iPhone and Apple Watch users in California will soon be able to add their digital ID and driver's license to the Wallet app, as revealed by new landing pages on the state DMV website. This feature follows a slow rollout since its announcement, with only five states currently supporting it. MacRumors reports: "Now you can add your California driver's license or state ID to Apple Wallet on iPhone and Apple Watch so you can present it easily and securely in person and in app," reads the landing pag

iPhone and Apple Watch users in California will soon be able to add their digital ID and driver's license to the Wallet app, as revealed by new landing pages on the state DMV website. This feature follows a slow rollout since its announcement, with only five states currently supporting it. MacRumors reports: "Now you can add your California driver's license or state ID to Apple Wallet on iPhone and Apple Watch so you can present it easily and securely in person and in app," reads the landing page, which contains broken links and placeholder images, and is still missing a proper website security certificate. The webpages were discovered on Sunday by Jimmy Obomsawin, after someone added a link to the landing pages in an Apple Wallet Wikipedia entry last Wednesday.

In Spartanburg County, South Carolina, on Interstate 85, police officers stop vehicles for traveling in the left lane while not actively passing, touching the white fog line, or following too closely. This annual crackdown is called Operation Rolling Thunder, and the police demand perfection. Any infraction, no matter how minor, can lead to a roadside interrogation and warrantless search. However, a 21-month fight for transparency shows participa

In Spartanburg County, South Carolina, on Interstate 85, police officers stop vehicles for traveling in the left lane while not actively passing, touching the white fog line, or following too closely. This annual crackdown is called Operation Rolling Thunder, and the police demand perfection.

Any infraction, no matter how minor, can lead to a roadside interrogation and warrantless search. However, a 21-month fight for transparency shows participating agencies play loose with South Carolina's Freedom of Information Act (FOIA), which requires the government to perform its business in an "open and public manner."

Motorists must follow state laws with exactness. But the people in charge of enforcement give themselves a pass.

Deny, Deny, Deny

The drawn-out FOIA dispute started on October 11, 2022, less than one week after a five-day blitz that produced nearly $1 million in cash seizures. Our public-interest law firm, the Institute for Justice, requested access to incident reports for all 144 vehicle searches that occurred during the joint operation involving 11 agencies: The Cherokee, Florence, Greenville, and Spartanburg County sheriff's offices; the Duncan, Gaffney, and Wellford police departments; the South Carolina Highway Patrol, Law Enforcement Division, and State Transport Police; and the U.S. Department of Homeland Security.

Our intent was simple. We wanted to check for constitutional violations, which can multiply in the rush to pull over and search as many vehicles as possible within a set time frame. South Carolina agencies have conducted the operation every year since 2006, yet no one has ever done a systematic audit.

Rather than comply with its FOIA obligation, Spartanburg County denied our request without citing any provision in the law. We tried again and then recruited the help of South Carolina resident and attorney Adrianne Turner, who filed a third request in 2023.

It took a lawsuit to finally pry the records loose. Turner filed the special action with outside representation.

Key Findings

The incident reports, released in batches from March through July 2024, show why Spartanburg County was eager to prevent anyone from obtaining them.

Over 72 percent of vehicle searches during Operation Rolling Thunder in 2022 produced nothing illegal. Officers routinely treated innocent drivers like criminals.

Carrying any amount of cash is legal, but officers treated currency as contraband. The records describe no single case in which officers found a large amount of cash and did not seize it. All money was presumed dirty.

Officers pressured property owners to sign roadside abandonment forms, giving up claims to their cash on the spot.

South Carolina residents mostly got a pass. Officers focused on vehicles with out-of-state plates, rental cars, and commercial buses. Over 83 percent of the criminal suspects identified during warrantless searches lived out of state. Nearly half were from Georgia.

Black travelers were especially vulnerable. Nearly 74 percent of the suspects identified and 75 percent of the people arrested were black. This is more than triple the South Carolina black population of 25 percent.

Working in the Shadows

While these records shine a light on police conduct, still more secrets remain.

By policy, the Spartanburg County Sheriff's Office and partner agencies do not create incident reports for every search. They only document their "wins" when they find cash or contraband. They do not document their "losses" when they come up empty.

Thanks to this policy, Spartanburg County has no records for 102 of the 144 searches that occurred during Operation Rolling Thunder in 2022. Nowhere do officers describe how they gained probable cause to enter the vehicles where nothing was found. The police open and close investigations and then act like the searches never happened.

This leaves government watchdogs in the dark—by design. They cannot inspect public records that do not exist. Victims cannot cite them in litigation. And police supervisors cannot review them when evaluating job performance.

Even if body camera video exists, there is no paper trail. This lack of recordkeeping undercuts the intent of FOIA. Agencies dodge accountability by simply not summarizing their embarrassing or potentially unconstitutional conduct.

The rigged system is rife with abuse. Available records show that officers routinely order drivers to exit their vehicles and sit in the front seat of a patrol car. If people show signs of "labored breathing," "nervousness," or being "visibly shaken," the police count this toward probable cause.

Officers overlook that anxiety is normal when trapped in a police cruiser without permission to leave. Even people who value their Fourth Amendment right to be "secure in their persons, houses, papers, and effects, against unreasonable searches and seizures" can break under pressure and consent to a search.

If travelers refuse, officers can bring K9 units to the scene for open-air sniffs. Having no drugs in the vehicle does not always help. False positives occurred during Operation Rolling Thunder, but the lack of recordkeeping makes a complete audit impossible.

Intimidation, harassment, and misjudgment are easily hidden. The police tell travelers: "If you have nothing to hide, you should let us search." But when the roles are reversed and the public asks questions, agencies suddenly want to remain silent.

Limited Run Games has announced that 20 new-old games will be released in physical form, including Fear Effect, Lollipop Chainsaw RePOP, Starship Troopers: Extermination, and Wolfenstein 2: The New Colossus.As part of its LRG3 2024 showcase, the distributor confirmed not only the 20th anniversary edition of Beyond Good & Evil, but also physical releases of classic PS1 games Gex Trilogy, Tomba Special Edition and Tomba 2, Fear Effect, and more – much, much more.In true LRG style, the Limited

Limited Run Games has announced that 20 new-old games will be released in physical form, including Fear Effect, Lollipop Chainsaw RePOP, Starship Troopers: Extermination, and Wolfenstein 2: The New Colossus.

