Argentine authorities are working with El Salvador, a pioneering nation in bitcoin adoption, aiming to boost cryptocurrency adoption in Argentina. High-ranking officials from Argentina's National Securities Commission (CNV), the country's securities regulator, met with El Salvador's National Commission of Digital Assets on May 23 to discuss the use of cryptocurrencies, according to an official announcement by the CNV. The talks focused on El Salv

Argentine authorities are working with El Salvador, a pioneering nation in bitcoin adoption, aiming to boost cryptocurrency adoption in Argentina.

High-ranking officials from Argentina's National Securities Commission (CNV), the country's securities regulator, met with El Salvador's National Commission of Digital Assets on May 23 to discuss the use of cryptocurrencies, according to an official announcement by the CNV. The talks focused on El Salvador's experience in adopting bitcoin and its regulatory framework.

"El Salvador has emerged as one of the leading countries, not only in the use of bitcoin, but it has also stood out in the world of crypto assets. It has created a specific commission, the National Commission of Digital Assets (CNAD), and therefore has an experience that is very valuable for the CNV at this time," said Roberto E. Silva, president of the CNV.

Under President Nayib Bukele, El Salvador made history by becoming the first country to adopt bitcoin as legal tender in September 2021, using it alongside the U.S. dollar. At the same time, the country launched Chivo Wallet, a government-backed digital wallet, and gave $30 worth of bitcoin to citizens who signed up for it.

Since then, El Salvador has embarked on several ambitious projects to promote bitcoin use, including creating a bitcoin city powered by geothermal energy, issuing bitcoin bonds, and offering expedited citizenship to bitcoin investors.

To date, the country has mined 474 bitcoin and holds 5,756 bitcoin, valued at just under $400 million, according to a website that tracksEl Salvador's bitcoin portfolio. Bukele has said he plans to keep growing El Salvador's holdings by buying one bitcoin every day.

In recent years, Argentina has also seen a surge in cryptocurrency adoption as its citizens seek refuge from the peso's depreciation and soaring inflation. And since Javier Milei became president of Argentina last year, the crypto sector has seen positive developments. Just a month after Milei took office, Minister of Foreign Affairs Diana Mondino legalized the use of bitcoin for settling contracts.

"We want to strengthen ties with the Republic of El Salvador, and therefore, we are going to explore the possibility of signing collaboration agreements with them," Silva said about the recent meeting. The meeting follows a visit in March by CNV Vice President Patricia Boedo to El Salvador to discuss regulatory issues, indicating the interest of both countries in reaching some kind of agreement on crypto assets.

News of this collaboration between the two countries sent ripples through the crypto market, pushing bitcoin's value past the $70,000 mark. A formal partnership between Argentina and El Salvador could signal a major shift in Latin America's approach to digital assets, paving the way for broader crypto adoption.

