRS is a stand-out magnet for grifters or other agencies need to return to their own investigations with a somewhat more skeptical eye.

Stimulus Fueled Inflation as Well as Fraud

It's maddening enough that the federal government is handing out vast sums of money to con artists. But Americans are contending with a 2024 economy in which the U.S. Bureau of Labor Statistics' own inflation calculator finds that it takes $124.77 to purchase what $100 bought in 2019, before anybody heard of COVID-19. Federal stimulus programs are directly to blame for much of that inflationary slippage in the dollar's buying power.

"U.S. fiscal stimulus during the pandemic contributed to an increase in inflation of about 2.6 percentage points in the U.S.," three economists with the Federal Reserve Bank of St. Louis estimated last year. The reason, they said, was that governments "injected large amounts of money into the economy"—money created from thin air to artificially pump up the economy.

"Inflation comes when aggregate demand exceeds aggregate supply," agreed economist John Cochrane of the Hoover Institution and the Cato Institute in a March piece for the International Monetary Fund. "The source of demand is not hard to find: in response to the pandemic's dislocations, the US government sent about $5 trillion in checks to people and businesses, $3 trillion of it newly printed money, with no plans for repayment."

Officials justified the stimulus as a necessary evil to offset economic collapse from often-mandatory pandemic closures by keeping demand flowing with government checks. After conceding that stimulus fueled inflation, the St. Louis Federal Reserve economists argued that massive spending likely prevented "worse outcomes despite the price pressures that may have resulted from the spending."

But officials could have refrained from issuing closure orders so the economy could function without mandated disruptions. That would have made the creation of trillions of dollars from thin air and its distribution around the country entirely beside the point. Then, grifters wouldn't have opportunity to scam hundreds of billions of dollars out of federal agencies, including the IRS.

It's nice that the IRS, like other federal agencies, is catching up with the vast fraud it enabled. But it would be better if government officials weren't constantly addressing problems they created.

The Road to Freedom: Economics and the Good Society, by Joseph E. Stiglitz, W.W. Norton & Company, 384 pages, $29.99 Joseph Stiglitz, a former chief economist of the World Bank, thinks that taxation is a precondition for freedom, not a threat to it. The current political problem, he argues in The Road to Freedom, is that the right (which for Stiglitz includes libertarians as well as conservatives) rejects the Founding Fathers' idea of no taxa

Joseph Stiglitz, a former chief economist of the World Bank, thinks that taxation is a precondition for freedom, not a threat to it. The current political problem, he argues in The Road to Freedom, is that the right (which for Stiglitz includes libertarians as well as conservatives) rejects the Founding Fathers' idea of no taxation without representation in favor of opposing any taxation at all. This is a problem, he continues, because market failures are more extensive and severe than the "neoliberals"—people like Stiglitz's fellow Nobel laureates Friedrich Hayek and Milton Friedman—would admit. For Stiglitz, redistribution and regulation are the real road to freedom.

Much of the book is devoted to criticizing neoliberals, who Stiglitz defines as proponents of "unregulated, unfettered markets." In Stiglitz's view, "a free-market, competitive, neoliberal economy combined with a liberal democracy" isn't enough—for "a stable equilibrium," we need "strong guardrails and a broad societal consensus on the need to curb wealth inequality and money's role in politics."

This book is written as though the regulatory state has not expanded since the end of World War II and as though the welfare state was dismantled in the 1980s. It is written as if liberal democracies' economic policies were all written by someone with the worldview of President Javier Milei of Argentina or the Brazilian MMA fighter Renato Moicano, who at UFC 300 proclaimed that everyone who cares about freedom should be reading the libertarian economist Ludwig von Mises. It is written as though we were still in the Lochner era, when the Supreme Court regularly struck down economic regulations.

But that is not the era we live in. Instead, the state has kept growing because neoliberalism has never reached the level of influence its adherents wanted. A more coherent argument—though still not a good one—would be that the modern state is big but should be bigger.