As part of its LRG3 2024 showcase, the distributor confirmed not only the 20th anniversary edition of Beyond Good & Evil, but also physical releases of classic PS1 games Gex Trilogy, Tomba Special Edition and Tomba 2, Fear Effect, and more – much, much more.

In true LRG style, the Limited Run Games editions of the following games will be released in physical form only, including:

In 2024, the federal budget deficit is estimated to reach nearly $2 trillion, according to new projections released by the Congressional Budget Office (CBO) this week. In February, the agency predicted that the deficit would only be $1.58 trillion. However, spending increases have caused the projected deficit to increase by $400 billion, a staggering 27 percent hike. According to the CBO, 80 percent of the spike in the deficit can be blamed on f

In 2024, the federal budget deficit is estimated to reach nearly $2 trillion, according to new projections released by the Congressional Budget Office (CBO) this week. In February, the agency predicted that the deficit would only be $1.58 trillion. However, spending increases have caused the projected deficit to increase by $400 billion, a staggering 27 percent hike.

According to the CBO, 80 percent of the spike in the deficit can be blamed on four sources of government spending.

The largest source, responsible for $145 billion of the increase, is changes to the federal student loan program that have resulted in massive waves of federal student loan forgiveness and increased forgiveness going forward.

Second, the CBO's report details how the costs for "deposit insurance have increased by about $70 billion because the Federal Deposit Insurance Corporation (FDIC) is not recovering payments it made when resolving bank failures in 2023 and 2024 as quickly as CBO previously anticipated."

Third, an additional $60 billion in cost increases came from additional legislation. And lastly, $50 billion in increased spending came from higher-than-expected Medicaid costs.

The long-term outlook for the budget deficit has increased too. In February, the CBO estimated that in 2034, the deficit would climb to $2.5 trillion. Its latest estimate now places that number as over $2.8 trillion.

"For the 2025–2034 period, CBO now projects that if current laws generally remained unchanged, the cumulative deficit would be $22.1 trillion. That amount is $2.1 trillion (or 10 percent) more than the $20.0 trillion the agency projected this past February," reads the CBO's report. "Measured in relation to the size of the economy, federal debt at the end of 2034 is now projected to equal 122 percent of gross domestic product (GDP); in February, debt at the end of that year was projected to equal 116 percent of GDP."

If the deficit continues to increase as the CBO predicts, the outcome could be disastrous.

"As debt grows unabated, there is the risk of a sudden loss of confidence in bond markets, with investors demanding much higher interest rates that could trigger a debt doom loop and broader fiscal crisis," Cato Institute researchers Romina Boccia and Dominik Lett warned this week. "Congress and the Biden administration should cut spending now while the economy is growing and conditions are favorable for deficit reduction, alleviating pressure on interest rates and the federal debt to grow, and before a fiscal crisis forces their hands."

From small donors to rich Silicon Valley investors, Donald Trump enthusiasts signaled their support for the convicted felon by sending money to his campaign.

From small donors to rich Silicon Valley investors, Donald Trump enthusiasts signaled their support for the convicted felon by sending money to his campaign.

The Affordable Connectivity Program (ACP), which provided monthly internet bill credits for low-income Americans, will officially end on June 1 due to a lack of additional funding from Congress. This termination threatens nearly 60 million Americans with increased financial hardship, as the program's lapse leaves them without the subsidies that made internet access affordable. CNN reports: The 2.5-year-old ACP provided eligible low-income Americans with a monthly credit off their internet bills,

The Affordable Connectivity Program (ACP), which provided monthly internet bill credits for low-income Americans, will officially end on June 1 due to a lack of additional funding from Congress. This termination threatens nearly 60 million Americans with increased financial hardship, as the program's lapse leaves them without the subsidies that made internet access affordable. CNN reports: The 2.5-year-old ACP provided eligible low-income Americans with a monthly credit off their internet bills, worth up to $30 per month and as much as $75 per month for households on tribal lands. The pandemic-era program was a hit with members of both political parties and served tens of millions of seniors, veterans and rural and urban Americans alike. Program participants received only partial benefits in May ahead of the ACP's expected collapse. [...]

On Friday, Biden reiterated his calls for Congress to pass legislation extending the ACP. He also announced a series of voluntary commitments by a handful of internet providers to offer -- or continue offering -- their own proprietary low-income internet plans.

The list includes AT&T, Comcast, Cox, Charter's Spectrum and Verizon, among others. Those providers will continue to offer qualifying ACP households a broadband plan for $30 or less, the White House said, and together the companies are expected to cover roughly 10 million of the 23 million households relying on the ACP. "The Affordable Connectivity Program filled an important gap that provider low-income programs, state and local affordability programs, and the Lifeline program cannot fully address," said FCC Chairwoman Jessica Rosenworcel in a statement, referring to the name of another, similar FCC program that subsidizes wireless and home internet service. "The Commission is available to provide any assistance Congress may need to support funding the ACP in the future and stands ready to resume the program if additional funding is provided."

Congressional Budget Office (CBO) projections provide valuable insights into how a big chunk of your income is being spent and reveal the long-term consequences of our government's current fiscal policies—you may endure them, and your children most certainly will. Yet, like most other projections looking into our future, these numbers should be taken with a grain of salt. So should claims that CBO projections validate anyone's fiscal track record

Congressional Budget Office (CBO) projections provide valuable insights into how a big chunk of your income is being spent and reveal the long-term consequences of our government's current fiscal policies—you may endure them, and your children most certainly will. Yet, like most other projections looking into our future, these numbers should be taken with a grain of salt. So should claims that CBO projections validate anyone's fiscal track record.

So much can and likely will happen to make projections moot and our fiscal outlook much grimmer. Unforeseen events, economic changes, and policy decisions render them less accurate over time. The CBO knows this and recently released alternative scenarios based on different sets of assumptions, and it doesn't look good. It remains a wonder that more politicians, now given a more realistic range of possibilities, aren't behaving like it.

First, let's recap what the situation looks like under the usual rosy growth, inflation, and interest rate assumptions. Due to continued overspending, this year's deficit will be at least $1.6 trillion, rising to $2.6 trillion by 2034. Debt held by the public equals roughly 99 percent of our economy—measured by gross domestic product (GDP)—annually, heading to 116 percent in 2034.