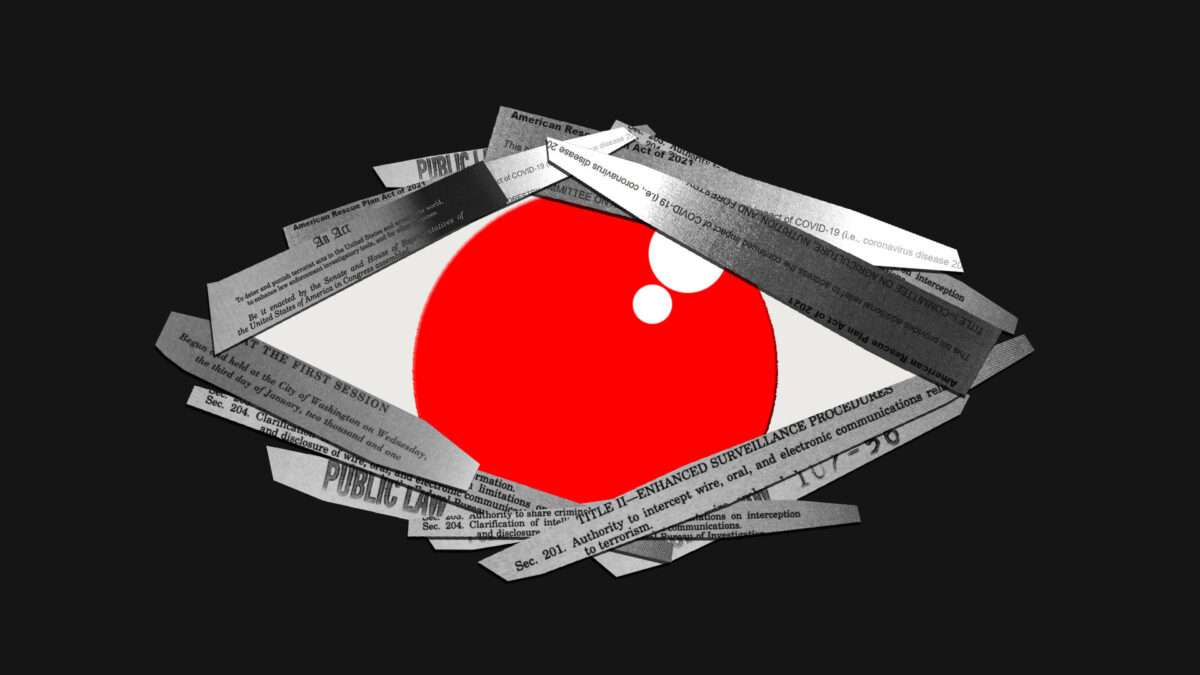

You have a 15-character password, shield the ATM as you enter your PIN, close the door when you meet with your banker, and shred your financial statements. But do you truly have financial privacy? Or has someone else been sitting silently in the room with you this whole time? While you might feel you have secured your financial information, the government has very much wedged its way into the room. Financial privacy has practically vanished over

You have a 15-character password, shield the ATM as you enter your PIN, close the door when you meet with your banker, and shred your financial statements. But do you truly have financial privacy? Or has someone else been sitting silently in the room with you this whole time?

While you might feel you have secured your financial information, the government has very much wedged its way into the room. Financial privacy has practically vanished over the last 50 years.

It's strange how quickly we have accepted the current state of financial surveillance as the norm. Just a few decades ago, withdrawing money didn't involve 20 questions about what we plan to use the money for, what we do for a living, and where we are from. Our daily transactions weren't handed over in bulk to countless third parties.

Yet, what is even stranger is that most people continue to believe in a version of financial privacy that no longer exists. They believe financial records continue to be private and the government needs a warrant to go after them. This belief couldn't be further from reality. Americans do not have financial privacy. Rather, we have the illusion of financial privacy.

Why is this? Put simply, financial surveillance has been kept hidden in three major ways: Encroachments into privacy have evolved gradually through obscure legislation, the scope of surveillance has constantly expanded through inflation, and much of the process is kept intentionally confidential.

Years of Obscure Legislative Changes

Compared to today, customers in the 1970s had far more freedom in opening accounts and interacting with their own money. Back then, the decision to transact with a bank could be based on the cash in one's pocket. Transactions were not scrutinized for threats of terrorism or drug trafficking. Customers were not legally required to supply a photo ID to set up an account. Banks decided for themselves what information they needed to set up an account, and this information remained effectively confidential between the customer and the bank.

This changed in the 1970s when a pivotal piece of legislation was passed: the Bank Secrecy Act. Stemming from concerns in Congress regarding Americans concealing their wealth in offshore accounts, the legislation aimed to gather financial information to detect such activities. For example, financial institutions were required to monitor and report transactions over $10,000 to the government.

It didn't stop there. Over the years, Congress came up with more ways to expand financial surveillance in what is now best referred to as the "Bank Secrecy Act regime."

In 1992, the Annunzio-Wylie Anti–Money Laundering Act led to the introduction of suspicious activity reports (SARs), where, instead of just reporting anything over $10,000, financial institutions had to report "any suspicious transaction relevant to a possible violation of law or regulation." Two years later, the Money Laundering Suppression Act authorized the secretary of the treasury to designate the Financial Crimes Enforcement Network (FinCEN) as the agency to oversee these reports.