Nor is this book a good guide to the views of "neoliberals" like Friedman, Hayek, and Mises. No reasonable reading of these writers would suggest that they do not believe in market failures, yet Stiglitz claims that neoliberals think "markets on their own were efficient and stable."

Stiglitz also claims that "Unfettered markets designed along neoliberal principles have effectively robbed [the U.S. and U.K.] of their political freedom." One would expect an economist of Stiglitz's stature to make an effort to support this claim, yet his book offers no evidence for it. The available empirical evidence suggests that Stiglitz has it backward: It is state control of the economy that suppresses democratic freedom. There are other inconvenient empirical studies, including ones showing that the neoliberal "Washington Consensus" works fairly well and that there is no clear evidence that economic freedom leads to more inequality. (There is, however, abundant evidence that economic freedom makes us richer.)

The book does contain many reasonable ideas. Stiglitz is certainly right that the challenges associated with global fisheries, pandemics, and climate change are a fertile opportunity for more economic analysis. And the notion that market failures are both more complex and more common in an increasingly interconnected world should be a starting point for economists and policy makers.

Unfortunately, Stiglitz is too comfortable claiming that the solution to these problems is "regulation," without adding much explanation of how regulation should address such issues. Here he should have engaged more deeply with the insights of another Nobel laureate in economics, Elinor Ostrom. Stiglitz does mention Ostrom's research on the regulation of the commons—that is, of shared resources that anyone can use (and overuse, in the absence of rules governing how people can draw on them). But he sees her work as a defense of "regulation" and a critique of private property.

That wasn't what Ostrom was arguing. Rather than rail against private property, Ostrom argued that it is an empirical question as to whether private property, communal arrangements outside the state, or government control is the most appropriate way to manage the commons. And nothing in Ostrom's work implies a wide-ranging critique of private property. Her work is fully within the same classical liberal tradition that includes Hayek and Friedman.

Public goods, Ostrom argued, are not provided solely by the government. She also stressed the importance of polycentricity—of multiple levels of governance that offer opportunities for citizens and nonprofits to provide public goods, with each level able to cooperate with the others and also to act independently. This is especially useful for thinking about how to address the kinds of complex externalities Stiglitz sees as pervasive. Ostrom even developed a polycentric approach to climate change.

The call for regulation is less fundamental than asking what political arrangements give rise to the most appropriate rules, be they public, private, or communal. Elinor Ostrom and her husband, Vincent Ostrom, highlighted federalism's value as a laboratory of democracy because, like Hayek, they recognized that we do not know how to solve many pressing problems. This book would have been more convincing if instead of devoting so much time to criticizing the neoliberals (and overstating their influence), Stiglitz had spent more time exploring such insights.

Stiglitz's polemics are unlikely to change anyone's mind, but they will probably find an audience among people already predisposed to agree with them. His ideological fellow-travelers will probably like his full-throated defense of "progressive capitalism" (basically contemporary Sweden, with its combination of a generous welfare state, pro-labor policies, and a market economy). But Stiglitz does not explain why the U.S. is not like Sweden, nor how to get to Sweden from where we are now. Nor does Stiglitz note that Sweden, which ranks highly in the Heritage Foundation's Index of Economic Freedom, is rather open to policies promoted by neoliberals.

If you're interested in understanding market liberalism, there are better recent books to read, such as Peter Boettke's The Struggle for a Better World or Deirdre McCloskey and Art Carden's Leave Me Alone and I'll Make You Rich, each of which explains what classical liberals mean by freedom. If you are tempted to accept the notion that neoliberals lack a moral sense, you would especially benefit from Humanomics—by Bart Wilson and another Nobel laureate, Vernon Smith—which articulates the rich moral framework of Adam Smith's tradition. And if you want a more compelling empirical critique of capitalism, Daniel Bromley's Possessive Individualism explains how modern capitalism differs from the capitalism of even half a century ago, let alone Adam Smith's time.

But even our current, heavily regulated variety of capitalism is better than countless real-world alternatives. After all, if the situation in the U.S. were as bad as Stiglitz suggests, one would not expect so many people to want to move here. The border "crisis," which is really a problem with excessive regulation, suggests that the U.S. has pretty good institutions. Or at the very least, that people think those institutions are better than what they are leaving. And what they are leaving is less economic and political freedom.