The only reason these numbers won't be as high as projected last year is that a few House Republicans fought hard to impose some spending caps during the debt ceiling debate. The long-term outlook is even scarier, with public debt reaching 166 percent of GDP in 30 years and all federal debt reaching 180 percent.

No one should be surprised. To be sure, the COVID-19 pandemic and the Great Recession made things worse, but we've been on this path for decades.

Unfortunately, if any of the assumptions underlying these projections change again, things will get a lot worse. That's where the CBO's alternative paths help. Policymakers and the public can better see the potential risks and opportunities associated with various fiscal policy choices, enabling them to make more informed decisions.

For instance, the CBO highlights that if the labor force grows annually by just 0.1 fewer percentage points than originally projected—even if the unemployment rate stays the same—slower economic growth will lead to a deficit $142 billion larger than baseline projections between 2025 and 2034. A similarly small slowdown in the productivity rate would lead to an added deficit of $304 billion over that period.

Back in 2020, the prevalent theory among those who claimed we shouldn't worry about debt was that interest rates were remarkably low and would stay low forever. As if. These guys have since learned what many of us have known for years: that interest rates can and will go up when the situation gets bad enough. So, what happens if rates continue to rise above and beyond those CBO used in its projections? Even a minuscule 0.1-point rise above the baseline would produce an additional $324 billion on the deficit over the 2025-2034 period.

The same is true with inflation, which, as every shopper can see, has yet to be defeated. If inflation, as I fear, doesn't go away as fast as predicted by CBO—largely because debt accumulation is continuing unabated—it will slow growth, increase interest rates, and massively expand the deficit. To be precise, an increase in overall prices of just 0.1 points over the CBO baseline would result in higher interest rates and a deficit of $263 billion more than projected.

Now, imagine all these variations from the current projections happening simultaneously. It's a real possibility. The deficit hike would be enormous, which could then trigger even more inflation and higher interest rates. The question that remains is: Why aren't politicians on both sides more worried than they seem to be?

What needs to happen before they finally decide to treat our fiscal situation as a real threat? President Joe Biden doesn't want to tackle the debt issue. In fact, he's actively adding to the debt with student loan forgiveness, subsidies to big businesses, and other nonsense. Meanwhile, some Republicans pay lip service to our financial crisis, but few are willing to tackle the real problem of entitlement spending.

The time for political posturing is over. The longer we wait to address these issues, the more severe the consequences will be for future generations. It's time for our leaders to prioritize the nation's long-term economic health over short-term political gains and take bold steps toward fiscal responsibility. Only then can we hope to secure a stable and prosperous future for all Americans.

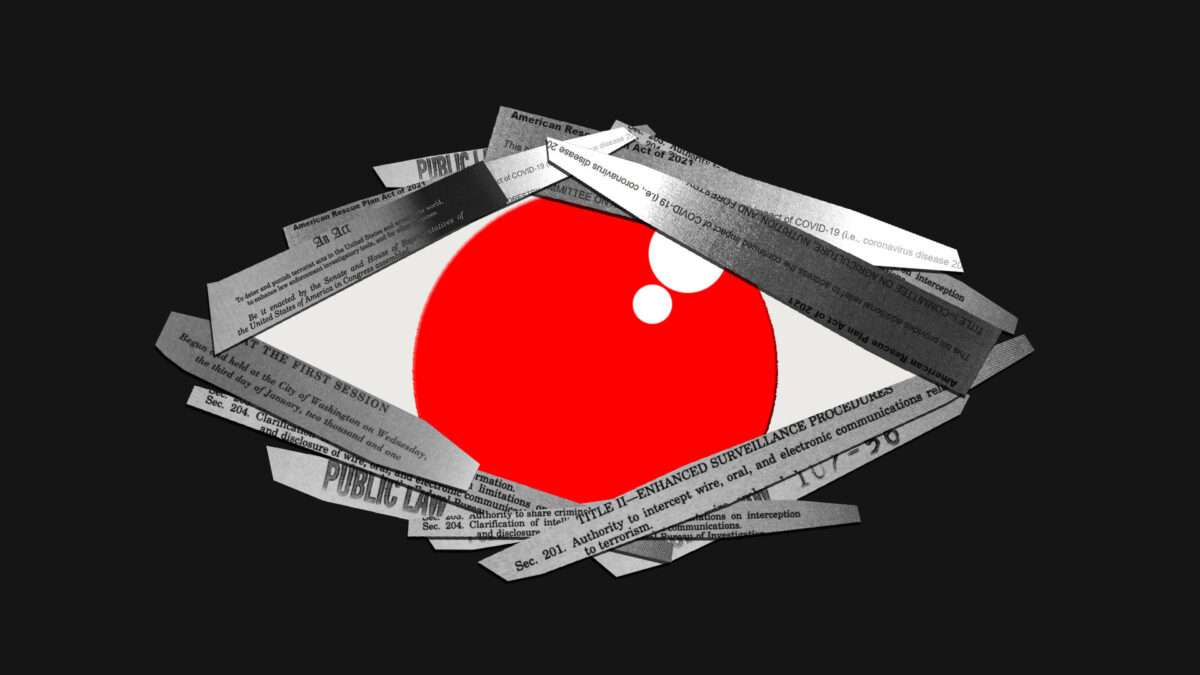

You have a 15-character password, shield the ATM as you enter your PIN, close the door when you meet with your banker, and shred your financial statements. But do you truly have financial privacy? Or has someone else been sitting silently in the room with you this whole time? While you might feel you have secured your financial information, the government has very much wedged its way into the room. Financial privacy has practically vanished over

You have a 15-character password, shield the ATM as you enter your PIN, close the door when you meet with your banker, and shred your financial statements. But do you truly have financial privacy? Or has someone else been sitting silently in the room with you this whole time?

While you might feel you have secured your financial information, the government has very much wedged its way into the room. Financial privacy has practically vanished over the last 50 years.

It's strange how quickly we have accepted the current state of financial surveillance as the norm. Just a few decades ago, withdrawing money didn't involve 20 questions about what we plan to use the money for, what we do for a living, and where we are from. Our daily transactions weren't handed over in bulk to countless third parties.