Following the September 11 attacks, the USA PATRIOT Act significantly expanded surveillance powers, granting the government easier access to communication records. Hidden among the pages of this sprawling omnibus bill was a set of "know your customer" requirements that forced banks not only to investigate who you are but also to verify that information on behalf of the government.

Again, Congress didn't stop there.

Another extensive omnibus bill, the American Rescue Plan Act of 2021, quietly introduced a rule intended to surveil all bank accounts with at least $600 of activity. Luckily, the controversial measure was noticed and met with immediate pushback. The Treasury Department responded by informing people that the government already has access to much of everyone's financial information.

While the proposal was retracted, the initiative was only shut down partially. Instead of affecting all bank accounts, the law narrowed its scope to require reporting for transactions over $600 made through a payment transmitter such as PayPal, Venmo, or Cash App.

Then the 2022 Special Measures To Fight Modern Threats Act aimed to eliminate some of the checks and balances placed on the Treasury, granting it the authority to use "special measures" to sanction international transactions.

While the Special Measures To Fight Modern Threats Act hasn't been passed, it remains a persistent presence in legislative proposals. It has been introduced in various forms, including as an amendment to the National Defense Authorization Act and as an amendment to the America COMPETES Act of 2022 (both of which failed), as well as a standalone bill.

Similar challenges exist in other bills that try to expand financial surveillance such as the Infrastructure Investment and Jobs Act, Transparency and Accountability in Service Providers Act, Crypto-Asset National Security Enhancement and Enforcement Act, and Digital Asset Anti-Money Laundering Act. Each new bill that passes could further chip away at our financial privacy.

Considering these laws and proposals are buried within thousands of pages of legislation, it's no wonder the public doesn't know what's going on.

A Constant Expansion Through Inflation

Even if every member of the public could read every bill front to back, there are still other ways that the Bank Secrecy Act regime has been able to expand silently each year. Surprisingly, inflation has also contributed to the erosion of our financial privacy.

Following the Bank Secrecy Act's requirement that financial institutions report transactions over $10,000, concerns were raised in court. A coalition including the American Civil Liberties Union, California Bankers Association, and Security National Bank argued that the Bank Secrecy Act violated constitutional protections, including the Fourth Amendment's protection against unreasonable search and seizure, as well as the First Amendment and Fifth Amendment. They successfully obtained a temporary restraining order against the act.

Unfortunately, the Supreme Court later held that the Bank Secrecy Act did not create an undue burden considering it applied to "abnormally large transactions" of $10,000 or more.

Let's put this number into context: In the 1970s, $10,000 was enough to buy two brand-new Corvettes and still have enough money left to cover taxes and upgrades. So perhaps the court's description of these transactions as "abnormally large" was fair at the time.

The problem is that this reporting threshold has never been adjusted for inflation. For over 50 years, it has stayed at $10,000. If the threshold had been adjusted this whole time, it would currently be around $75,000—not $10,000. Not adjusting for inflation would be like not receiving a cost-of-living adjustment for your income; it means losing money each year.

Each year with inflation is another year that the government is granted further access to people's financial activity. In 2022 alone, the U.S. financial services industry filed around 26 million reports under the Bank Secrecy Act. Of those, 20.6 million were on transactions of $10,000 or more, with around 4.3 million filed for suspicious activity. However, the second-most-common reason for filing a SAR was for transactions close to the $10,000 threshold. It almost makes one wonder why Congress bothered with a threshold at all if you can be reported for crossing it and also reported for not crossing it.

While the public has been focusing on the prices of groceries and gasoline when it comes to inflation, the impact of inflation on expanding financial surveillance has largely gone unnoticed.

Much of the Process Is Confidential

With millions of reports being filed each year as both Congress and inflation continue to expand the Bank Secrecy Act regime, shouldn't members of the public at least know if they were reported to the government? For a little while, Congress seemed to think the process should operate that way.

Realizing the need to establish boundaries after the Supreme Court gave the green light to deputizing financial institutions as law enforcement investigators, Congress enacted the Right to Financial Privacy Act of 1978. The legislation mandated that individuals should be told if the government is looking into their finances. Not only did the law establish a notification process, but it also allowed individuals to challenge these requests.