Congressional Budget Office (CBO) projections provide valuable insights into how a big chunk of your income is being spent and reveal the long-term consequences of our government's current fiscal policies—you may endure them, and your children most certainly will. Yet, like most other projections looking into our future, these numbers should be taken with a grain of salt. So should claims that CBO projections validate anyone's fiscal track record

Congressional Budget Office (CBO) projections provide valuable insights into how a big chunk of your income is being spent and reveal the long-term consequences of our government's current fiscal policies—you may endure them, and your children most certainly will. Yet, like most other projections looking into our future, these numbers should be taken with a grain of salt. So should claims that CBO projections validate anyone's fiscal track record.

So much can and likely will happen to make projections moot and our fiscal outlook much grimmer. Unforeseen events, economic changes, and policy decisions render them less accurate over time. The CBO knows this and recently released alternative scenarios based on different sets of assumptions, and it doesn't look good. It remains a wonder that more politicians, now given a more realistic range of possibilities, aren't behaving like it.

First, let's recap what the situation looks like under the usual rosy growth, inflation, and interest rate assumptions. Due to continued overspending, this year's deficit will be at least $1.6 trillion, rising to $2.6 trillion by 2034. Debt held by the public equals roughly 99 percent of our economy—measured by gross domestic product (GDP)—annually, heading to 116 percent in 2034.

The only reason these numbers won't be as high as projected last year is that a few House Republicans fought hard to impose some spending caps during the debt ceiling debate. The long-term outlook is even scarier, with public debt reaching 166 percent of GDP in 30 years and all federal debt reaching 180 percent.

No one should be surprised. To be sure, the COVID-19 pandemic and the Great Recession made things worse, but we've been on this path for decades.

Unfortunately, if any of the assumptions underlying these projections change again, things will get a lot worse. That's where the CBO's alternative paths help. Policymakers and the public can better see the potential risks and opportunities associated with various fiscal policy choices, enabling them to make more informed decisions.

For instance, the CBO highlights that if the labor force grows annually by just 0.1 fewer percentage points than originally projected—even if the unemployment rate stays the same—slower economic growth will lead to a deficit $142 billion larger than baseline projections between 2025 and 2034. A similarly small slowdown in the productivity rate would lead to an added deficit of $304 billion over that period.

Back in 2020, the prevalent theory among those who claimed we shouldn't worry about debt was that interest rates were remarkably low and would stay low forever. As if. These guys have since learned what many of us have known for years: that interest rates can and will go up when the situation gets bad enough. So, what happens if rates continue to rise above and beyond those CBO used in its projections? Even a minuscule 0.1-point rise above the baseline would produce an additional $324 billion on the deficit over the 2025-2034 period.

The same is true with inflation, which, as every shopper can see, has yet to be defeated. If inflation, as I fear, doesn't go away as fast as predicted by CBO—largely because debt accumulation is continuing unabated—it will slow growth, increase interest rates, and massively expand the deficit. To be precise, an increase in overall prices of just 0.1 points over the CBO baseline would result in higher interest rates and a deficit of $263 billion more than projected.

Now, imagine all these variations from the current projections happening simultaneously. It's a real possibility. The deficit hike would be enormous, which could then trigger even more inflation and higher interest rates. The question that remains is: Why aren't politicians on both sides more worried than they seem to be?

What needs to happen before they finally decide to treat our fiscal situation as a real threat? President Joe Biden doesn't want to tackle the debt issue. In fact, he's actively adding to the debt with student loan forgiveness, subsidies to big businesses, and other nonsense. Meanwhile, some Republicans pay lip service to our financial crisis, but few are willing to tackle the real problem of entitlement spending.

The time for political posturing is over. The longer we wait to address these issues, the more severe the consequences will be for future generations. It's time for our leaders to prioritize the nation's long-term economic health over short-term political gains and take bold steps toward fiscal responsibility. Only then can we hope to secure a stable and prosperous future for all Americans.