Yet, what is even stranger is that most people continue to believe in a version of financial privacy that no longer exists. They believe financial records continue to be private and the government needs a warrant to go after them. This belief couldn't be further from reality. Americans do not have financial privacy. Rather, we have the illusion of financial privacy.

Why is this? Put simply, financial surveillance has been kept hidden in three major ways: Encroachments into privacy have evolved gradually through obscure legislation, the scope of surveillance has constantly expanded through inflation, and much of the process is kept intentionally confidential.

Years of Obscure Legislative Changes

Compared to today, customers in the 1970s had far more freedom in opening accounts and interacting with their own money. Back then, the decision to transact with a bank could be based on the cash in one's pocket. Transactions were not scrutinized for threats of terrorism or drug trafficking. Customers were not legally required to supply a photo ID to set up an account. Banks decided for themselves what information they needed to set up an account, and this information remained effectively confidential between the customer and the bank.

This changed in the 1970s when a pivotal piece of legislation was passed: the Bank Secrecy Act. Stemming from concerns in Congress regarding Americans concealing their wealth in offshore accounts, the legislation aimed to gather financial information to detect such activities. For example, financial institutions were required to monitor and report transactions over $10,000 to the government.

It didn't stop there. Over the years, Congress came up with more ways to expand financial surveillance in what is now best referred to as the "Bank Secrecy Act regime."

In 1992, the Annunzio-Wylie Anti–Money Laundering Act led to the introduction of suspicious activity reports (SARs), where, instead of just reporting anything over $10,000, financial institutions had to report "any suspicious transaction relevant to a possible violation of law or regulation." Two years later, the Money Laundering Suppression Act authorized the secretary of the treasury to designate the Financial Crimes Enforcement Network (FinCEN) as the agency to oversee these reports.

Following the September 11 attacks, the USA PATRIOT Act significantly expanded surveillance powers, granting the government easier access to communication records. Hidden among the pages of this sprawling omnibus bill was a set of "know your customer" requirements that forced banks not only to investigate who you are but also to verify that information on behalf of the government.

Again, Congress didn't stop there.

Another extensive omnibus bill, the American Rescue Plan Act of 2021, quietly introduced a rule intended to surveil all bank accounts with at least $600 of activity. Luckily, the controversial measure was noticed and met with immediate pushback. The Treasury Department responded by informing people that the government already has access to much of everyone's financial information.

While the proposal was retracted, the initiative was only shut down partially. Instead of affecting all bank accounts, the law narrowed its scope to require reporting for transactions over $600 made through a payment transmitter such as PayPal, Venmo, or Cash App.

Then the 2022 Special Measures To Fight Modern Threats Act aimed to eliminate some of the checks and balances placed on the Treasury, granting it the authority to use "special measures" to sanction international transactions.

While the Special Measures To Fight Modern Threats Act hasn't been passed, it remains a persistent presence in legislative proposals. It has been introduced in various forms, including as an amendment to the National Defense Authorization Act and as an amendment to the America COMPETES Act of 2022 (both of which failed), as well as a standalone bill.

Similar challenges exist in other bills that try to expand financial surveillance such as the Infrastructure Investment and Jobs Act, Transparency and Accountability in Service Providers Act, Crypto-Asset National Security Enhancement and Enforcement Act, and Digital Asset Anti-Money Laundering Act. Each new bill that passes could further chip away at our financial privacy.

Considering these laws and proposals are buried within thousands of pages of legislation, it's no wonder the public doesn't know what's going on.

A Constant Expansion Through Inflation

Even if every member of the public could read every bill front to back, there are still other ways that the Bank Secrecy Act regime has been able to expand silently each year. Surprisingly, inflation has also contributed to the erosion of our financial privacy.

Following the Bank Secrecy Act's requirement that financial institutions report transactions over $10,000, concerns were raised in court. A coalition including the American Civil Liberties Union, California Bankers Association, and Security National Bank argued that the Bank Secrecy Act violated constitutional protections, including the Fourth Amendment's protection against unreasonable search and seizure, as well as the First Amendment and Fifth Amendment. They successfully obtained a temporary restraining order against the act.

Unfortunately, the Supreme Court later held that the Bank Secrecy Act did not create an undue burden considering it applied to "abnormally large transactions" of $10,000 or more.

Let's put this number into context: In the 1970s, $10,000 was enough to buy two brand-new Corvettes and still have enough money left to cover taxes and upgrades. So perhaps the court's description of these transactions as "abnormally large" was fair at the time.

The problem is that this reporting threshold has never been adjusted for inflation. For over 50 years, it has stayed at $10,000. If the threshold had been adjusted this whole time, it would currently be around $75,000—not $10,000. Not adjusting for inflation would be like not receiving a cost-of-living adjustment for your income; it means losing money each year.

Each year with inflation is another year that the government is granted further access to people's financial activity. In 2022 alone, the U.S. financial services industry filed around 26 million reports under the Bank Secrecy Act. Of those, 20.6 million were on transactions of $10,000 or more, with around 4.3 million filed for suspicious activity. However, the second-most-common reason for filing a SAR was for transactions close to the $10,000 threshold. It almost makes one wonder why Congress bothered with a threshold at all if you can be reported for crossing it and also reported for not crossing it.

While the public has been focusing on the prices of groceries and gasoline when it comes to inflation, the impact of inflation on expanding financial surveillance has largely gone unnoticed.

Much of the Process Is Confidential

With millions of reports being filed each year as both Congress and inflation continue to expand the Bank Secrecy Act regime, shouldn't members of the public at least know if they were reported to the government? For a little while, Congress seemed to think the process should operate that way.

Realizing the need to establish boundaries after the Supreme Court gave the green light to deputizing financial institutions as law enforcement investigators, Congress enacted the Right to Financial Privacy Act of 1978. The legislation mandated that individuals should be told if the government is looking into their finances. Not only did the law establish a notification process, but it also allowed individuals to challenge these requests.

So why don't we see complaints of invasive financial surveillance on the news?

Put simply, the Right to Financial Privacy Act doesn't live up to its name. Although it should result in some protections, Congress included 20 exceptions that let the government get around them. For example, the fourth exception applies to disclosures pursuant to federal statutes, including the reports required under the Bank Secrecy Act.