So why don't we see complaints of invasive financial surveillance on the news?

Put simply, the Right to Financial Privacy Act doesn't live up to its name. Although it should result in some protections, Congress included 20 exceptions that let the government get around them. For example, the fourth exception applies to disclosures pursuant to federal statutes, including the reports required under the Bank Secrecy Act.

Making matters worse, the Annunzio-Wylie Anti–Money Laundering Act made filing SARs a confidential process. Both financial institution employees and the government are prohibited from notifying customers if a transaction leads to a SAR.And it's not just the contents of the reports that are confidential: Banks cannot even reveal the existence of a SAR.

With these laws, banks went from protecting the privacy of their depositors to being forced to protect the secrecy of government surveillance programs. It's the epitome of "privacy for me, but not for thee."

The frustration and harm this process causes might not be so secret. There are numerous news stories about banks closing accounts without any explanation. While many have blamed the banks for giving customers the silent treatment, they may be legally prohibited from disclosing that a SAR led to the closure.

As one customer described it, "I feel that I was treated unjustly and at least I deserve to get an explanation. I had no overdrafts, always paid my credit cards on time and I consider myself to be an honest person, the way they closed my accounts made me feel like a criminal." Another customer said, "Any time I asked about why [my account was closed] they said they were not allowed to discuss the matter."

The government claims this process should be kept secret so that it doesn't tip off criminals. Yet SARs are not evidence of a crime by default.

The exact details of the reports are confidential but some aggregate statistics are available. These suggest that the top three reasons for a bank to file a SAR include (1) suspicions concerning the source of funds, (2) transactions below $10,000, and (3) transactions with no apparent economic purpose. These are not smoking guns.

There are many reasons why a bank might close an account, including inactivity, violations of terms and conditions, frequent overdrafts, and internal restructuring. But when banks refuse to explain closures, it might just be because they are prohibited from doing so, further keeping the public in the dark about financial surveillance activities.

A Balancing Act

Many might still ask, "If these reports catch a couple of bad guys, aren't they all worth it?" This raises a fundamental societal question: To what extent are we OK with pervasive surveillance if it stops bad people doing bad things?

To answer this question, we should first recognize that the optimal crime rate is not zero. While a world without crime might seem preferable, the costs of achieving that can be prohibitively high. We can't burn down the entire world just to stop somebody from stealing a pack of gum. There is a percentage of crime that is going to exist—it's not ideal, but it is optimal.

Similarly, the cost of pervasive surveillance is also too high. Maintaining a balance of power by protecting people's privacy is essential for a free society. Surveillance can restrict freedoms, such as the freedom to have certain religious beliefs, support certain causes, partake in dissent, and hold powerful people accountable. We need to have financial privacy. We have too many examples where surveillance has gone wrong and allowed these freedoms to be squashed. We have to be careful about creeping surveillance that tilts the balance of power too far away from the individual.

Removing this huge financial surveillance system doesn't mean ending the fight against terror or crime. It means making sure that Fourth Amendment protections are still present in the modern digital era. It's not supposed to be easy to get this magic permission slip that lets you into everyone's homes. The Constitution was put in place to prevent such abuses—to restrict the powers of government and protect the people.

Breaking the Illusion of Financial Privacy

Over the past 50 years, the U.S. government has slowly built a sprawling system of unchecked financial surveillance. It's time to question whether this is the world we want to live in. Instead of having a regime that generates 26 million reports on Americans at a cost of over $46 billion in a given year, we should have a system that respects individual rights and only goes after criminals.

Yet, government officials seem to have another vision in mind. Through obscure legislative changes, inflationary expansions, and a process of confidentiality, financial privacy has been continuously eroded over time.

Changing this reality is an uphill battle, but it's one that's worth fighting. The first step is raising awareness about how far financial surveillance norms have shifted in just a few decades.Changes won't happen until we dispel the illusion of financial privacy.