Making matters worse, the Annunzio-Wylie Anti–Money Laundering Act made filing SARs a confidential process. Both financial institution employees and the government are prohibited from notifying customers if a transaction leads to a SAR.And it's not just the contents of the reports that are confidential: Banks cannot even reveal the existence of a SAR.

With these laws, banks went from protecting the privacy of their depositors to being forced to protect the secrecy of government surveillance programs. It's the epitome of "privacy for me, but not for thee."

The frustration and harm this process causes might not be so secret. There are numerous news stories about banks closing accounts without any explanation. While many have blamed the banks for giving customers the silent treatment, they may be legally prohibited from disclosing that a SAR led to the closure.

As one customer described it, "I feel that I was treated unjustly and at least I deserve to get an explanation. I had no overdrafts, always paid my credit cards on time and I consider myself to be an honest person, the way they closed my accounts made me feel like a criminal." Another customer said, "Any time I asked about why [my account was closed] they said they were not allowed to discuss the matter."

The government claims this process should be kept secret so that it doesn't tip off criminals. Yet SARs are not evidence of a crime by default.

The exact details of the reports are confidential but some aggregate statistics are available. These suggest that the top three reasons for a bank to file a SAR include (1) suspicions concerning the source of funds, (2) transactions below $10,000, and (3) transactions with no apparent economic purpose. These are not smoking guns.

There are many reasons why a bank might close an account, including inactivity, violations of terms and conditions, frequent overdrafts, and internal restructuring. But when banks refuse to explain closures, it might just be because they are prohibited from doing so, further keeping the public in the dark about financial surveillance activities.

A Balancing Act

Many might still ask, "If these reports catch a couple of bad guys, aren't they all worth it?" This raises a fundamental societal question: To what extent are we OK with pervasive surveillance if it stops bad people doing bad things?

To answer this question, we should first recognize that the optimal crime rate is not zero. While a world without crime might seem preferable, the costs of achieving that can be prohibitively high. We can't burn down the entire world just to stop somebody from stealing a pack of gum. There is a percentage of crime that is going to exist—it's not ideal, but it is optimal.

Similarly, the cost of pervasive surveillance is also too high. Maintaining a balance of power by protecting people's privacy is essential for a free society. Surveillance can restrict freedoms, such as the freedom to have certain religious beliefs, support certain causes, partake in dissent, and hold powerful people accountable. We need to have financial privacy. We have too many examples where surveillance has gone wrong and allowed these freedoms to be squashed. We have to be careful about creeping surveillance that tilts the balance of power too far away from the individual.

Removing this huge financial surveillance system doesn't mean ending the fight against terror or crime. It means making sure that Fourth Amendment protections are still present in the modern digital era. It's not supposed to be easy to get this magic permission slip that lets you into everyone's homes. The Constitution was put in place to prevent such abuses—to restrict the powers of government and protect the people.

Breaking the Illusion of Financial Privacy

Over the past 50 years, the U.S. government has slowly built a sprawling system of unchecked financial surveillance. It's time to question whether this is the world we want to live in. Instead of having a regime that generates 26 million reports on Americans at a cost of over $46 billion in a given year, we should have a system that respects individual rights and only goes after criminals.

Yet, government officials seem to have another vision in mind. Through obscure legislative changes, inflationary expansions, and a process of confidentiality, financial privacy has been continuously eroded over time.

Changing this reality is an uphill battle, but it's one that's worth fighting. The first step is raising awareness about how far financial surveillance norms have shifted in just a few decades.Changes won't happen until we dispel the illusion of financial privacy.

A federal court yesterday heard arguments in an appeal concerning an area of law that, while niche, has seen a streak of similarly situated plaintiffs pile up in recent years. At stake: When a SWAT team destroys an innocent person's property, should the owner be strapped with the bill? There is what I would consider a commonsense answer to that question. But in a reminder that common sense does not always guide law and policy, that is not the ans

A federal court yesterday heard arguments in an appeal concerning an area of law that, while niche, has seen a streak of similarly situated plaintiffs pile up in recent years. At stake: When a SWAT team destroys an innocent person's property, should the owner be strapped with the bill?

There is what I would consider a commonsense answer to that question. But in a reminder that common sense does not always guide law and policy, that is not the answer reached by several courts across the U.S., where such victims are sometimes told that "police powers" provide an exception to the Constitution's promise to give just compensation when the government usurps property for public use.

It remains to be seen where the U.S. Court of Appeals for the 6th Circuit will fall as it evaluates the complaint from Mollie and Michael Slaybaugh, who are reportedly on the hook for over $70,000 after a SWAT team destroyed much of their home in Smyrna, Tennessee.

In January 2022, Mollie Slaybaugh stepped outside her house and was greeted by a police officer with his gun drawn. She was informed that her adult son, James Jackson Conn—who did not live with her but had recently arrived to visit—was wanted for questioning concerning the murder of a police officer, which she says was news to her. Although she offered to speak to Conn and bring him out of her house, law enforcement declined to permit that, or to let her re-enter at all, so she went to stay at her daughter's house nearby.

The next day, police broke down the door and launched dozens of tear gas grenades into the Slaybaughs' home, laying waste to nearly everything in the house. Their insurance declined to assist them, as their policy—like many policies—does not cover damage caused by the government. Yet both Smyrna and Rutherford County said they were immune from helping as well.

But despite Mollie Slaybaugh's offer to coax Conn out sans tear gas, her complaint does not dispute that it was in the best interest of the community for law enforcement to do as they did that day. It merely contests the government's claim that innocent property owners should have to bear the financial burden by themselves when police destroy their homes in pursuit of a suspect.

"Law enforcement is a public good. Through our taxes, we pay for the training, equipment, and salaries of police officers. We pay to incarcerate criminals. We pay for a court system and public defenders," reads her complaint. "When the police destroy private property in the course of enforcing the criminal laws, that is simply another cost of law enforcement. Forcing random, innocent individuals to shoulder that cost alone would be as fair as conducting a lottery to determine who has to pay the police chief's salary each year."

That hypothetical is absurd. And yet the spirit of it is at the heart of several court decisions on the matter. That includes the U.S. District Court for the Middle District of Tennessee, which ruled last year that the Slaybaughs were not entitled to a payout because, in the court's view, the Takings Clause of the Fifth Amendment does not apply when the state seizes and destroys someone's property in the exercise of "police powers."

The Slaybaughs are unfortunately not alone. The notion that "police powers" immunize the government from liability is what doomed Leo Lech's lawsuit, which he filed after a SWAT team did so much damage to his home—in pursuit of a suspect that broke in and had no relation to the family—that it had to be demolished. In 2020, the Supreme Court declined to hear the case.

Similar claims are continuing to accumulate. The city of Los Angeles refused to compensate Carlos Pena after a SWAT team destroyed his North Hollywood print shop in pursuit of a suspect who barricaded himself inside, and the government in McKinney, Texas, turned away Vicki Baker after police ruined her home and much of its contents while, again, trying to catch a fugitive. After a legal odyssey of sorts, Baker was able to secure a judgment from a federal jury—though that was ultimately overturned by the U.S. Court of Appeals for the 5th Circuit, which ruled there was a "necessity" exception to the Takings Clause. Most recently, the local government in South Bend, Indiana, rejected Amy Hadley's pleas for help after police mutilated her home in search of a suspect she'd never met and who'd never been to her home. An officer's botched investigation led law enforcement to her house, and she has been forced to pay the price of that blunder. Accountability should not just be for the little people.

"The plain text of the Just Compensation Clause contains no exemptions for the police power, for public necessity, or for damage done by law enforcement. And the government bears the burden of establishing that any such exception is grounded in our nation's history and tradition," Jeffrey Redfern, an attorney with the Institute for Justice representing the Slaybaughs, told the 6th Circuit yesterday. "But the government hasn't even tried to meet that burden. Instead it asks this court to blindly follow decisions from other jurisdictions—decisions whose reasoning the government isn't really defending."

In some sense, the government is throwing what it can at the wall to see what sticks. And a fair amount of nonadhesive material is successfully latching on—an exception to the laws of nature that few entities other than the government could reasonably hope to enjoy.

Dennis Powanda and Vincent Yakaitis are bound together by a common experience: They were both criminally charged in connection with an attempted burglary. Powanda was the burglar, and Yakaitis was the property owner. Ah, justice. Indeed, that's not a misprint, parody, or a bad joke (although I wish it were the latter). Powanda was arrested and charged with criminal trespass and burglary, along with other related offenses, for executing the botche

Dennis Powanda and Vincent Yakaitis are bound together by a common experience: They were both criminally charged in connection with an attempted burglary. Powanda was the burglar, and Yakaitis was the property owner.

Ah, justice.

Indeed, that's not a misprint, parody, or a bad joke (although I wish it were the latter). Powanda was arrested and charged with criminal trespass and burglary, along with other related offenses, for executing the botched raid a little before 2:00 a.m. in February 2023 at Yakaitis' property in Port Carbon, Pennsylvania. The government charged Yakaitis, who is in his mid-70s, with using a firearm without a license after he shot Powanda, despite that it appears prosecutors agree Yakaitis justifiably used that same firearm in self-defense.

Whatever your vantage point—whether you care about criminal justice reform and a fair legal system, or gun rights, or all of the above—it is difficult to make sense of arresting and potentially imprisoning someone over what essentially amounts to a paperwork violation. That injustice is even more glaring when considering that Powanda, 40, allegedly charged at Yakaitis, who happens to be about three and a half decades older than Powanda.

Pennsylvania's permitting regime does carve out a couple of exceptions, one of which would seem to highly favor Yakaitis. Someone does not need a license to carry, according to the law, "in his place of abode or fixed place of business." Yakaitis owned the home Powanda attempted to burglarize. The catch: He didn't live there—it reportedly had no tenants at the time of the crime—opening a window for law enforcement to charge him essentially on a technicality.

If convicted, Yakaitis faces up to five years in prison and a $25,000 fine. Quite the price to pay for protecting your life on your own property. The misdemeanor charge also implies that Yakaitis has no history of using his weapon inappropriately, or any criminal record at all, as Pennsylvania law classifies his particular crime—carrying a firearm without a license—as a felony if the defendant has prior criminal convictions and would be disqualified from obtaining such a license. In other words, we can deduce that Yakaitis was a law-abiding citizen and eligible for a permit, which means he is staring down five years in a cell for not turning in a form and paying a fee to local law enforcement. OK.

Yakaitis is not the first such case. In June, law enforcement in New York charged Charles Foehner with so many gun possession crimes that if convicted on all of them he would face life in prison. Police came to be aware of his unlicensed firearms when Foehner defended himself against an attempted mugger—the surveillance footage is here—after which they searched Foehner's home and found that only some of his weapons were licensed with the state.

Prosecutors classified it as a justified shooting. And then they hit Foehner with an avalanche of criminal charges that would have resulted in a longer prison sentence than his assailant would have received, had he survived.

There's also LaShawn Craig, another New York City man whose case I covered in December. He, too, shot someone in self-defense and he, too, was arrested for doing so without a license. Like Foehner, he was charged with criminal possession of a weapon, a violent felony in New York. For a paperwork violation.

New York is a particularly relevant case study on the subject, as its highly restrictive concealed carry framework was the subject of a landmark Supreme Court case—New York State Rifle & Pistol Association, Inc. v. Bruen—which the majority disemboweled. It wasn't just conservative gun rights advocates who wanted that ruling, although you'd be forgiven for thinking so based on how polarized this debate tends to be. That Supreme Court decision also attracted support from progressive public defenders with The Black Attorneys of Legal Aid, The Bronx Defenders, and Brooklyn Defender Services. As I wrote in June about the amicus brief they submitted to the Court:

[The public defenders] offered several case studies centered around people whose lives were similarly upended. Among them were Benjamin Prosser and Sam Little, who had both been victims of violent crimes and who are now considered "violent felons" in the eyes of the state simply for carrying a firearm without the mandated government approval. Little, a single father who had previously been slashed in the face, was separated from his family while he served his sentence at the Vernon C. Bain Center, a notorious jail that floats on the East River. The conviction destroyed his nascent career, with the Department of Education rescinding its offer of employment.

In many jurisdictions, including New York, it can be expensive and time-consuming to get the required license, which in turn makes the Second Amendment available only to people of a certain class.