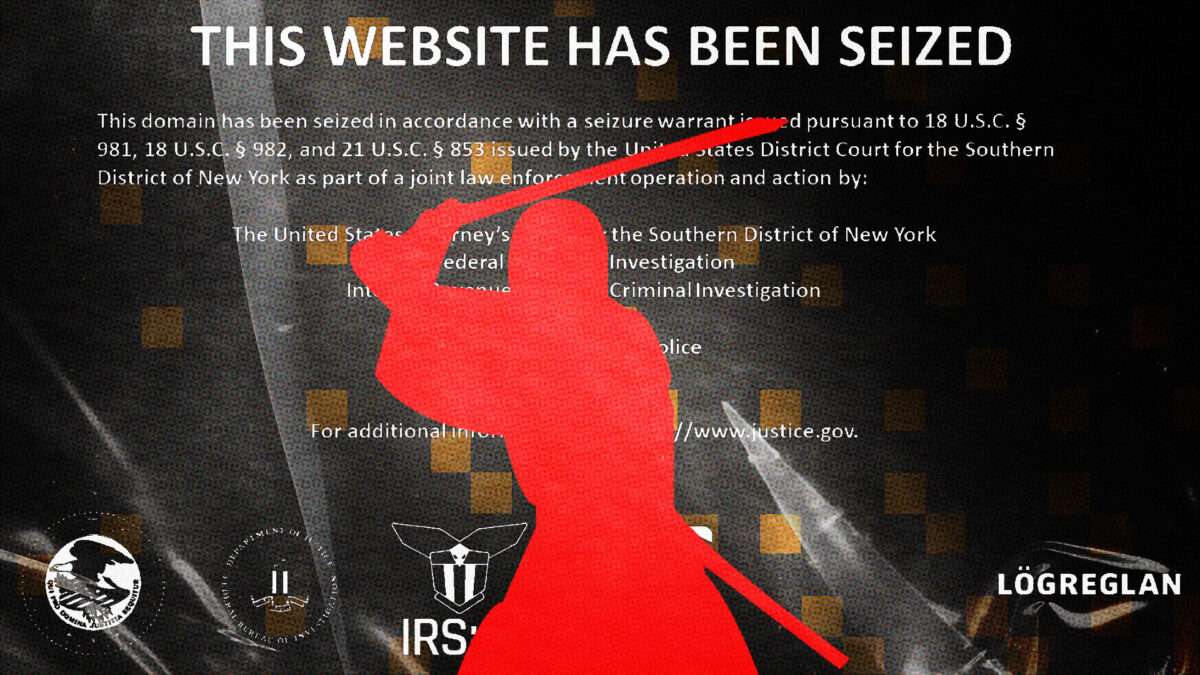

The Department of Justice indicted the creators of an application that helps people spend their bitcoins anonymously. They're accused of "conspiracy to commit money laundering." Why "conspiracy to commit" as opposed to just "money laundering"? Because they didn't hold anyone else's money or do anything illegal with it. They provided a privacy tool that may have enabled other people to do illegal things with their bitcoin. But that's not a crime,

The Department of Justice indicted the creators of an application that helps people spend their bitcoins anonymously. They're accused of "conspiracy to commit money laundering." Why "conspiracy to commit" as opposed to just "money laundering"?

Because they didn't hold anyone else's money or do anything illegal with it. They provided a privacy tool that may have enabled other people to do illegal things with their bitcoin. But that's not a crime, just as selling someone a kitchen knife isn't a crime. The case against the creators of Samourai Wallet is an assault on our civil liberties and First Amendment rights.

What this tool does is offer what's known as a "coinjoin," a method for anonymizing bitcoin transactions by mixing them with other transactions, as the project's founder, Keonne Rodriguez, explained to Reason in 2022:

"I think the best analogy for it is like smelting gold," he said. "You take your Bitcoin, you add it into [the conjoin protocol] Whirlpool, and Whirlpool smelts it into new pieces that are not associated to the original piece."

Smelting bars of gold would make it harder for the government to track. But if someone eventually uses a piece of that gold for an illegal purchase, should the creator of the smelting furnace go to prison? This is what the government is arguing.