So where do we go from here? Those skeptical of rolling back concealed carry restrictions may take comfort in the fact that this doesn't have to be black and white. Governments, for example, can "give eligible persons a 30-day grace period to seek and obtain a permit after being charged, then automatically drop charges and expunge record once obtained," offers Amy Swearer, a senior legal fellow at the Heritage Foundation, or "remove the criminal penalty entirely" and perhaps "make it a fineable infraction," like driving without a license.

Whatever the case, it should be—it is—possible to balance public safety with the right to bear arms, and, as an extension, the right to self-defense. To argue otherwise is to embolden a legal system that incentivizes elderly men like Yakaitis to sit down and take it when someone threatens their life.

The Republican chairman of the House Budget Committee made news recently by announcing that if his party is serious about changing the fiscal path we are on, they'll have to consider raising taxes. Politics is about compromise, so the chairman is right. Every side must give a little. However, "putting taxes on the table" is not as simple a fix to our debt problems as some think. Looking at recent Congressional Budget Office reports, one can have

The Republican chairman of the House Budget Committee made news recently by announcing that if his party is serious about changing the fiscal path we are on, they'll have to consider raising taxes. Politics is about compromise, so the chairman is right. Every side must give a little. However, "putting taxes on the table" is not as simple a fix to our debt problems as some think.

Looking at recent Congressional Budget Office reports, one can have no doubts about the fiscal mess. Annual deficits of $2 trillion will soon be the norm. Interest payments on the debt will exceed both defense and Medicare spending this year and become the government's largest budget item. With no extra revenue available, the Treasury will have to borrow money to cover these expenses. Meanwhile, we're speeding toward a Social-Security-and-Medicare fiscal cliff that we've known of for decades, and we'll reach it in only a few years.

Talking about the need for a fiscal commission to address Washington's mountain of debt, the committee chair, Rep. Jodey Arrington (R–Texas), toldSemafor, "The last time there was a fix to Social Security that addressed the solvency for 75 years, it was Ronald Reagan and Tip O'Neill, and it was bipartisan. It had revenue measures and it had program reforms. That's just the reality." He made these comments after some people warned that a fiscal commission is a gateway only to raising taxes.

I understand the worry. That's what the most recent deficit reduction commission tried to do. And while I don't believe this is what Arrington is planning, I offer a warning to the chair and to the future commission: If the goal is truly to improve our fiscal situation, as defined by reducing the ratio of debt to gross domestic product (GDP) or reducing projected gaps between revenue and spending, increasing tax revenue should be limited to the minimum politically possible.

For one thing, our deficits are the result of excessive promises made to special interests—mostly seniors in the form of entitlement spending—without any real plans to pay. The problem is constantly growing spending, not the lack of revenue and taxes. The common talking point from the left that rich people don't pay their fair share of taxes is a distraction. Not only is our tax system remarkably progressive, but there are not enough rich people to fleece to significantly reduce our future deficits.

Furthermore, the work of the late Harvard economist Alberto Alesina has established that the best way to successfully reduce the debt-to-GDP ratio is to implement a fiscal-adjustment package based mostly on spending reforms. A reform mostly geared toward tax increases will backfire as the move will slow the economy in the short and longer terms, causing it to ultimately fail to raise enough revenue to reduce the debt relative to GDP. Legislators, unfortunately, have made this mistake many times without learning any lesson—at least until the deal that was cut in 1997.

As a 2011 New York Times column by Catherine Rampell reminded us, until then, all deficit-reduction deals were very tax-heavy. What the article didn't mention is that they failed to reduce the deficit. What distinguishes the 1997 deal is that it cut both spending and taxes. The result was the first budget surplus in decades helped by a fast-growing economy. Now, this lesson doesn't mean that a fiscal commission must cut taxes, but it does caution against attempting to reduce the debt largely by raising taxes.

Another risk looms in the idea of a tax-and-spending compromise; that the tax increases will be implemented while the spending cuts won't. We have many examples of this pattern, but I'll recount just one: In 1982, President Ronald Reagan made a deal with Congress (the Tax Equity and Fiscal Responsibility Act) which would have raised $1 in revenue for every $3 in spending cuts.

There were tax hikes, indeed. But instead of spending cuts, Reagan got lots of spending increases. Remembering the story years later in Commentary magazine, Steven Hayward wrote, "By one calculation, the 1982 budget deal actually resulted in $1.14 of new spending for each extra tax dollar."

The moral of this story is that putting revenue on the table to reduce the debt has a bad track record. As such, the chairman, who I believe is serious about putting the U.S. on a better fiscal path, will have to be careful about whatever deal is made.

If you’ve been spending as much time as we have with Infinite Craft, you probably didn’t notice Neal.fun has other games to play. In fact, some may be just as entertaining and addicting. After much debate, we’ve ranked the top 10 best games on Neal.fun!

10. Ambient Chaos

Image Source: Neal.fun via Twinfinite

Ambient Chaos is less of a traditional game and more of a fun tool to mess around with, especially if you’re into sound mixing. It features 30 unique sounds that you can toggle at

If you’ve been spending as much time as we have with Infinite Craft, you probably didn’t notice Neal.fun has other games to play. In fact, some may be just as entertaining and addicting. After much debate, we’ve ranked the top 10 best games on Neal.fun!

10. Ambient Chaos

Image Source: Neal.fun via Twinfinite

Ambient Chaos is less of a traditional game and more of a fun tool to mess around with, especially if you’re into sound mixing. It features 30 unique sounds that you can toggle at will, and even adjust the volume for each one. I can see it as a useful tool for filling the silence with the soothing sounds of the waves while you work.

In this week's The Reason Roundtable, Katherine Mangu-Ward is in the driver's seat, alongside Nick Gillespie and special guests Zach Weissmueller and Eric Boehm. The editors react to the latest plot twists in Donald Trump's various legal proceedings and the death of Russian opposition leader Alexei Navalny. 00:41—The trials of Donald Trump in Georgia and New York 25:04—Weekly Listener Question 33:23—Sora, a new AI video tool 43:55—The death of Al

In this week's TheReason Roundtable, Katherine Mangu-Ward is in the driver's seat, alongside Nick Gillespie and special guests Zach Weissmueller and Eric Boehm. The editors react to the latest plot twists in Donald Trump's various legal proceedings and the death of Russian opposition leader Alexei Navalny.

00:41—The trials of Donald Trump in Georgia and New York

Send your questions to [email protected]. Be sure to include your social media handle and the correct pronunciation of your name.

Today's sponsor:

ZBiotics. Pre-Alcohol Probiotic Drink is the world's first genetically engineered probiotic. It was invented by Ph.D. scientists to tackle rough mornings after drinking. Here's how it works: When you drink, alcohol gets converted into a toxic byproduct in the gut. It's this byproduct, not dehydration, that's to blame for your rough next day. ZBiotics produces an enzyme to break this byproduct down. Just remember to make ZBiotics your first drink of the night and to drink responsibly, and you'll feel your best tomorrow. Go to zbiotics.com/roundtable to get 15 percent off your first order when you use code ROUNDTABLE at checkout. ZBiotics is backed with a 100 percent money-back guarantee, so if you're unsatisfied for any reason, they'll refund your money, no questions asked.

It's quite a turn when a prosecutor defends the use of cash for financial transactions. After years of authorities treating mere possession of physical money as sketchy and grounds for seizure, this week a law enforcement official claimed there's nothing to see in her alleged cash reimbursements to her boyfriend for an enviable lifestyle arguably funded by the taxpayers. Either Fani Willis and company were right in the past and she should be subj

It's quite a turn when a prosecutor defends the use of cash for financial transactions. After years of authorities treating mere possession of physical money as sketchy and grounds for seizure, this week a law enforcement official claimed there's nothing to see in her alleged cash reimbursements to her boyfriend for an enviable lifestyle arguably funded by the taxpayers. Either Fani Willis and company were right in the past and she should be subject to scrutiny for anonymous transactions, or she's right today and she and her colleagues owe the rest of us a pass on our taste for financial anonymity.

If you haven't kept up on the details, Fani Willis is the Fulton County district attorney overseeing the Georgia election interference case, which has been described as potentially the strongest and most consequential case against former (and maybe future) president Donald Trump. At least, it was described that way until defense attorneys revealed that Nathan Wade, a special prosecutor in the case, is unqualified for the job, was romantically involved with Willis, and is being paid much more than any of his colleagues (around $654,000 in all)—money from which Willis seemingly benefited in the form of expensive vacations and other pleasures of life with Wade.

She Reimbursed Everything in Cash. Of Course.

Well, she benefited unless she reimbursed Wade for her share. Whether or not she did is among the issues raised in a hearing investigating her alleged misconduct in the case.

"I didn't ever make him produce receipts to me," Willis said in response to questions about the couple's significant expenses. "Whatever he told me it was, I gave him the money back."

"You gave him cash before you ever went on the trip?" she was asked to clarify about one vacation.

"Mmm-hmm," Willis replied.

But she not only had no receipts, she also had no ATM slips or evidence the cash existed. It supposedly came from a substantial stash she kept at home on her father's urging.

Dad's Advice and 'Printed Freedom'

"I was trained, and most Black folks, they hide cash or they keep cash, and I was trained you always keep some cash," her father, John Floyd, confirmed. "I gave my daughter her first cash box and told her, 'Always keep some cash.'"

That's great advice. Cash is essential in emergencies, useful when electronic payments systems are down, and (importantly for this case) it's private and anonymous. When central-bank types floated the idea of abolishing physical money in favor of digital currency a decade ago, prominent German economist Lars Feld retorted that cash is "printed freedom" which helps people escape state control.

But that anonymity, which Fani Willis cited as the reason she had no evidence that she'd compensated Wade for his expenses, is exactly why government officials so despise its use by mere mortals.

Governments Hate Cash

"It just was not credible," CNN legal analyst Michael Moore, a former United States Attorney, commented of Willis's testimony about "things as nebulous as cash payments so there's no way to track it." He added: "It reminded me of watching a criminal defendant take the stand."

Cash is increasingly assumed by officialdom to be nefarious in and of itself.

"Cash can play a role in criminal activities such as money laundering and allow for tax evasion," notes Investopedia. "Since 2016, global policies have been implemented to thwart the use of cash in favor of digital currency transactions."

The mere presence of physical money triggers official suspicion and the urge to confiscate.

"It's the presence of paper legal tender—U.S. currency—that underlies nearly all of the thousands of police interactions we reviewed," The Greenville Newsreported in a 2020 story on civil asset forfeiture, under which money and valuables are seized, often with no charges brought against their owners.

Like Fani Willis, CNN's Moore is from Georgia and served there at both the state and federal level, so his attitude is illuminating. Georgia gets a D- grade from the Institute for Justice (I.J.) for its forfeiture laws.

"Across 15 states for which we have reliable property data for 2018,38 currency—primarily cash—predominates, accounting for an average of nearly 70% of forfeited property," I.J. revealed in the 2020 report, Policing for Profit. Georgia was among those states and "between 2015 and 2018, Georgia law enforcement agencies forfeited more than $51 million under state law. Between 2000 and 2019, they generated an additional $388 million from federal equitable sharing, for a total of at least $439 million in forfeiture revenue."

The 2023 budget for Fani Willis's Fulton County government includes Fund 442, Federal Equitable Sharing, for "proceeds of liquidated seized assets from asset forfeitures."

Willis may have taken her father's excellent advice about keeping cash on-hand. But her office is among those putting the screws to members of the public who abide by similar counsel and rely on physical money for its utility and anonymity. To keep large amounts of cash in Fulton County, Georgia, is to risk its seizure by the authorities. Yet Willis (assuming we believe her) does much business in cash.

If Prosecutors Get To Benefit, So Do We

So, which is it? Was the Fani Willis of the past, along with most of her profession, correct in considering cash to be inherently sketchy and evidence of some sort of criminal activity? If so, the court should view her claims of cash transactions as suspicious in themselves, just as she would treat regular people.

Or is the Fani Willis of last week correct that using cash is just good sense and evidence of homey wisdom handed down through the family? If that's the case, her office should have been treating people with the same light touch she hopes to receive.

The powers-that-be should abide by the same policies they inflict on the rest of us. If they want the freedom and privacy inherent in using cash, they can't keep it as a private privilege; we all get to benefit.

My sentiments are with John Floyd and Lars Feld on this. Cash is freedom and we should always keep some on hand. If that applies to Fani Willis, it must apply to everybody.