Cash is the payment technology used most by criminals, but it also happens to be essential for preserving the financial privacy of law-abiding citizens, as Human Rights Foundation chief strategy officer Alex Gladstein told Reason:

"The ATM model, it gives people the option to have freedom money," says Gladstein. "Yes, the government will know all the ins and outs of what flows are coming in and out, but they won't know what you do with it when you leave. And that allows us to preserve the privacy of cash, which I think is essential for a democratic society."

The government's decision to indict Rodriguez and his partner William Lonergan Hill is also an attack on free speech because all they did was write open-source code and make it widely available.

"It is an issue of a chilling effect on free speech," attorney Jerry Brito, who heads up the cryptocurrency nonprofit Coin Center, told Reason after the U.S. Treasury went after the creators of another piece of anonymizing software. "So, basically, anybody who is in any way associated with this tool…a neutral tool that can be used for good or for ill, these people are now being basically deplatformed."

Are we willing to trade away our constitutional rights for the promise of security? For many in power, there seems to be no limit to what they want us to trade away.

In the '90s, the FBI tried to ban online encryption because criminals and terrorists might use it to have secret conversations. Had they succeeded, there would be no internet privacy. E-commerce, which relies on securely sending credit card information, might never have existed.

Remember when the Canadian government ordered banks to freeze money headed to the trucker protests? Central Bank Digital Currencies would make such efforts far easier.

"We come from first principles here in the global struggle for human rights," says Gladstein. "The most important thing is that it's confiscation resistant and censorship resistant and parallel, and can be done outside of the government's control."

The most important thing about bitcoin, and money like it, isn't its price. It's the check it places on the government's ability to devalue, censor, and surviel our money. Creators of open-source tools like Samourai Wallet should be celebrated, not threatened with a quarter-century in a federal prison.

Music Credits: "Intercept," by BXBRDVJA via Artlist; "You Need It,' by Moon via Artlist. Photo Credits: Graeme Sloan/Sipa USA/Newscom; Omar Ashtawy/APAImages / Polaris/Newscom; Paul Weaver/Sipa USA/Newscom; Envato Elements; Pexels; Emin Dzhafarov/Kommersant Photo / Polaris/Newscom; Anonymous / Universal Images Group/Newscom.

On April 24, the Department of Justice continued its assault on open source developers, arresting Keonne Rodriguez and William Lonergan Hill on allegations of money laundering. Rodriguez and Hill, operating the well-known bitcoin application Samourai Wallet, committed the grand offense of writing code. Under the auspices of money laundering, the DOJ seized servers located abroad, pulled the Samourai website from its domain, and had Google remove

On April 24, theDepartment of Justice continued its assault on open source developers, arresting Keonne Rodriguez and William Lonergan Hill on allegations of money laundering. Rodriguez and Hill, operating the well-known bitcoin application Samourai Wallet, committed the grand offense of writing code.

Under the auspices of money laundering, the DOJ seized servers located abroad, pulled the Samourai website from its domain, and had Google remove the app from its Play Store.

It's a stunning flashback to the 1990s "crypto wars," when the feds last went after cryptographers and others writing code.

At that time, government officials alleged that producing and sharing encryption technology amounted to exporting weapons. Politicians worried that these privacy technologies would fall into the "wrong" hands, so much so that President Bill Clinton declared anational emergency and then-Sen. Joe Biden (D–Del.) introduced a bill to allow the government tospy on text and voice communications.

Philip Zimmermann, a programmer, wrote an encryption software called Pretty Good Privacy (PGP) that would thwart the government's snooping efforts. As Paul Detrick explained for Reason, the software was so good that the DOJ launched a criminal investigation in 1993 "on the grounds that by publishing his software he had violated the Arms Export Control Act. To demonstrate that PGP was protected under the First Amendment, Zimmerman[n] got MIT Press to print out its source code in a book and sell it abroad."

The DOJ dropped the case.

Around the same time, Berkeley Ph.D. student Daniel Bernstein developed an encryption method called Snuffle based on a one-way hash function. After publishing an analysis and instructions on how to use his code, he reached out to theState Department to present it. Bad move. The State Department required Bernstein to "register as an arms dealer, and apply for a[n] export license merely to publish his work online." Berstein, represented by the Electronic Frontier Foundation, took the government to court, and ever since the landmark ruling in Bernstein v. U.S. Department of Justice, code has been considered speech.

Thirty years later, politicians are now worried less about technical data leaking to foreigners and more about those foreigners' money flows. In a supposed attempt to prevent terrorism, the government is cracking down on money laundering.

But the main impetus hasn't changed: Behavior not subject to the oversight of the U.S. government must be suspicious—and is probably illegal.

With roots in thecypherpunk ethos to which both Zimmermann and Bernstein belonged, bitcoin encompasses the "code is speech" verdict from the '90s. Bitcoin is a digital currency based on an elaborate system of cryptographically protected numbers, signed and validated by other numbers, all in the open. Bitcoin is math. Software that runs bitcoin wallets are strings of 1s and 0s; they are speech, and at no point dobitcoin transactions cease to be speech.

The main service for which Rodriguez and Hill's Samourai Wallet has run afoul with law enforcement is Whirlpool, a privacy-enhancing feature on a blockchain that's otherwise open and available for anyone to inspect. In the fiat system, my employer can't spy into my bank account or I into theirs (though the bank can, and anyone who successfully hacks the bank's record). A grocery store, car dealership, or insurance provider can't see how much funds I have, where they came from, or who might have spent them a few hops before they came to me. With bitcoin, that's all in the open—hence why services like Whirlpool are so important.

Whirlpool constructs a five-input, five-output transaction between an unknown number of people. Five units of similar-sized bitcoin go in and five come out to new addresses. This obfuscates the individual coins' history, and anybody observing flows on thepublicly available blockchain can no longer know which of the five outputs belonged to which input.

In the DOJ's enlightened view, that now constitutes money laundering and a failure to register as a money transmitter, even though Samourai is a noncustodial wallet, where the "operators do not take custody of user funds and therefore are technically incapable to 'accept' deposits or 'execute' the transmission of funds," according to Bitcoin Magazine.

I sometimes get paid in bitcoin from various international clients and employers. I've used Whirlpool many times—and it's about as nefarious and shady as any good old cash transaction. I don't exactly want my employer to be able to find out where I spent my funds. I definitely don't want someone I send bitcoin to to know how much I carry in the specific wallet from which I was spending. This is all standard hygiene in a modern digital world; we leak wealth and spending information like crazy, and protecting some of that privacy is just prudent behavior.

Have there been terrorists or otherwise certified Bad People using Samourai's services? Probably, but that's too low of a bar to throw a legal fuss. It's a bad-faith argument, as Reason's Zach Weismuller writes: "They will point to bad people using these tools, just as they pointed out that Hamas raised some funds in various cryptocurrencies, without noting that a vast amount of money laundering happens with government-issued currency."

Terrorists and criminals use these services, officials say. OK, but they also, to a much larger extent,use the U.S. dollar. Maybe the DOJ should arrest Jerome Powell and confiscate the Federal Reserve's servers while they're at it. We don't go after high-end leather wallet manufacturers because some of their customers carry notes that may have once been involved in crimes. We don't inspect cash registers at gas stations for illicit dollars—and then go after the manufacturer of the cash register themselves.

That's what Rodriguez and Hill are: manufacturers. Using code, they created a program that others operate on their own phones and computers. At no point in the process did they take custody of users' funds—which is why all the DOJ acquired when arresting Rodriguez and Hill were servers and domains. No stash of laundered and illicit bitcoin sat in the basement of the alleged culprits.

Government protagonists always have seemingly good reasons—terrorism, trafficking, drugs, Bad People doing normal things—to intervene and sidestep people's rights.

Those of us who worry about government overreach always feared that the crypto wars of the 1990s mightone day return. Last week, the DOJ revived that battle.

A large metaverse project created by the company behind the Bored Apes Yacht Club NFT project held a recent series of beta sessions for individuals who owned certain NFTs. While the developers claim this is just the beginning, it’s not looking promising considering how much money is involved. Read more...

A large metaverse project created by the company behind the Bored Apes Yacht Club NFT project held a recent series of beta sessions for individuals who owned certain NFTs. While the developers claim this is just the beginning, it’s not looking promising considering how much money is involved.